The GP-led secondary market: Scaling with relationship capital

Over the past decade, GP‑led secondaries have shifted from a niche, often misunderstood corner of the private markets to a mainstream, all‑weather tool for creating liquidity and extending ownership of high‑conviction assets. Today, high‑quality sponsors are using continuation vehicles (CVs) to hold trophy assets longer, offer targeted liquidity options to existing LPs and invite new investors into their strongest companies, creating a growing pipeline of curated, relationship‑driven secondary opportunities. Keith Brittain, Co-Head of Secondaries at Hamilton Lane, shares his insights.

From laying the foundations to raising record deal flow

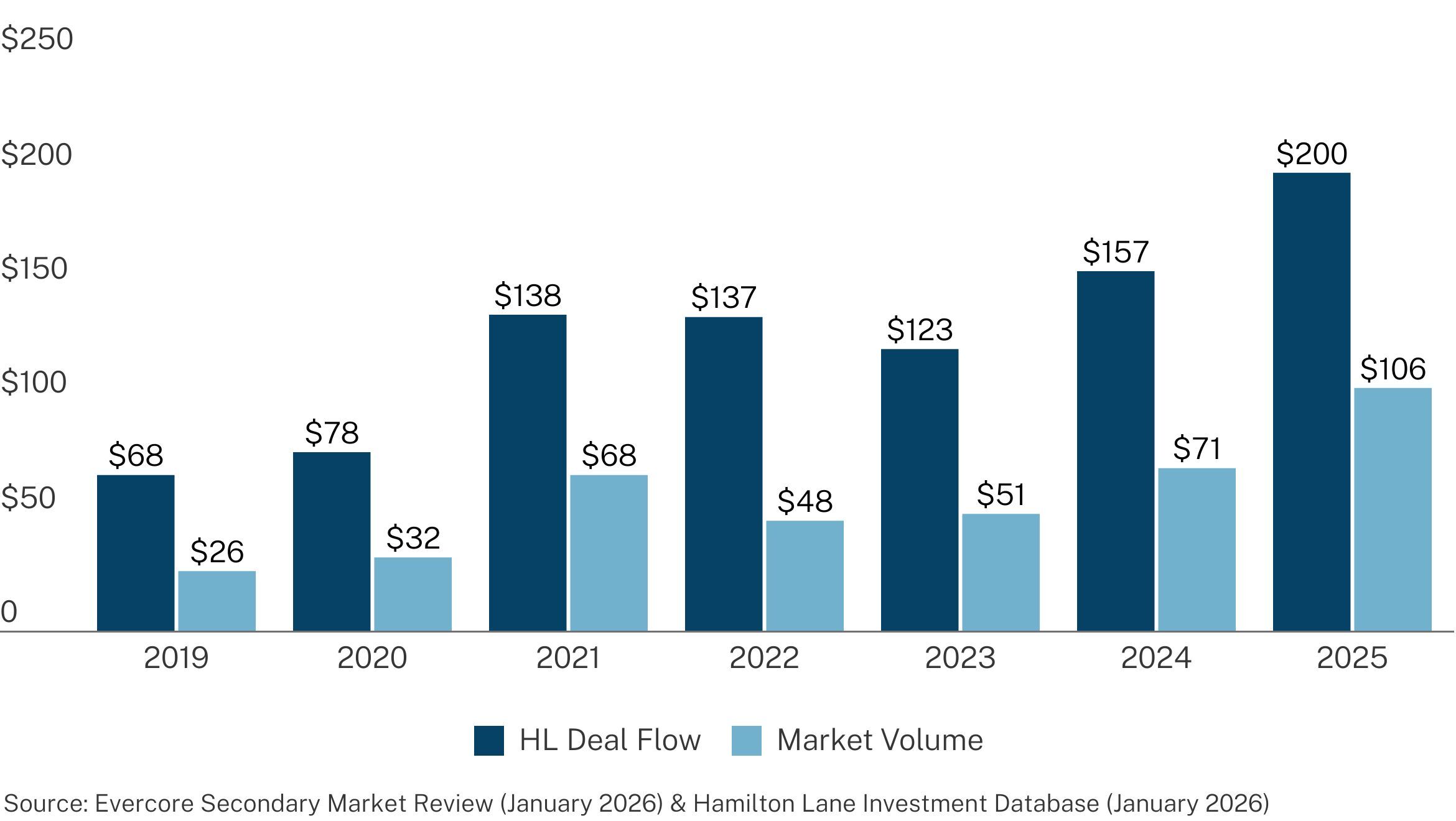

Deal types beyond traditional LP-interest transactions now account for roughly half of annual secondary market volume, with GP‑leds driving much of that expansion. From 2019 to 2024, total GP‑led market volume grew at nearly a 20% CAGR, with single‑asset CVs growing even faster. Over the trailing twelve months to June 30, 2025, GP‑led volumes reached approximately $94 billion, nearing the $112 billion total secondary market volume recorded just three years earlier. As high‑quality middle‑market GPs adopt CVs, especially single‑asset CVs, GP‑leds have become a diverse, high‑growth opportunity set offering targeted access to the private markets.

With private markets' net asset value (NAV) now exceeding $10 trillion, the secondary capital overhang ratio is nearing historical lows at roughly 0.9x, and GP-led deal flow is running at approximately 2x the rate of closings. We believe that, in the long term, well-capitalized secondary investors are uniquely positioned to capture this opportunity.

Built to endure market cycles

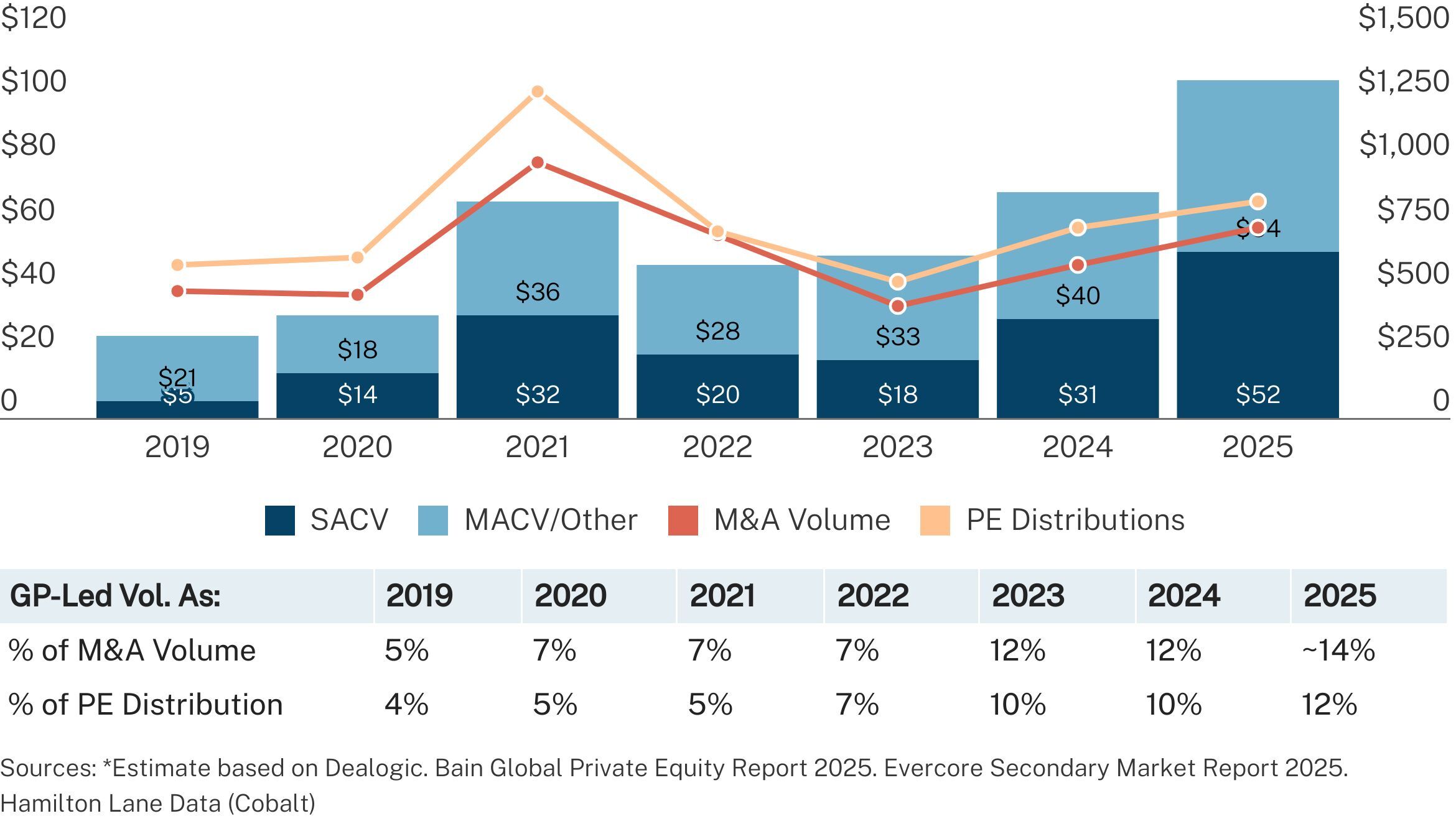

Sceptics sometimes argue that GP‑led growth is simply a byproduct of a weak M&A environment. The data suggests otherwise. Between 2019 and 2021, CV volume grew at a 38% CAGR, outpacing total sponsor‑backed M&A, which grew at 15% over the same period. From 2022 to 2024, CV volume grew at a 13% CAGR, while total M&A declined at a rate of ‑7%. In the first half of 2025 alone, CVs represented 19% of total sponsor‑backed exit volume, up from 13% in 2024.

In other words, the CV market has expanded both alongside and as an alternative to traditional exit routes. Rather than a temporary response to dislocation, GP‑leds appear to be a durable fixture of the private markets’ toolkit.

Quality assets, strong alignment and attractive performance

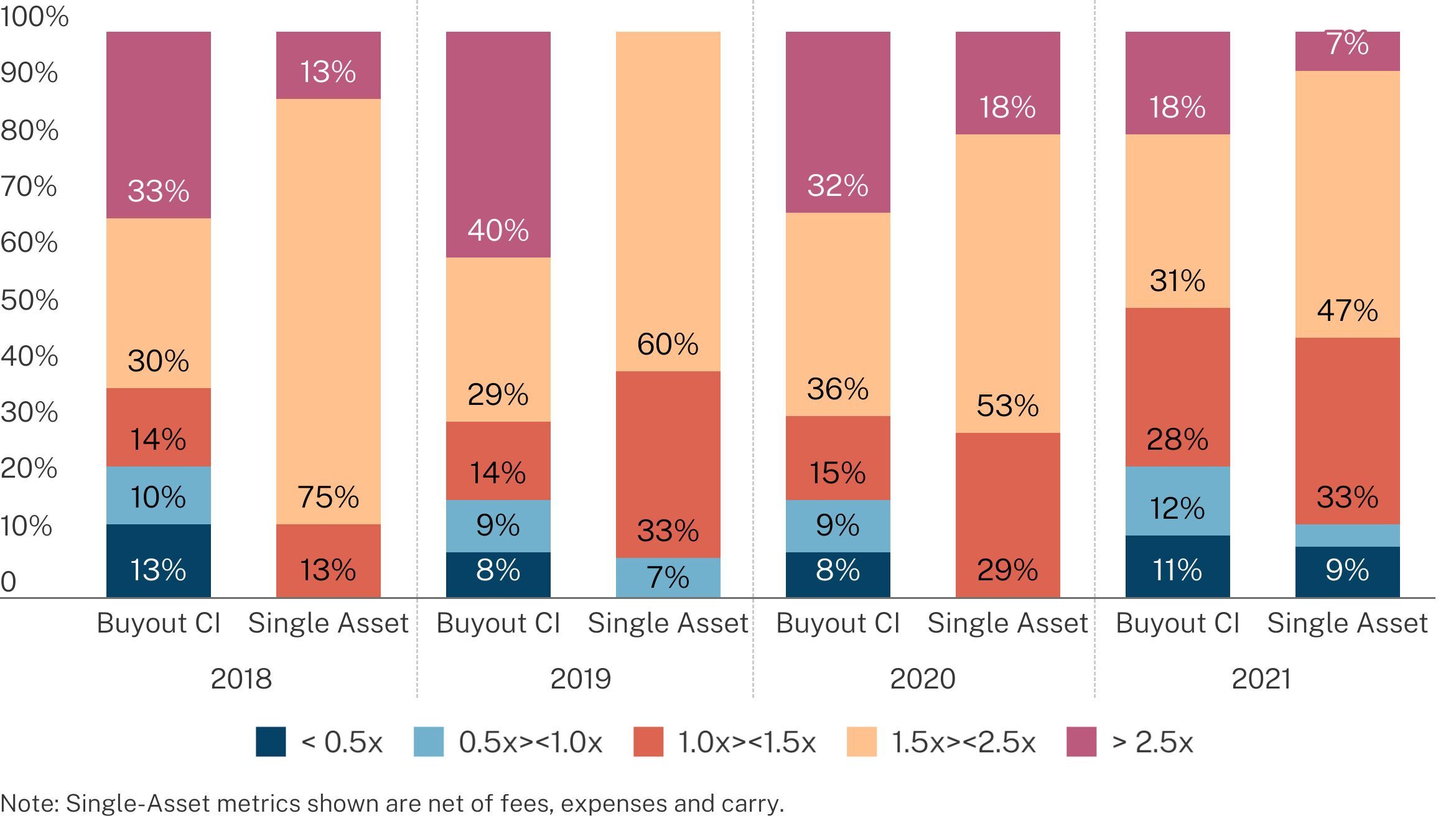

Today’s GP‑led market is heavily weighted toward high‑quality, “trophy” assets backed by high‑quality sponsors. Our sell‑side data, based on CV transactions reviewed as an existing LP between 2022 and 2025, shows:

- An average realized MOIC of approximately 4.5x for multi‑asset CVs; and

- Approximately 3.9x MOIC for single‑asset CVs, measured at the level of the selling funds.

Alignment is similarly robust. Over the past three years, average GP commitments have been roughly $90 million, or 9.2% of total capital across CVs, which is well above typical GP commitments to diversified primary funds. In addition, GPs rolled 100% or more of realised carry into the new vehicle in roughly 88% of these deals, reinforcing that managers are meaningfully “in the same boat” as LPs.

Middle-market differentiators

We believe that investors seeking to capitalise on GP‑led secondaries should focus on the small- and middle‑market (SMID) segment, where the opportunity is most attractive. Structurally, middle‑market companies tend to operate in more fragmented industries with greater buy‑and‑build potential, more conservative leverage and valuation levels and more opportunities to exit, including the ability to sell “up‑market” to larger sponsors.

In fact, our data (dating back to 2003) shows that:

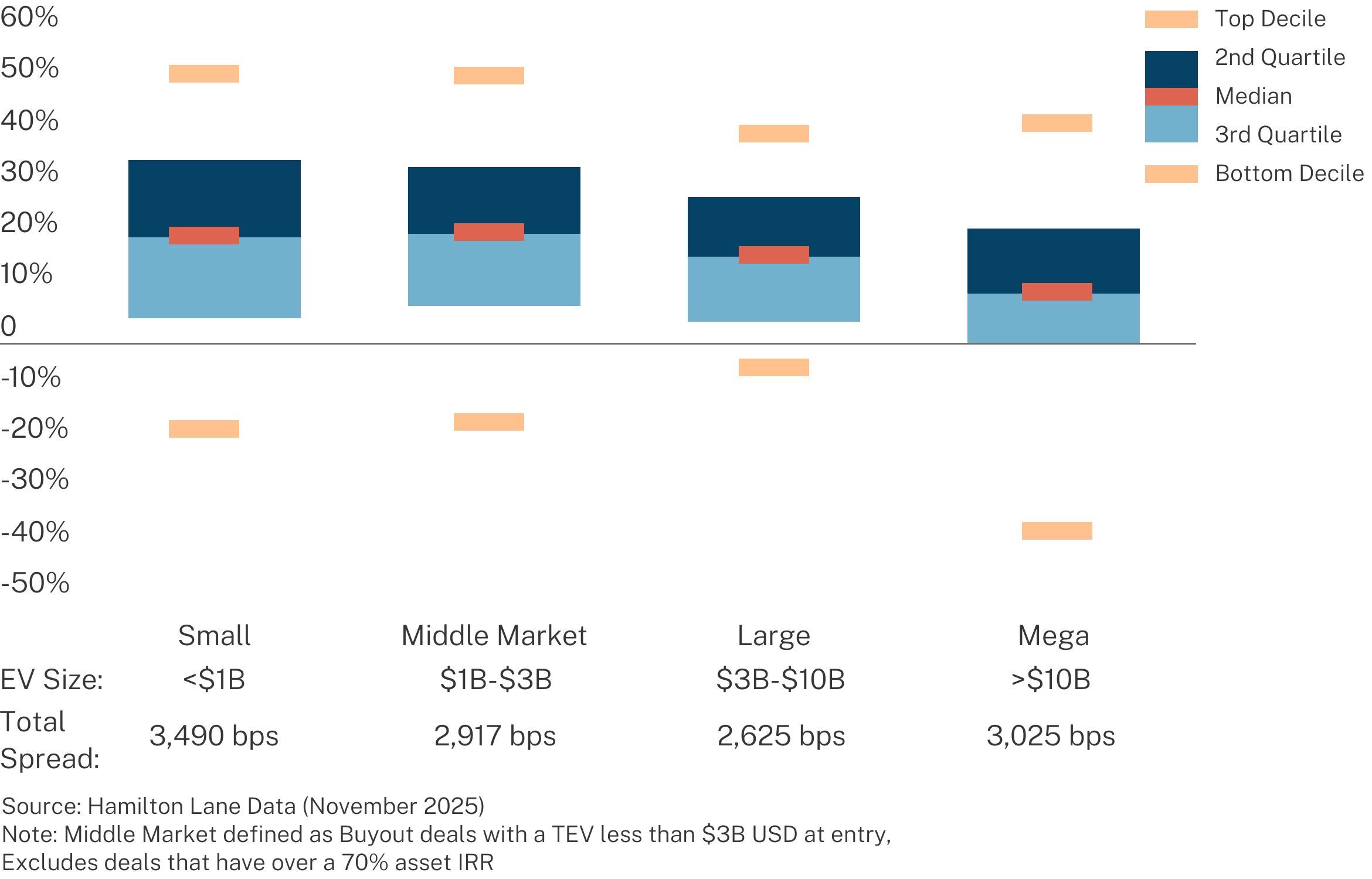

- SMID buyout deals have delivered a median realised gross IRR of 21.1%, versus 16.6% for large‑cap deals; and

- Over the same period, SMID deals generated roughly 36% greater EBITDA growth than large/mega deals.

Emerging CV data tells a similar story. According to a March 2025 analysis of 150 CVs completed since 2018, small‑cap CVs have so far produced a median net MOIC of 1.7x, compared to 1.3x for mega‑cap CVs and ~1.4x for mid‑ and large‑cap sponsors. Meanwhile, the median entry price for single‑asset CVs has been roughly 99.5% of NAV between 2022 and 2025.

In an environment where many deals clear near par, the opportunity for valuation arbitrage lies increasingly in GP conservatism, shorter durations and smaller, less intermediated companies, which are all hallmarks of the middle‑market.

As the GP‑led market has matured, the highest‑quality opportunities increasingly flow first to investors who represent strategic relationship capital, not just syndicate dollars. GPs are prioritising secondary partners who can combine deep, long‑term primary fund relationships and a track record of leading and structuring GP‑led transactions, rather than participating solely as follower capital.

Taken together, the evidence points to a GP‑led market that is large, growing and undercapitalised. However, only certain investors are positioned to capture its growth. We believe the full potential of GP‑led secondaries will accrue to platforms that combine specialised secondary expertise, scale and deeply embedded GP relationships to consistently lead, rather than follow, GP‑led transactions, especially in the middle market.