Posted by Q&A with Ramey King Insurance on 29 May 2026

Turn insurance into a strategic tool in the 2026 market cycle

What should you understand about the 2026 insurance market?

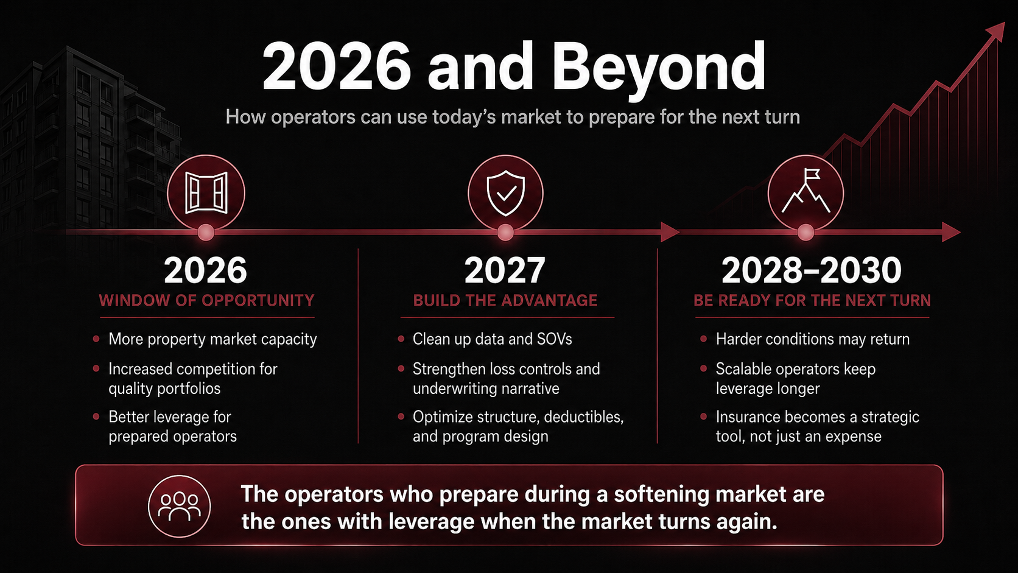

The property market is resetting. After several difficult years of rate pressure, limited capacity, and stricter underwriting, carriers are competing again for clean, well-managed portfolios. The best outcomes are going to operators who can clearly demonstrate risk quality through accurate statements of value, updated replacement costs, roof ages, electrical updates, loss history, lender requirements, and documented controls. A more competitive market does not eliminate underwriting discipline. It rewards preparation. Strong submissions give carriers confidence, and confidence helps them pencil their strongest number upfront. The market is giving prepared operators a window, but it is still asking for a clear reason to compete.

How does scale change the insurance conversation for multifamily operators?

Scale creates options. A single asset is often priced property by property with limited flexibility around structure. Larger portfolios can tell a broader risk story. Instead of asking, “What is the lowest quote on this location?” the conversation becomes, “What structure gives the operator the most control, flexibility, and long-term stability?” Scale can open the door to master property programs, layered placements, shared limits, deductible options, and eventually captive or program-based solutions. When scale is paired with strong operations, the operator has more leverage because the risk is presented as a portfolio strategy, not a one-off transaction. That is where insurance can start supporting acquisitions, refinancing, lender compliance, and long-term NOI strategy.

What kind of data should operators have ready before going to market?

Underwriters want clarity. Operators should maintain clean SOVs, accurate building values, year built, roof age, roof type, wiring details, electrical panel information, plumbing and HVAC updates, occupancy, protection class, lender requirements, and five years of currently valued loss history when available. The strongest operators also document what changed after a loss. If there was a fire, water loss, freeze event, liability claim, or crime issue, the loss run rarely tells the full story. Completed repairs, vendor invoices, inspection reports, security upgrades, maintenance procedures, and operational changes help underwriters understand why the risk is better today. Clean data creates speed, but more importantly, it creates trust.

Can operators with losses still get competitive terms?

Yes, but unexplained losses create problems. A loss does not automatically eliminate market interest, especially in multifamily where carriers understand that claims happen. What matters is whether the operator can explain what happened, what was corrected, and why the same issue is less likely to repeat. Clear narratives, corrective action, and loss controls help markets price the risk as it stands today, not just the loss history. The best number often comes from the carrier with the clearest understanding of the risk. Storytelling is not marketing language in this context. It is underwriting strategy.

How should apartment operators prepare beyond 2026?

Operators should use this window to build leverage before the next hard market. Insurance cycles do not stay soft forever. Capacity can tighten quickly after catastrophe activity, reinsurance pressure, poor loss performance, or broader economic volatility. The operators who prepare during a softening market are the ones with options when conditions turn again. That means cleaning up data now, improving controls, reviewing deductible strategy, aligning coverage with lender requirements, and evaluating whether the current structure supports the business plan. By 2028 to 2030, the strongest operators will not be buying insurance one property at a time. They will use portfolio strategy, master programs, scale, data, and risk financing tools to protect NOI and stay ahead of volatility.

—————

IMN's Middle Market Multifamily event series brings together the people and insights that matter most across the US and Canada, giving multifamily stakeholders direct access to the trends, strategies, and relationships they need to stay competitive and informed.