Has private equity lost its historical advantage in today’s economy?

Over the past decade, returns from private and public equity have converged. Should we be worried?

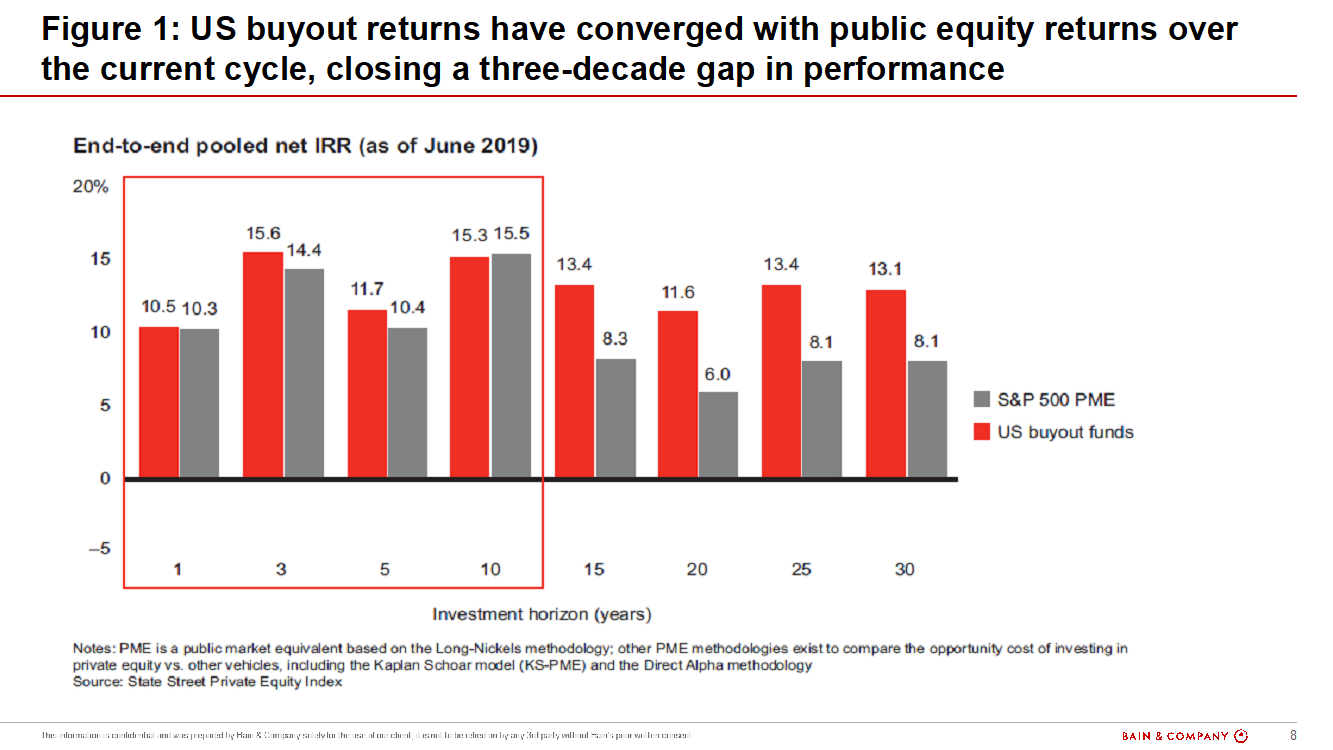

Investors have poured more than $2 trillion into buyout funds over the past decade for a simple reason: They deliver. For 30 years, US buyouts have generated average net returns of 13.1%, compared with 8.1% for an alternative private-market performance benchmark, based on the Long-Nickels public market equivalent (PME) method and using the S&P 500 as the proxy.

Shorten the time frame, however, and the picture is less rosy. Since 2009, when the global economy limped out of the worst recession in generations, US public equity returns have essentially matched returns from US buyouts at around 15% (see Figure 1).

While a 15% average annual return net of fees is impressive even by private equity’s own high standard, parity with public markets is not what PE investors are paying for. Institutions that allocate increasing portions of their portfolios to buyout funds have good reason to expect a premium. All things being equal, public equities offer more liquidity at less cost.

And that raises a disquieting question for buyout managers: Will the convergence in 10-year returns make it harder to raise the next $2 trillion?

The power of cycles

Working with Professor Josh Lerner of Harvard Business School, as well as State Street Global Markets and State Street Private Equity Index, we analyzed what’s been driving returns in both markets. Bain & Company’s 2020 Private Equity study found little to suggest that competition from the public markets is likely to persist.

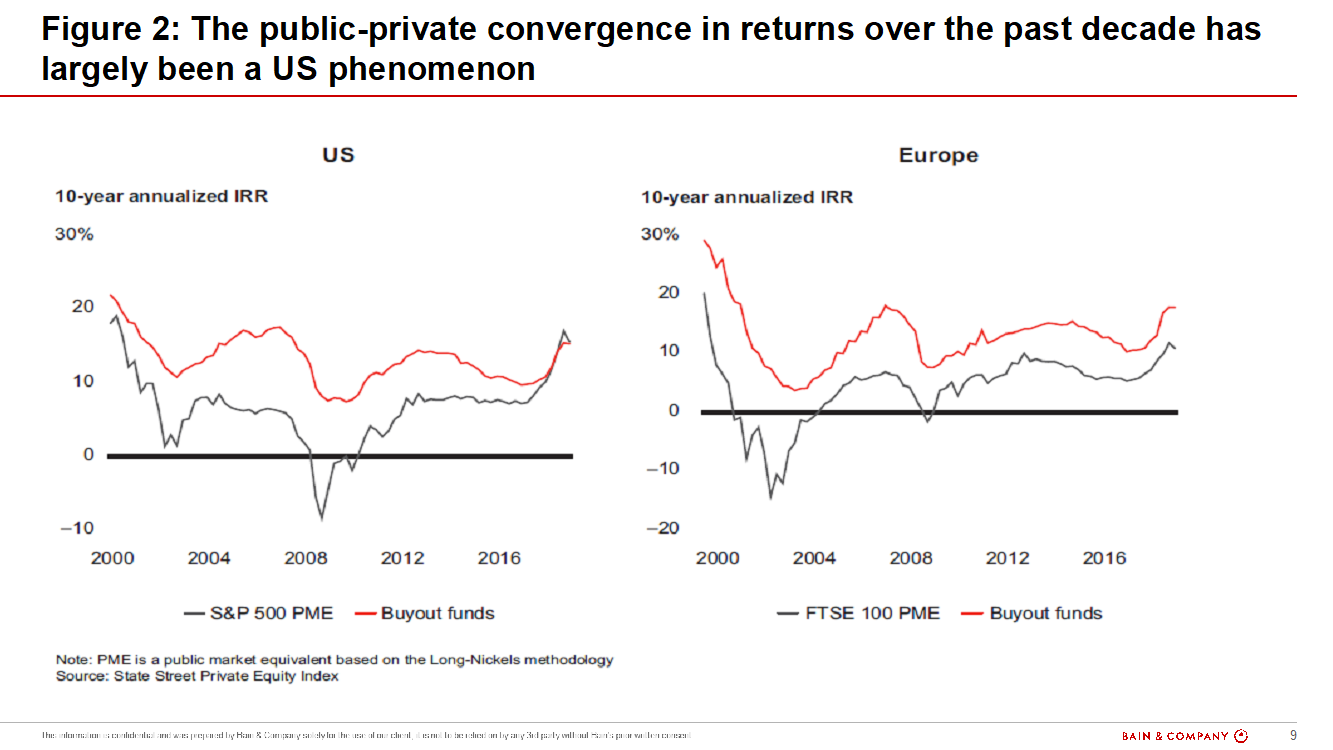

Given the historic sell-off in the wake of the global financial crisis, US stocks were teed up for a dramatic rebound. Over the ensuing decade, accommodating monetary policy and trouble in European markets drove investors to seek solace in the S&P 500. It’s worth noting that public and private returns have not converged in Europe, where PE continues to outperform (see Figure 2).

Several periods in US market history have produced similar surges, including the decade ending in March 2000, when the dot-com bubble drove a 19.4% 10-year return for the S&P 500 PME index. Inevitably, though, public markets revert to the mean.

In the decade following the dot-com bust, the PME index’s annual return fell to 0.08%, while private equity averaged 7.5%. As noted earlier, the PME index has posted an 8.1% annualized return over the past 30 years, which is consistent with the 8% long-term average logged by the S&P 500. This gap over time is why investors continue to flock to private equity. Since 2000, net asset value for global buyouts has grown 3.5 times faster than the public markets.

The performance imperative

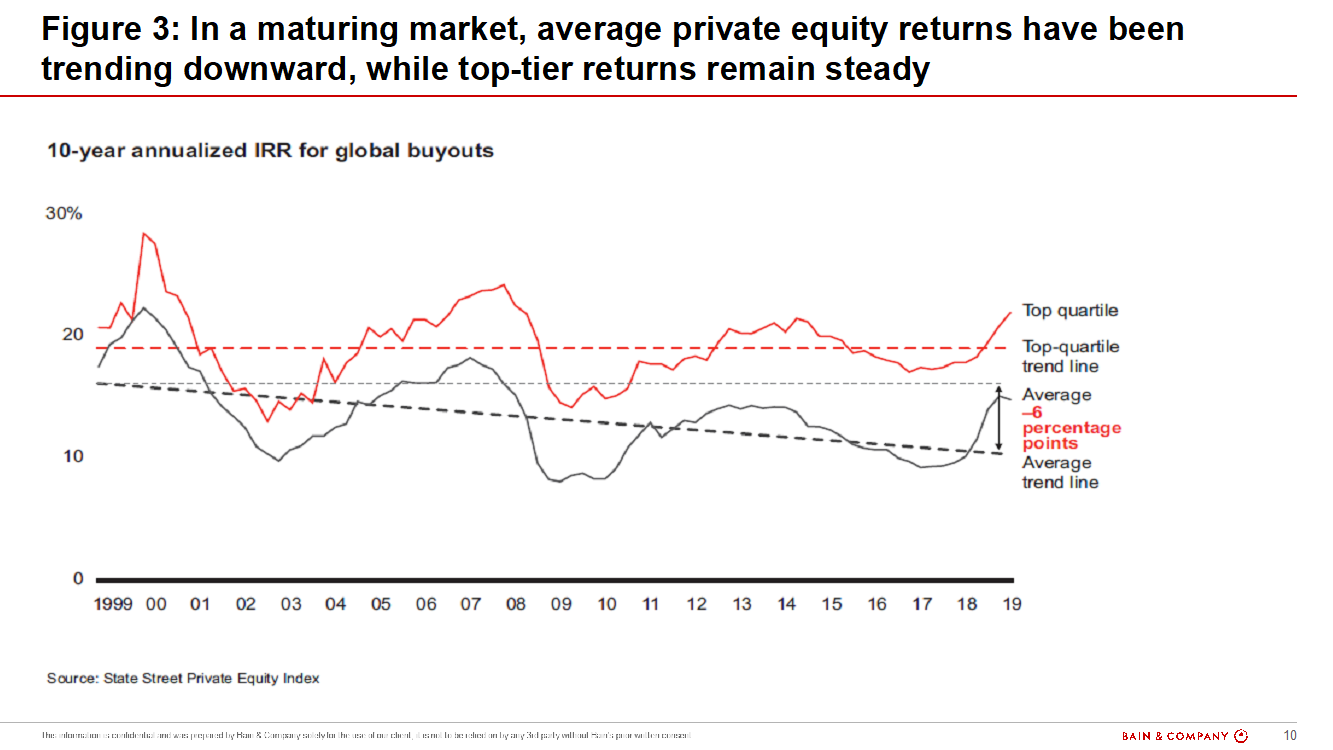

But none of this means that PE funds can relax. While competition from the public markets will surely ease at some point, the long-term trend in PE returns is more troublesome. As strong as private equity’s performance has been for the past decade, buyout returns have trended downward over the past 30 years as the industry has matured and become more competitive. Draw a trend line between the average 10-year return in 1999 and the average 10-year return today, and it shows a decline of 6 percentage points (see Figure 3). Extend the same slope out another 10 years, and PE returns start to look a lot less compelling.

Yet Figure 3 also shows that the industry’s top-tier funds are bucking this trend, which is why investors increasingly reward them with the most new capital. The question is, what are they doing right?

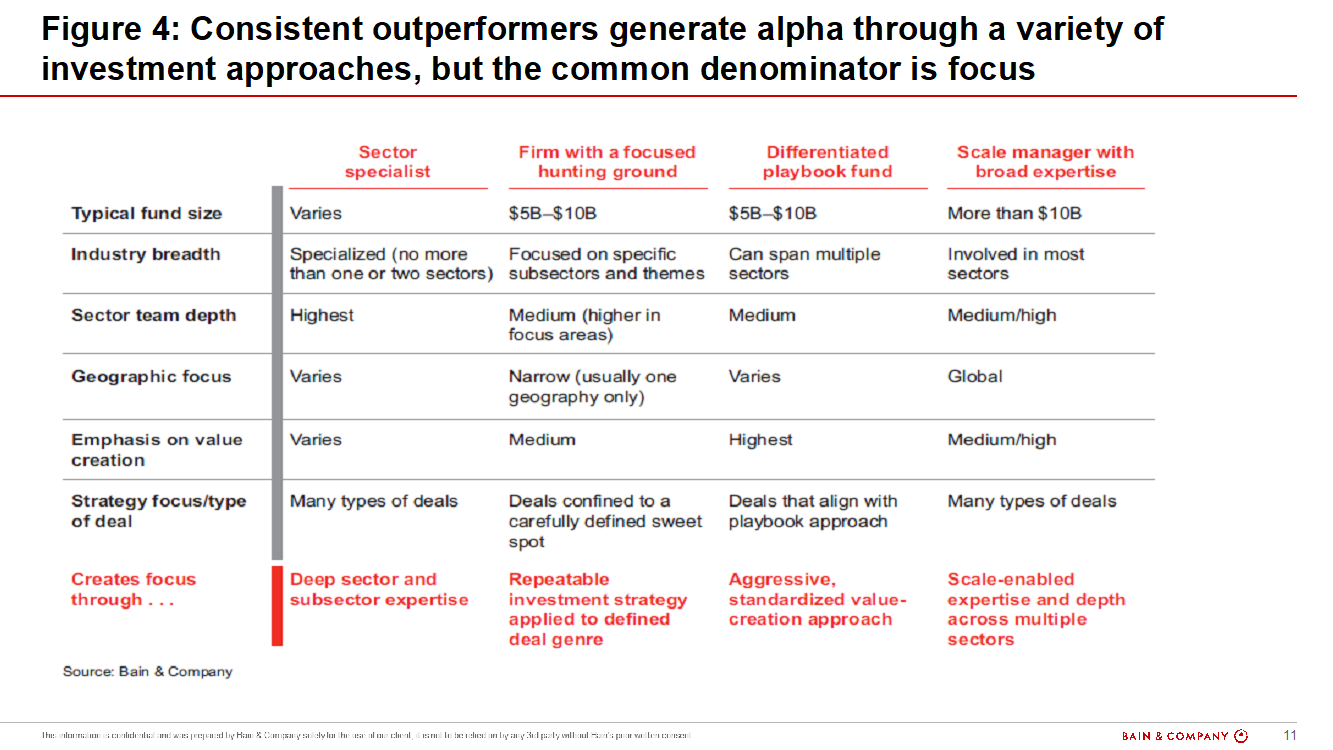

Bain’s private equity experts recently studied a pool of 113 private equity firms that each have raised $5 billion or more since 2000. Only 28 of them were consistent outperformers, meaning at least 80% of their funds ranked in the top two quartiles of industry performance over that period. The common denominator was focus: The best firms know what they are good at and wield it as a competitive weapon.

Our consistent outperformers fell into four broad categories (see Figure 4).

- Sector specialists. These firms know more about a given sector than anyone else. They’ve become so smart in their area that they can assess risk and opportunities in ways competitors can’t. (Think Thoma Bravo, Silver Lake and Vista Equity in tech, Charlesbank and L Catterton in consumer.)

- Firms with a focused hunting ground. These firms target a sweet spot with a repeatable investment approach, but don’t limit themselves to one sector. They know exactly which risks to underwrite and are very comfortable managing them. They also know which risks they will never underwrite. Examples include MBK Partners, Equistone Partners Europe, Veritas Capital and Audax Group, which focuses on buy-and-build strategies.

- Differentiated playbook funds. These funds know from pattern recognition what kinds of companies they can improve and how. They have a well-defined playbook that works on companies with certain characteristics; by running it with great precision, they create significant value. Examples include Clayton, Dubilier & Rice and GTCR.

- Scale managers with broad expertise. Scale funds capitalize on their size and breadth. They bring massive resources to whatever they invest in and often do the biggest, most complex deals. Firms like Blackstone, KKR, CVC, EQT, Permira and Apax Partners have teams of people with deep expertise. They also have the staying power to wait out troubled investments that otherwise would go bust.

Focused firms win—and win consistently—because commitment to a formula sharpens all phases of the value-creation cycle. For middling firms, that begs several questions:

- Is your sweet spot clear and distinctive?

- Do you know a particular sector or geography better than anybody else?

- Can you confidently recognize patterns for value creation and deliver against them?

- Does your scale allow you to overwhelm the competition with more resources and staying power?

Competition from the public markets will ease eventually. But as limited partners continue to favor the industry’s top tier, PE funds have never faced greater pressure to outperform the average.

Interested in finding out more? Read Bain and Company's Global Private Equity Report 2020 for a deeper dive.