"FinTech codgers look back 25 years"

QuantMinds (formerly Global Derivatives) is now in its 25th anniversary year. Our new name reflects the growing breadth of quantitative topics and broad range of industries in which quants now operate. Here, David Leinweber also takes a look back 25 years, to consider and discuss some of the pivotal developments and the evolution of the industry.

Over the past thirty years, I was a founder or (co-founder) of two financial technology firms, an advisor to many others, a multi-billion institutional quant equity manager, and a low form of faculty life (visitor, adjunct, fellow) at Caltech, USC, and Berkeley.

The initial plan for this article was to have an “e-roundtable” discussion with a small group of other “fintech codgers”, passing around a series of drafts for informed 25-year insights/pontification/commentary/flames on these topics:

- High speed markets and High Frequency Trading

- Cyber-risk and TEOTWAWKI ("The End of the World As We Know It")

- What happens when everything is indexed?

- Impacts of Artificial Intelligence

- Age-ism in the investment industry

Doing an asynchronous e-roundtable isn’t easy. A search on “theory and practice joke” produces 11 million results. Most of them are applicable to the experience of trying to organize the electronic round-table discussion on these topics. It sounded good in theory, but was problematic in practice. Some people sent aggregated tomes larger than a whole issue of the JoI. Some sent marketing slogans. From “Nah!” to “I’m too busy running my bar on Maui.” to “I have condos to build in Switzerland.” to “Let’s do lunch.” There were some useful and timely contributions, which are included. I have drawn on many of the verbal comments and I appreciate the efforts that went into all of them. Elaborations, distillations and highlights of the 25-year retrospective financial technology codger views on these topics follow.

High speed markets and HFT

Back in the 1980s, Dale Prouty and I left the mainstream AI world to develop a realtime market analysis product called “MarketMind”. It was acquired by Jefferies, extended to do actual trading, and renamed QuantEx, for “quantitative execution”, then spun off, with the POSIT cross, as the Investment Technology Group. QuantEx was one of the first commercial AI systems for the buy-side to use NYSE and NASDAQ’s electronic stock order systems.

We didn’t call it HFT then – the characteristic times were in full seconds. For years, there was a “safety stop” feature that allowed human traders to review orders and cancels. It was still enormously faster than phone and fax communication between institutional investors and brokers. Automation led to the precipitous drop in commissions (fixed at 25 cents per share for years prior) and trading costs. Systems in today’s much more complex markets have characteristic times in micro- and even nano-seconds. There is a range of opinions on whether this is a positive development.

The role of equity markets is, in theory, to allow for efficient capital allocation and investment in companies that produce jobs, wealth, and economic growth. Technology was a great facilitator in this from the beginning. Telegraphy, ticker tape, market data feeds, and electronic execution systems expanded the pool of potential investors from a bunch of Dutchmen under a tree to the whole world. Markets were liquid, robust, and mostly efficient.

There have always been intermediaries in markets – including market makers, and floor specialists and upstairs brokers. Technology (and regulation) has transformed these roles dramatically. Moving from trading in eighths, to sixteenths to pennies to sub-pennies and from time scales of minutes to nanoseconds may have adverse consequences when taken to extremes.

The flash crash

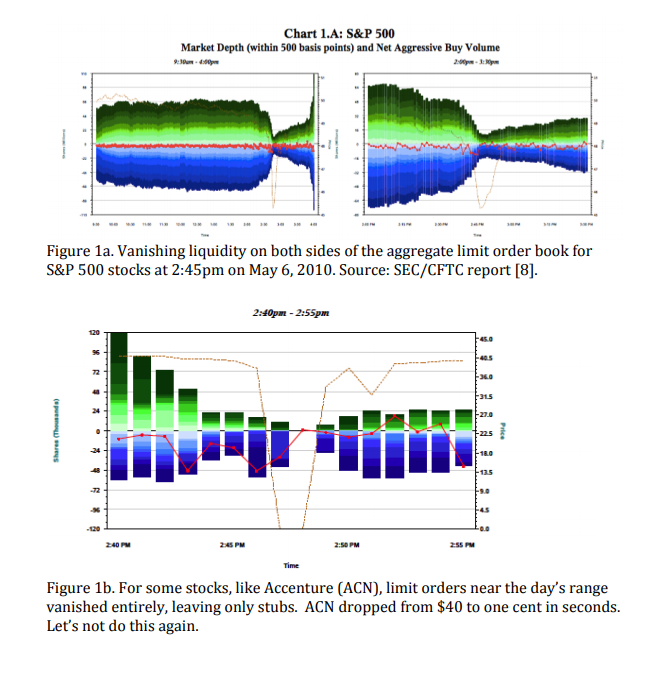

By some accounts, the Flash Crash of May 6, 2010 was an example of an adverse consequence. Highly fragmented markets, with a more than a dozen electronic trading venues, with thousands of participants feeding orders and cancels at megahertz rates can saturate communication systems. Delays from the electronic market analog of the dreaded “spinning wheel” can lead to apparent invalid market states, which send all the trade-bots to the sidelines, resulting in an evaporation of liquidity in the limit order book, followed by flash crashes (the big one in 2010 was just the most impressive example). Figure 1, from the SEC/CFTC report on the Flash Crash (8) illustrates this.

One early official explanation for the 2010 Flash Crash was that it was all due to some ill-timed futures trading by Waddell and Reid, a medium sized investment firm. Later theories laid some of the blame on a lone trader operating out of his parents’ basement outside London. These may have elements of truth, but shed no light on the many other widely reported (non Flash Crash) lesser anomalous or unstable market events, including an embarrassing failure of the BATS market system on the day of the BATS IPO in 2012.

Synchronization of market systems

On closer inspection, it really is no surprise that we see instabilities in fragmented financial systems. These are such a technical and regulatory mashup that even their clocks don’t have to match. In 2010, it was alarming to find that systems trading NMS stocks on microsecond time scales only required clock synchronization between systems of plus or minus 3 whole seconds (i.e. 3,000,000 microseconds) relative to the NIST standard clock! This is indeed like timing a swim meet with a calendar, and makes no sense other than to accommodate the large number of outdated legacy systems (some called “clocks”) at many small firms. Member firms at exchanges get one governing vote irrespective of size. Electoral College fans take note.

In the intervening years, the synchronization standard was reduced to a full second, and now, five years later, there is progress.

“Given the increasing speed of trading in today’s automated markets, FINRA believes the current one second tolerance is no longer appropriate for computer system clocks recording events in NMS securities and OTC Equity Securities, thus FINRA proposed to tighten the synchronization requirement for computer system clocks that record events in NMS securities and OTC Equity Securities by reducing the drift tolerance from one second to 50 milliseconds.”

At one point, MIFID, the European financial governing body wanted to address this by setting a one nanosecond standard. Researchers at CERN and the LHC pointed out that this was a high bar even for multibillion dollar world-beating physics labs to achieve, so MIFID backed off to 50 nanoseconds. The whole discussion, here and in Europe was remarkably uninformed and silly. Standard GPS clocks costing under $100 are accurate and synchronized to under 100 nanoseconds, and have been available for decades. The lack of synchronization between financial technology regulators and technologists, as described later, goes well beyond clocks. It remains a wholly unnecessary obstacle to safer and more stable electronic markets.

To read the full article with references, click here >>

David Leinweber will be talking about frontiers in big data, machine learning and cupercomputing at the leading quant finance event, May 14-18 in Lisbon.