China – to do or not to do

China is always both fast and slow. Slow to change but a fast adopter once initiated. As China opens the financial sector to foreign majority ownership, my clients find themselves grappling with the question of just how to compete in the marketplace.

China is always both fast and slow. Slow to change but a fast adopter once initiated. As China opens the financial sector to foreign majority ownership, my clients find themselves grappling with the question of just how to compete in the marketplace.

For years, I’ve helped global asset managers move past the complications of continuously changing regulations. Move past the ‘how to’ of market access. In the end each manager lands on a singular issue: how exactly does one graft a company’s global DNA onto such a unique market? While regulations are a good analog of market direction, I find that what matters most is deciding who you will target and why. The answer to that will fundamentally drive your business plan and allow you to slot in, or set aside, new rule issuance in an ever-changing market.

Understanding the underlying dynamics of investor demand and the economic undertones at play is critical. Here’s my take on market growth drivers – past and future:

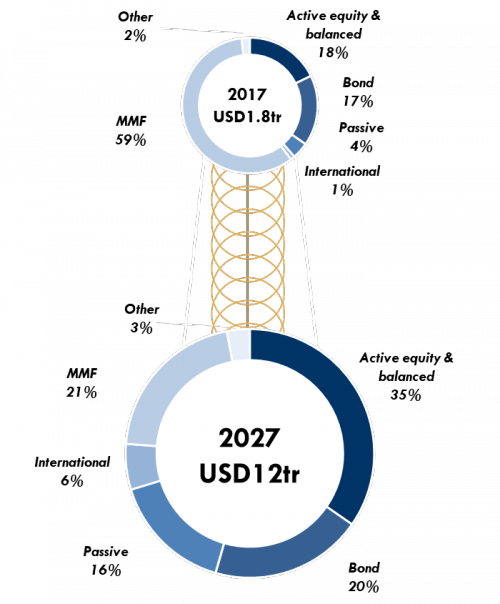

AUM growth

Moving forward, the onshore market will see the most growth. China will maintain an aggressive home bias but that will give way to a need for global solutions in time.

- Looking back…Mutual fund AUM quadrupled over the past 10 years to USD1.8tr (2017-end), a historic growth achieved without the support of any defined contribution pension flows to date. Bank disintermediation combined with market volatility pushed flows into short-term products, while critical interest rate reforms pushed better risk/return and cash-equivalent products.

- To look forward…Expect a six-fold increase in mutual fund AUM to USD12tr by 2027. Increased depth and breadth within domestic capital markets stand to dampen volatility and attract long-term investors. The introduction of tax-incentivized pension programs this year will lead to increased flows and a more mature market, with pension flows reaching 40% of total fund AUM by 2027.

- Flows into global products appear sizeable in absolute terms (USD715bn) but will represent no more than 6% of industry AUM. The largest, AUM needle-moving opportunity without a doubt resides locally in the onshore market. But cross-border plays are not without merit: as China goes global – pursuing investment and business abroad – offshore needs will begin to differ from those onshore. The geographical split of such organic asset growth could increasingly sideline the importance of capital controls over time. Financial solutions will need to address both pools of assets holistically.

Product demand

Product demand

A strong belief in active management will persist, but as property investments turn debt-driven, there will be a growing need for portfolio diversification and returns achieved on a risk-adjusted basis.

- Broadly speaking, a unique risk-reward profile exists in China that differs from global markets. With property a common investment that has claimed a near 20-year streak of appreciation, investment allocations have remained barbelled between equities and property with little diversification in-between. Cash-acquired property has long doubled as both a savings investment and a retirement plan in a country devoid of commercial pensions – until now. An uptick in mortgages – dovetailed with new-to-market tax-incentive retirement programs and target date funds – will encourage product diversification.

- Contrary to global trends, China claims a lower adoption rate of low-fee passive products, but this will change as diversification becomes more commonplace and even sought after. Cash-equivalent solutions will however experience a decline in their overall share of industry AUM, in favor of active equity and active fixed income as end-client demand continues to mature.

Profitability

With mutual fund companies generating 30-40% in net margins on average, total industry profitability is set to rise from USD4.4bn in 2017 to USD32bn by 2027. The key to capturing flows lies in market timing and vigilant monitoring of evolving investor demand.

Chantal Grinderslev advises global financial services firms on their China strategy and execution. At present she specializes in distribution dynamics, RMB credit and cross-border flows, but her functional focus remains broad: reconciling business goals with operational practicalities. Prior to joining Z-Ben Advisors, Chantal focused on policy and macro-economic issues in Beijing, London, Dakar, and Washington DC, working first as the director of a national non-profit and later as a diplomat. She holds degrees from the Georgetown School of Foreign Service and London School of Economics.

Click to find out more about Chantal Grinderslev at FundForum Asia >>