Carbon emissions from concrete are out of control. Here's how to rein them in.

What is decarbonisation's biggest challenge? Here's a clue. It’s ugly, it’s heavy, it’s responsible for more carbon emissions than all but the two most emissions intensive economies, and it’s everywhere.

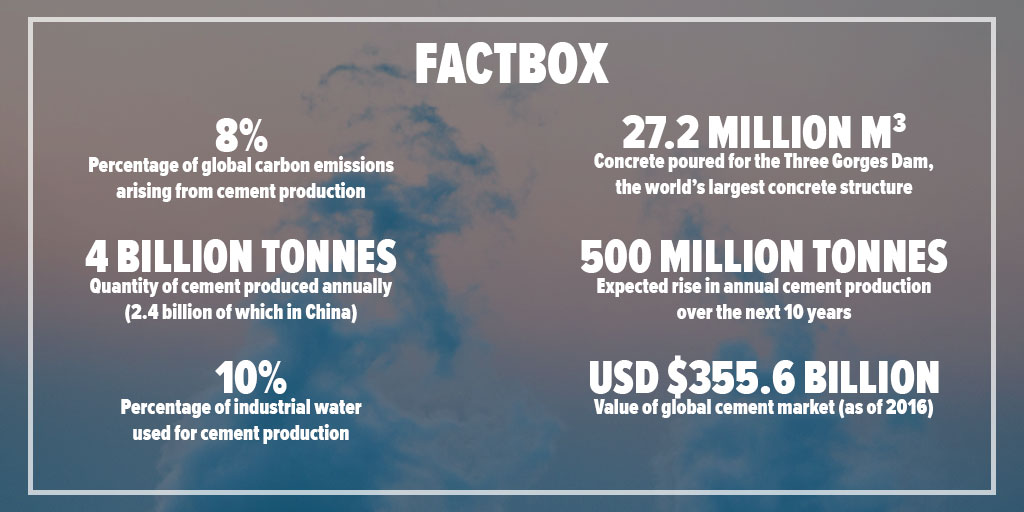

You guessed it. Concrete is the world’s most widely used building material, and we’re consuming more of it all the time. At present, we use 10 billion tonnes of the stuff a year.

4 billion tonnes of this is cement – concrete’s key ingredient. When mixed with sand, gravel and water, it creates a material that is inexpensive, easy to manipulate, and highly durable.

Within the next decade, cement consumption will have risen by a further 500 million tonnes per annum.

Most of the emissions associated with concrete come from the production of cement. For every tonne of cement the industry produces, a tonne of carbon is released into the atmosphere.

Want more articles like this? Sign up to the KNect365 Energy newsletter>>

This is a major problem, because concrete is extremely useful.

It’s so useful in fact, that it’s difficult to picture a climate resistant future without it. Wind turbines are built on concrete foundations. Sea walls, a vital defence against rising sea levels, are generally made from concrete. Hydroelectric dams are essentially massive concrete fortifications.

It doesn’t end there. Urban densification, a key strategy for improving the energy efficiency of buildings, minimising residential land usage and reducing transport sector carbon emissions, requires the construction of more high-rise buildings in city centres. These buildings will for the most part be made from concrete.

The fact that cement – itself a significant cause of emissions – plays a role in each of these climate solutions isn’t some cruel irony. It’s simply an indication of how difficult it is to undertake any kind of economic activity without it.

The use of cement is so closely linked to economic development that, without knowing anything else about a country except its level of cement consumption, you could make an educated guess at its annual rate of GDP growth.

The lowest cement consumption is seen in two types of countries: immature economies with below average GDP and little investment, and mature economies with slow economic growth and well-developed existing infrastructure.

The highest per capita cement consumption comes from the most rapidly growing regions. Unsurprisingly, China leads the pack.

What this means is that solutions to decarbonise cement are urgently needed. If solutions can’t be found, economic development imperatives must come into conflict with the need to reduce emissions.

Fortunately, there are some options on the table. Most of them are in their infancy, and it is certain that more than one solution will be needed to bring emissions down to acceptable levels.

Some of the options available are technological, and some are regulatory. Some involve other sectors, such as transportation or energy, while others require switching to alternative materials.

Figuring out which of them will be most effective in reducing the emissions from cement consumption first requires an understanding of how these emissions arise.

What causes the emissions from cement production?

Around half of the emissions from cement production arise directly from the calcination reaction used to produce clinker, the unground precursor to Portland cement (the most widely used form of cement, and the form of cement used to make concrete).

These emissions are difficult to avoid, because the purpose of calcination is to rid the input material, limestone, of its carbon content. The reaction converts limestone (CaCO3) to calcium oxide (CaO), otherwise known as lime, and CO2. The lime is used to produce clinker, while the CO2 is released into the atmosphere.

Decarbonising this part of the cement production process is tricky, but there are two approaches that can be taken. One is to reduce the quantity of clinker in cement by replacing it with something else. The other is to capture the carbon released from calcination. More on both later.

As we’ve said, around 50% of the emissions from cement production are released by the calcination reaction. A further 40% are emitted by the fossil fuels used to heat the kilns in which this reaction takes place.

Decarbonising this side of cement production means replacing fossil fuels, like coal or natural gas, with low carbon or zero carbon fuels like biomass, waste or hydrogen.

The final 10% or so of emissions come from the fuels consumed mining the materials used to produce cement and transport them to the plant. Here, electrification may have an important role to play in reducing emissions.

As can be seen, a range of solutions will be needed to bring down cement industry emissions, each of them working in tandem. This is the only approach that can reduce emissions from the three main sources arising from cement production: the calcination reaction, the fuels burned to heat the kiln, and the cement supply chain.

What about carbonation?

As the importance of reducing industrial sector emissions starts to play a bigger part in the debate around climate change, the cement industry is increasingly coming under fire.

But it has one major card to play in this debate, and it would be remiss of us to ignore it. Like plants, soil and the ocean, concrete and other cement-based materials actually act as a carbon sink.

That’s right – over a period of decades, concrete absorbs CO2 from the atmosphere. Researchers from the University of East Anglia have found that over the 83 years between 1930 and 2013, cement-based structures absorbed 4.5 gigatons of carbon. The chemical reaction which allows for this to happen is known as carbonation.

While carbonation is a significant mark in cement’s favour, it should be noted that concrete is at best absorbing only a portion of the CO2 it was responsible for releasing.

The authors of the UEA study estimate that the carbon absorbed over the 83-year period offset 43% of the CO2 emissions from cement production released over the same timeframe.

Another thing to bear in mind is that carbonation is an extremely slow process. Even if much of the carbon released by cement produced today is offset in the long-term, short-term increases in carbon emissions could have an outsized impact if they push us past certain climate tipping points (for example the melting of the Arctic permafrost, forest dieback or the collapse of the Greenland ice shelf).

On the flip side, should carbon capture and storage technology be integrated into the cement production process, carbonation could do much more than offset the emissions from cement.

If all the carbon released during cement production was captured, then carbonation could make concrete carbon negative. Using more concrete could actually reduce atmospheric CO2 levels, rather than raising them.

As impressive as that sounds, we’re still a long way away from a future in which concrete is a boon for the climate. For the time being, it’s more sensible to think in terms of mitigating an existing source of emissions.

Which brings us on to the solutions.

Factory for the processing of aggregates used to produce concrete

Factory for the processing of aggregates used to produce concreteSolution 1: Clinker substitution

The first solution is to circumvent emissions from clinker production by switching out some of the clinker for a different material. The authors of a Chatham House study on low carbon cement estimate that replacing 70% of the clinker in cement globally by 2050 could save 1.5 Gigatons of CO2 emissions a year.

There are a couple of different materials able to serve as replacements, such as coal fly ash or blast furnace slag. The former is produced as a waste material in coal-fired power stations, while the latter is a by-product from iron and steel making.

Neither is a perfect solution, as there are doubts about whether they can be obtained in sufficient quantities. Both are also available due to industrial processes that are themselves carbon intensive.

Nonetheless, clinker substitution is an inexpensive option that can be implemented today. Initiatives like co-locating kilns with coal-fired power stations or furnaces can help to accelerate the pace with which substitutes are adopted.

Solution 2: Alternative concretes and cements

There are a variety of alternative forms of cement currently being tested and commercialised. These include the biocement developed by the US company bioMASON, which uses a strain of bacillus bacteria to obtain calcium carbonate rather than relying on calcination.

‘Self healing’ forms of microbial concrete are also in development, which could minimise consumption by helping concrete structures to endure for longer.

Another option is carbon cured concrete. With these types of concrete, CO2 captured from industrial processes is injected into the material to help it harden, which sequesters the carbon and prevents it from entering the atmosphere.

Although these solutions are innovative, there are a few barriers that need to be overcome before they can play a larger role. For one, engineers and construction firms need to be persuaded of the durability of alternative materials before investing in them – no easy task.

The prices of alternative building materials also need to be brought down to levels where they can compete with ordinary cement and concrete.

Solution 3: Alternative fuels

Cement production has traditionally relied upon fossil fuels such as coal, oil or natural gas to produce the heat necessary for the calcination reaction.

An increasing number of cement producers, particularly in Europe, are switching to the combustion of waste materials to reduce emissions. These waste materials include used tires, non-recycled plastics and paper, waste oils and wastewater sludge.

Other producers have turned to biomass to meet their fuel needs. The carbon impact of biomass depends greatly on how it is sourced – waste biomass from forestry or agriculture can bring significant reductions in net emissions, while biomass sourced from virgin forest could be a worse option than fossil fuels.

Alternative fuels account for approximately 43% of the fuel consumption of European cement producers, but the adoption of alternatives has been much slower in China, India, and some of the other leading cement consumers.

Alternative fuel uptake could be accelerated in the future by the adoption of low carbon gasses, such as renewable hydrogen from electrolysis, hydrogen reformed from natural gas (with the use of CCS), synthetic natural gas and biomethane.

Solution 4: Improving energy efficiency

More energy efficient kilns help to minimise the use of fuels during the calcination reaction. Efficiency is also important in other energy intensive stages of the cement production process, such as grinding the clinker.

Although Europe is ahead of the curve on some of the solutions outlined here (such as the use of alternative fuels and substitute clinkers), the prevalence of older cement kilns means efficiency is often lower than in developing economies.

According to Chatham House, the average thermal energy consumption of cement factories is 3.5 GJ per tonne of clinker produced, which compares to a minimum achievable consumption of 2.9 GJ using the best available technology.

The average thermal energy consumption of the Indian cement industry, where equipment is generally less outdated, is 3.0 GJ per every tonne produced.

Replacing older equipment should be a priority for the most inefficient producers, although the considerable expense of doing this means that incentivisation will be key. Efficiency gains can also be achieved through the recovery of waste heat and better monitoring of industrial processes.

Solution 5: Carbon Capture and Storage

As is the case with many other forms of energy intensive industry, carbon capture and storage (CCS) could reduce the emissions from cement production without the need for alternative fuels, most of which are less readily available and more expensive.

CCS holds particular promise for the cement industry because it could also be used to capture the emissions from the calcination reaction.

At the moment, CCS in the cement industry is still at the pilot project stage. As part of the EU backed Horizon 2020 programme, a trial plant run by Heidelberg Cement in Belgium is currently being used to study the capture of CO2 emissions from cement production.

The project is testing a technology called Direct Separation, which segregates the pure CO2 released by calcination from the exhaust gases released by the furnace. Should the project prove successful, its sponsors claim that it will allow for cement production with comparable capital costs to conventional equipment.

While such efforts show significant potential, optimism around CCS is best tempered with a little realism about the technology’s commercial uptake. The costs of introducing carbon capture to other sectors, such as power-generation (particularly where retrofitting is required), have so far kept the technology from making much impact on emissions.

Another potential obstacle is the difficulty of incentivising the transportation and sequestration of the captured carbon. Co-locating cement plants with industrial facilities able to use CO2 as a chemical feedstock could provide an option, as could the use of carbon cured concrete able to trap carbon (see solution 2).

Solution 6: Reducing emissions from mining and transportation

This problem of emissions from mining and transportation cuts across sectors and will not be solely in the hands of the cement industry to solve.

Nonetheless, through their choice of suppliers, cement producers can make an impact. And there are positive indications that both mining and heavy haulage can achieve sizeable emissions reductions within a realistic timeframe.

As mining often takes place in remote areas with limited access to pipelines or power grid infrastructure, renewable energy is often proving a more cost-effective option at new mine sites.

Even where mining companies have access to the power grid, many companies (including Antofagasta and Newmont Mining), are turning to renewable energy suppliers to meet their energy needs.

As for transportation, perceptions are beginning to shift around the applications to which battery electric propulsion is suited. Tesla’s Semi HGV made headlines around the world when it was revealed that the vehicle could have a range of up to 500 miles on a single charge.

Solution 7: Effective carbon taxation

Carbon taxation has been left to last because it is a solution that touches upon each of the first six. A sufficiently high carbon tax provides the incentives needed for the cement industry to explore emissions mitigation.

Whether it is through reducing the use of fossil fuels, investing in carbon capture and storage technology, replacing inefficient equipment or switching to alternative materials, a sufficiently high carbon tax provides the price signals necessary to bring about a change in behaviour.

It should also be stressed that promoting more demanding taxes could avert a potentially much more damning outcome for the cement industry – the introduction of a cement tax.

Alarm around cement’s rising share of global emissions has prompted some researchers to advocate a specific tax levied on the building material.

The problem with the proposal is that such a tax, if not properly calibrated, could indiscriminately punish even those cement producers most inclined to invest in emissions mitigation.

It could also dispose construction companies to use alternative materials, even if these materials are more emissions intensive (such as choosing to build offshore wind platforms with foundations of steel rather than concrete).

An effective carbon tax punishes individual producers only in proportion to the emissions they are responsible for. If the cement industry can up its game to reduce emissions at a faster rate than other sectors, it could still secure a role for itself in a low carbon world.

This underlines the point that taking action to reduce emissions in the near future will be crucial to the cement industry’s long-term survival.