Enhancing customer experience of savings products through AI-based optimal product design

Given the longer lifespan, the rising healthcare costs, and the persistent low interest rates, savings behaviors have experienced significant changes over the last decade, illustrated by the increasingly differentiated savings patterns, in line with new needs associated to subsequent life phases.

Meeting the expectations of the insured thus requires an optimization of the product design, through product features tailored to the savings patterns, for an enhanced Customer Experience.

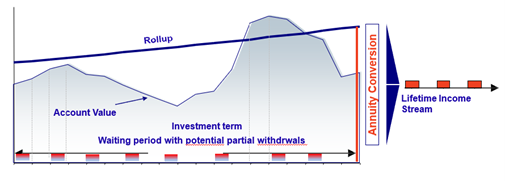

Savings & Retirement products guarantees to the customer a life annuity (= a regular and homogeneous income stream, paid until death = "Lifetime Income Stream") at the end of a waiting period, during which savings are invested in financial assets ("Account Value") and benefit from a Guarantee increasing at a minimum rate ("rollup"). The customer can also make one-off withdrawals of varying sizes.

Why is a customer-centric optimal design for an enhanced Customer Experience needed?

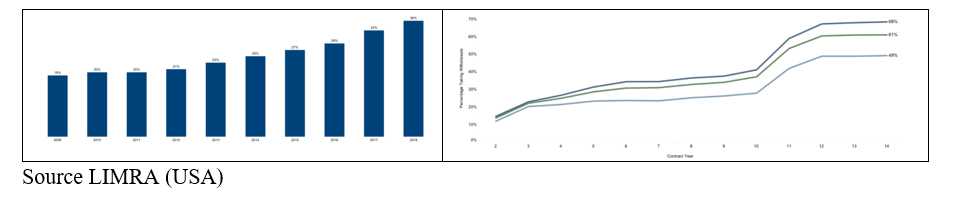

Savings behaviors have significantly changed over the past decade, as illustrated by an increasing use of ther accumulated savings, and this in an accelerated way with age.

There are three main types of Savings behavior patterns, illustrated by the frequency and withdrawals size, strongly influenced by age:

• Before the age of 60: one-off withdrawals of heterogeneous sizes, most often massive, illustrative of the consumption of expensive durable goods, real estate purchases, financing education and children's studies, or periods of unemployment.

• From 60- to 70-year-old: regular withdrawals, of moderate and homogeneous sizes during retirement, illustrative of the entry into annuity.

• Post 70-year-old: mostly the entry into annuity with regular moderate and homogeneous withdrawals; but also excess withdrawals (for tax reasons or donation).

This segmentation of customer savings patterns illustrates an increasingly strong differentiation behavior, and in turn calls for an optimization of the product design.

How to implement a product design for an enhanced Customer Experience?

1/ An explicit AI-based modelling of efficient savings behaviour

The Savings are invested in an investment account A with volatility σ.

The contract events take place at the discrete policy years, at which the future cash flow fn can take 3 forms:

- in case of death: a death insurance amount Dn– with probability pn , paid to the beneficiaries in the event of the death of the insured while the cash flow ends.

- in case of non-death: 2 forms – with probability(1-pn):

- a withdrawal of γna variable amount [0],An] which reduces the investment account An and the guarantee Gn

- or the activation of the life annuity of amount In,

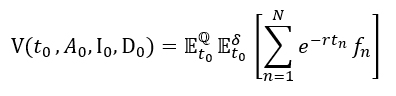

The Customer experience is measured by the value of the retirement savings contract, i.e. the average sum of future cash flows discounted over the life of the retirement savings contract:

By noting 𝑓 = (𝑓1,𝑓2,…,𝑓𝑁) the savings consumption strategy, we consider that the empirical patterns correspond to an optimal strategy 𝑓∗ that maximizes customer satisfaction:

![]()

This is a problem of optimal control of the random withdrawal, whose resolution is carried out recur-sively, starting from the terminal condition of date N:

2/ Enhancing the Customer Experience through product features that meet customer expectations

The introduction of specific product features leads to savings behaviour in line with the observed patterns, for an enhanced Customer Experience.

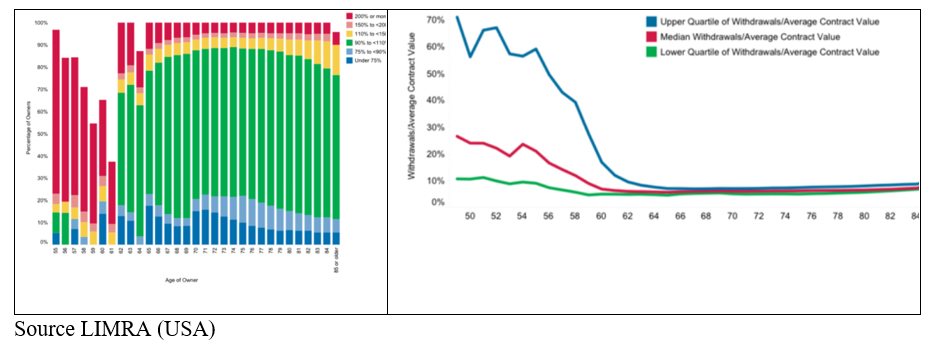

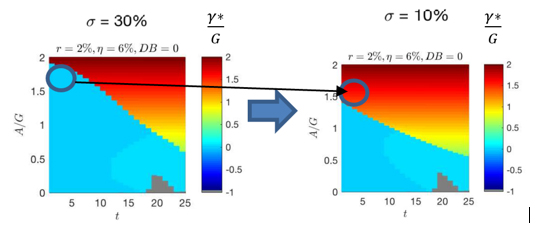

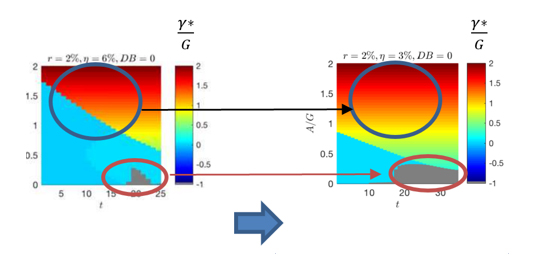

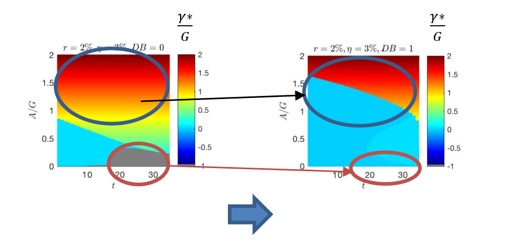

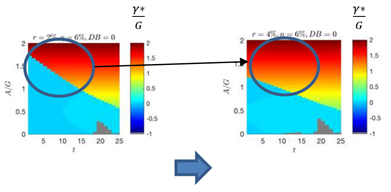

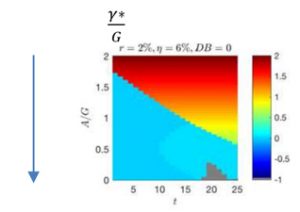

Behaviours can take the form of (i) withdrawals (γ*)/G>0 (expressed as % of guarantee G) or (ii) activation of the life annuity ((γ*)/G=-1) in the chart below, depending on the past duration t and the ratio "A/G" (investment account A divided by guarantee G).

1/ The choice of less risky S investment assets (lower volatility, 10% vs. 30%) encourages earlier savings withdrawals, in line with the below 60-year-old savings pattern:

2/ the introduction of a variable growth rate η of the guarantee, (i.e. decreasing with the fall in interest rates), favours no only a smaller disparity in the amounts of withdrawals, but also a more frequent activation of the life annuity, in line with the observed profile of young retirees aged 60 to 70.

3/ the introduction of a death guarantee promotes not only smaller withdrawal amounts combined with a few withdrawals of massive size,; but also the postponement of withdrawals and the activation of the life annuity, in line with the observed pattern of those over 70 years of age.

The effectiveness of the 3 product designs above is itself increased or attenuated,

• by the economic environment because a rise in interest rates encourages to increase the frequency and withdrawals size:

• and by the past performance of the contract: because a low investment account A and / or a high G guarantee encourage to reduce the frequency and amount of withdrawals, and to activate the life annuity earlier.

Conclusion

Longer life expectancy, increasing lifestyle and health care costs, and the persistence of low interest rates have contributed to the emergence of increasingly differentiated savings behavior patterns.

The explicit quantitative modelling of customer-centric efficient savings behavior makes it possible to select the product features that meet customers ‘needs and expectations, in line with their empirical savings behavior patterns, for an enhanced Customer Experience.

Aymeric Kalife is a CEO at iDigital Partners & Adjunct Professor at Paris Dauphine – PSL University.