Control the controllable, weather the rest: Private equity midyear report 2026

At a glance

- Amid early-year market disruptions, investments, exits, and fund-raising all dragged in the first half, and liquidity remained a major challenge.

- AI continued to loom as a disruptive factor but also as an opportunity to transform how portfolio companies and PE firms operate.

- As portfolios age, proactive firms are taking important steps to increase investor distributions, but they’re also intently focused on building the systems necessary to consistently generate alpha.

Call it the “Groundhog Day” dynamic. Recovery deferred ... again.

A year ago at this time, the private equity industry was poised for an upturn that never really took hold. Early-year optimism was dashed by tariff turmoil—just the latest in a long line of market dislocations dating back to the Covid-19 pandemic.

This year: more of the same. Coming into 2026, the buyout market had largely shaken off tariff concerns, and dealmaking was on the rise. But then three more shocks arrived in rapid succession: the AI-driven “SaaSpocalypse” in software, redemption stress in private credit, and the war in Iran with its attendant spike in oil prices.

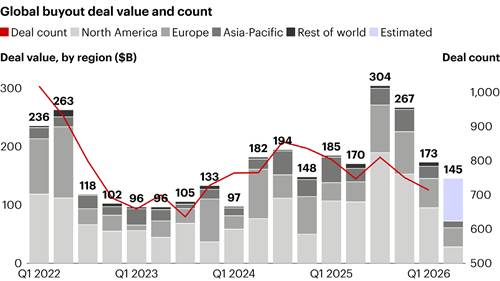

The reduction in dealmaking has been sharp and wide-ranging (see Figure 1). Amid the new bout of uncertainty, bid-ask spreads have widened, investment committees have pulled back, and exit momentum has stalled out. Select transactions continue to clear—and at high prices—but mostly those involving A-plus assets.

Most frustrating is that there’s nothing fundamentally broken in the financial markets. Public equities, pumped up by (sometimes tentative) AI euphoria, continue to defy gravity. SpaceX, OpenAI, and Anthropic are lining up for trillion-dollar initial public offerings. The global economy remains in expansion mode, and there’s ample dry powder to do deals. The debt markets are open and functioning, despite the private credit jitters.

So, where does that leave private equity? Given the growing pressure to buy and sell companies, it wouldn’t take much to unlock a wave of new dealmaking in the year’s second half. But a truly sustained upturn in activity will likely depend on the market finding an equilibrium that lasts more than a quarter or two. There’s no question the fog will lift eventually—it always does. In the meantime, though, the general partners (GPs) positioning themselves to lead out of the slump are focusing on what they can control now, not what they can’t.

Figure 1: Hopes that 2026 would be a bigger year for dealmaking have yet to materialize

Notes: Excludes add-ons, special-purpose acquisition companies, loan-to-own transactions, and acquisitions of bankrupt assets; based on announcement date; includes announced deals that are completed or pending, with data subject to change; deal value includes deals with disclosed value only and includes net debt where relevant; deal count includes deals with disclosed and undisclosed value; geography based on target’s location; Q2 2026 deal value and deal count estimated based on data through May 18. Source: Dealogic

That starts with recognizing that private equity has entered a much more difficult and competitive era—one defined by higher interest rates, stubbornly high asset prices, and less of the multiple expansion that powered so many deals in the past. Generating consistent outperformance in the years ahead is going to require ever sharper strategic clarity and the value-creation system to back it up. It will also mean accelerating distributions to limited partners (LPs) by taking practical steps to boost exit momentum.

The firms best placed in today’s environment are concentrating scarce resources where they have a differentiated right to win. They’re building repeatable models for underwriting and value creation—both operational and strategic. They’re leaning hard into AI, not just as a risk to manage or a cost-cutting tool but also as a means to develop new products, create new revenue opportunities, and sharpen decision making at the firm level. With holding periods stretched, firm resources constrained, and disruption a constant, the premium is on specialization, operational capability, talent, and execution discipline. The hard work done in market troughs to develop these competitive attributes is often what determines who leads in the next cycle.

Here’s a look at how the first half unfolded.

Investments

The net impact of the early-year market dislocations is that investment activity has slowed overall for buyouts, but unevenly across sectors. The industry’s overhang of dry powder means GPs must continue to hunt for deals where they can find them. Yet there are “green zones” where conviction still exists and “red zones” where uncertainty is highest.

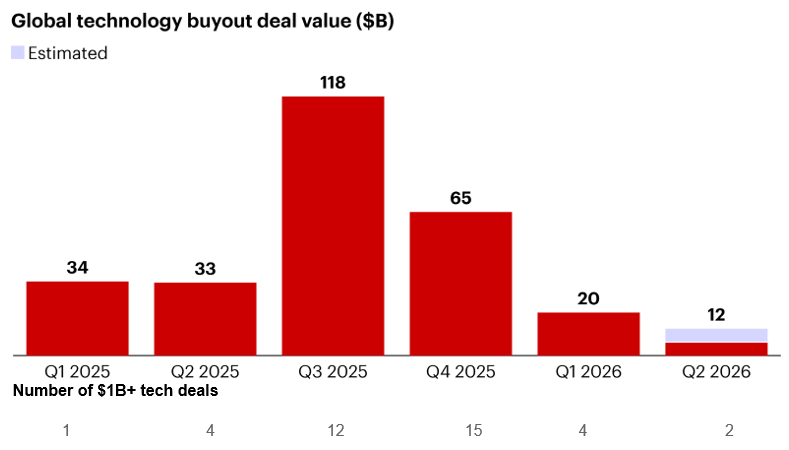

Technology falls somewhere in between. Uncertainty about what companies are worth today has caused tech deal value to drop 70% from the fourth quarter of 2025 to the first quarter of 2026, with fewer large software deals getting done (see Figure 2). Dealmaking didn’t come to a halt by any means—transactions like EQT’s acquisition of Adevinta’s Spanish business and Francisco Partners’ buyout of Jamf found their way to completion. But February’s nearly 30% drop in public market software valuations (and subsequent partial recovery) signaled the degree to which uncertainty around AI’s impacts is unnerving investors and clouding future prospects.

Figure 2: Technology deal value has fallen off sharply amid deep uncertainty about AI disruption

Notes: Excludes add-ons, special-purpose acquisition companies, loan-to-own transactions, and acquisitions of bankrupt assets; based on announcement date; includes announced deals that are completed or pending, with data subject to change; deal value includes deals with disclosed value only and includes net debt where relevant; Q2 2026 includes deals announced prior to May 18. Source: Dealogic

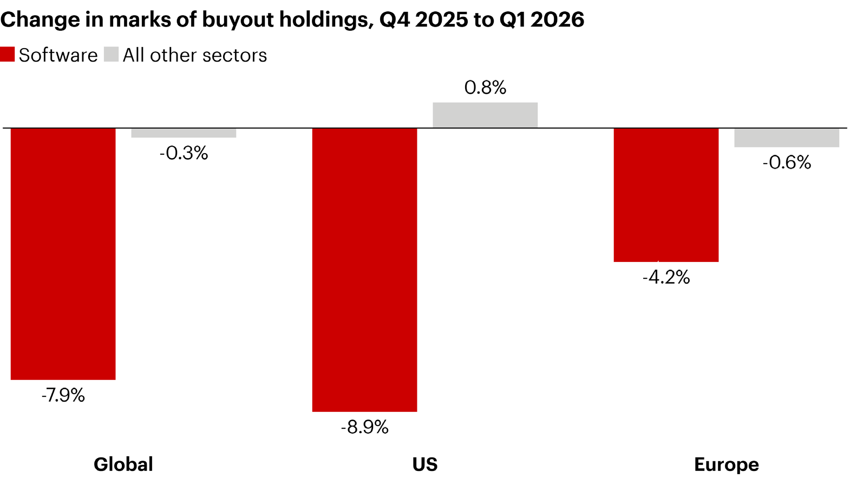

Figure 3: Buyout software valuations dropped by around 8% in the first quarter

Notes: Global and US calculated in US dollars, Europe in euros; changes in marks are capital weighted. Source: MSCI Private Capital Solutions

The first real look at how that uncertainty translated into private company valuations comes from a proprietary MSCI analysis of first-quarter buyout marks. Through the end of March, software valuations in private equity portfolios declined roughly 8% overall—far less than the public market correction but still meaningful. The decline was notably more muted in Europe, where software marks fell just 4.2% vs. 8.9% in the US (see Figure 3). Both the MSCI and public company data also point to a wide dispersion of outcomes beneath the surface.

Read Bain's full Private Equity Midyear Report here.