Posted by Rima Haddad on 01 October 2025

How active ETFs can help investors fine-tune portfolio construction

Actively managed exchange-traded funds are on the rise. In the short time since their debut in 2008, active ETFs have already topped $1 trillion in assets under management.1 This expansion has been driven by demand from investors attracted by active ETFs’ fusion of active management with the benefits of the ETF wrapper, which makes these funds a powerful portfolio-management tool.

The “active” in active ETF means these funds are managed by investment professionals with specific goals, which can include outperforming a benchmark, generating income and targeting a specific investment theme. The “ETF” tells you they offer the same advantages as all exchange-traded funds. They can be bought and sold at a known price on an exchange, just like stocks. They can be cost-effective and offer greater transparency on holdings.

This combination of attributes can make active ETFs a valuable addition to an investment portfolio. They offer investors an efficient, flexible way to gain exposure to equity and fixed income markets, including corners of these markets where structural inefficiencies make specialist research and rigorous bottom-up security selection essential, in our view. Innovative products such as derivative-income and buffer ETFs can allow investors to manage volatility while generating income.

We believe the active ETF market will continue to expand in the years ahead, and that the active component of these funds will be critical in driving market growth. The focus on delivering specific investment outcomes will intensify. This will result in a broadening range of targeted products offering access to new markets and asset classes and providing investors with increasingly sophisticated tools for portfolio construction and management.

The rise of active ETFs

Active ETFs grew slowly in the years following the first fund launch 17 years ago, but that changed in 2019, when the US Securities and Exchange Commission streamlined the process for bringing new ETFs to market.2 Among other changes, the so-called ETF Rule allowed for the use of custom baskets of assets. This gave managers greater flexibility to manage a fund’s underlying portfolio and liquidity, a crucial change that facilitated the development of active ETFs.

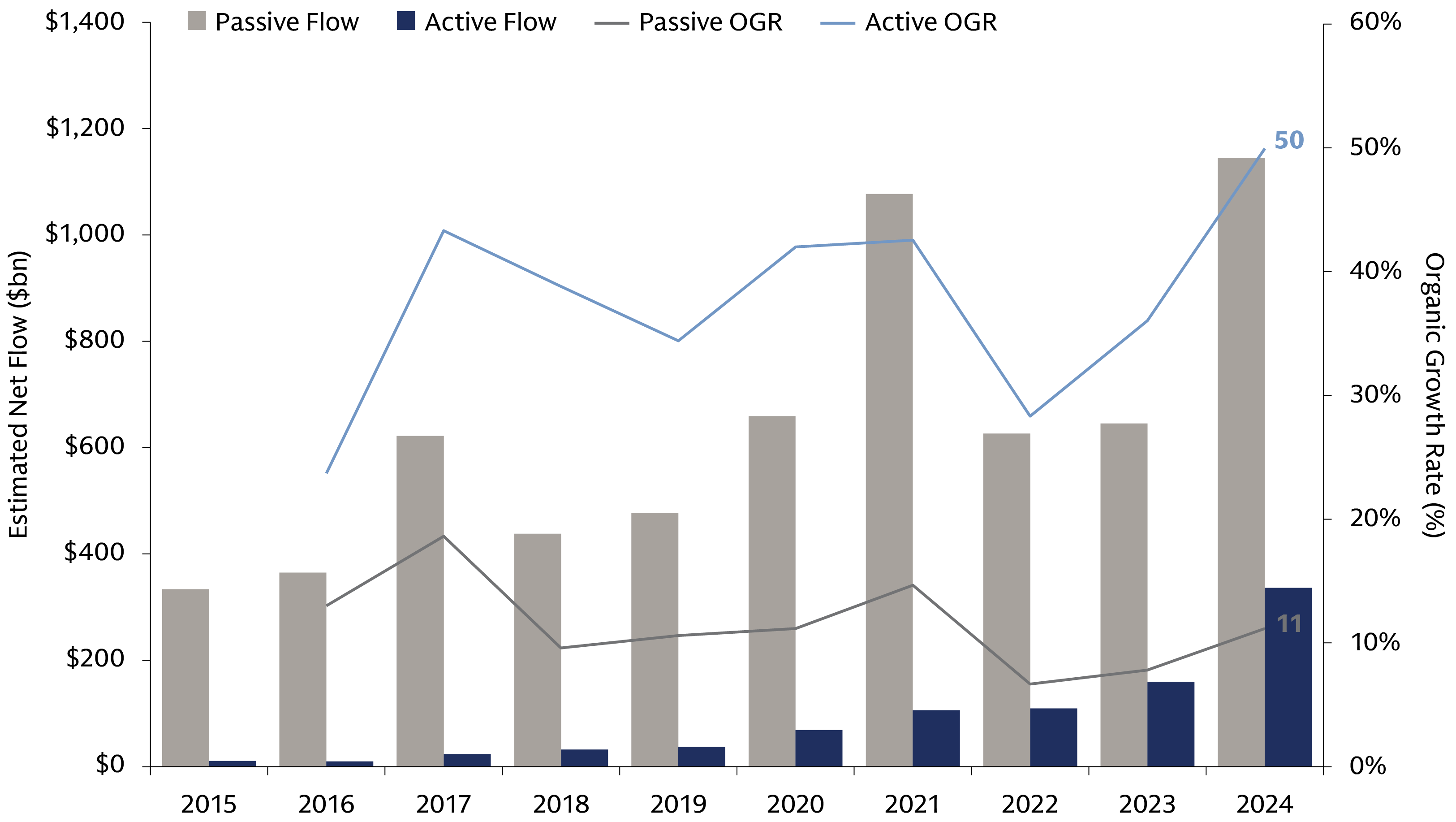

ETFs have been around for more than three decades, and during most of that time they have been associated primarily with passive investing and index-tracking funds. That is changing. Active ETFs accounted for just 7.8% of all ETF assets at the end of 2024, but they grew almost five times faster than their passive peers, fuelled by a surge in global net inflows to $339 billion.3

Actively managed ETFs are on the rise, fuelled by a surge in global investor demand

Source: Morningstar, Goldman Sachs Asset Management. As of December 31, 2024.

Enhancing portfolio diversity and efficiency

For investors who are familiar with active investing through mutual funds, active ETFs deliver many of the same potential benefits, such as in-depth research and dynamic management with the goal of outperforming a benchmark. In addition, they offer the advantages of the ETF vehicle, including intraday trading, portfolio diversification and the potential for lower costs.

For investors who are familiar with ETFs as a passive strategy through index-tracking and rules-based funds, active ETFs offer access to the alpha potential, robust security selection and engagement with portfolio companies that an active manager can bring, without sacrificing the benefits of the ETF vehicle.

Thanks to this unique combination of attributes, active ETFs can provide an efficient complement to existing allocations that allows investors to diversify their portfolios. The solutions they offer may help investors who are seeking to manage market volatility and also outperform the market. Active security selection can allow investors to avoid the concentration issues facing many passive investment products that track indices whose performance is driven by a small percentage of stocks.

The ease of buying and selling an active ETF makes these products efficient tools for short-term and tactical investments. This could benefit an investor who has committed to a private equity investment, for example. While they wait for their capital to be called and deployed, the investor could put it to work through an active ETF and sell the exposure quickly when their capital is called.

Active ETFs could also be a versatile component of a model portfolio, which provides a framework for pursuing an investor’s objectives as they evolve over time. As part of a diversified asset allocation that balances risk and return, active ETFs may also be used to expand an investor’s investment options. For example, derivative-income ETFs provide the potential to generate income from equity markets that is independent of the interest-rate movements that impact yield in fixed income.

Industry trends to watch

We expect ETFs to build on a record-setting 2024, when flows, assets under management and fund launches all posted significant gains. We anticipate these trends may continue in the years ahead as ETFs become the pooled vehicle of choice for many investors thanks to their ease of trading, transparency and cost-effectiveness.

We are watching three key trends that investors should be aware of. Active ETFs have become the fastest-growing part of the industry, and we see further expansion ahead. The market is dominated by US-listed funds, though investor demand in the rest of the world is increasing.4 In Europe, assets in active ETFs rose sharply last year to $56.7 billion.5

We think solutions-oriented ETFs are particularly well positioned for further development. We also expect to see the increased incorporation of ETFs, especially active ETFs, in model portfolios that many investors rely on to provide a road map toward their chosen investing destination.

The importance of active management

With new uncertainties around inflation, growth and international trade arising, in our view, investors have reasons to recalibrate their portfolios, and an active investment approach, diversification and sound risk management will be essential. The rise of active ETFs offers investors a flexible and efficient tool to diversify their portfolios and prepare them to take advantage of the potential opportunities that lie ahead.

Notes

1 Global assets under management in active ETFs rose to $1.075 trillion at end-2024 from $669 billion a year earlier. See “Global ETF Flows 2025,” Morningstar. Data as of December 31, 2024.

2 “SEC Adopts New Rule to Modernize Regulation of Exchange-Traded Funds,” SEC press release. As of September 26, 2019.

3 “Global ETF Flows 2025,” Morningstar. Data as of December 31, 2024.

4 “Global ETF Flows 2025,” Morningstar. Data as of December 31, 2024.

5 European ETF & ETC Asset Flows: Q4 2024,” Morningstar Manager Research. Data as of December 31, 2024. The USD figure given here is a conversion of EUR 54.4 billion in the Morningstar report as of December 31, 2024.

Risk considerations and disclosures

Exchange-Traded Funds are subject to risks similar to those of stocks. Investment returns may fluctuate and are subject to market volatility, so that an investor’s shares, when redeemed, or sold, may be worth more or less than their original cost. ETFs may yield investment results that, before expenses, generally correspond to the price and yield of a particular index. There is no assurance that the price and yield performance of the index can be fully matched.

Diversification does not protect an investor from market risk and does not ensure a profit.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

This material is provided for educational and informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this publication and may be subject to change, they should not be construed as investment advice.

Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

This material is for informational purposes only. It has not been, and will not be, registered with or reviewed or approved by your local regulator. This material does not constitute an offer or solicitation in any jurisdiction. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United States: In the United States, this material is offered by and has been approved by Goldman Sachs Asset Management, L.P., which is a registered investment adviser with the Securities and Exchange Commission.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA):

This financial promotion is provided by Goldman Sachs Asset Management B.V.

This marketing communication is disseminated by Goldman Sachs Asset Management B.V., including through its branches (“GSAM BV”). GSAM BV is authorised and regulated by the Dutch Authority for the Financial Markets (Autoriteit Financiële Markten, Vijzelgracht 50, 1017 HS Amsterdam, The Netherlands) as an alternative investment fund manager (“AIFM”) as well as a manager of undertakings for collective investment in transferable securities (“UCITS”). Under its licence as an AIFM, the Manager is authorized to provide the investment services of (i) reception and transmission of orders in financial instruments; (ii) portfolio management; and (iii) investment advice. Under its licence as a manager of UCITS, the Manager is authorized to provide the investment services of (i) portfolio management; and (ii) investment advice. Information about investor rights and collective redress mechanisms are available on am.gs.com/policies-and-governance. Capital is at risk. Any claims arising out of or in connection with the terms and conditions of this disclaimer are governed by Dutch law.

In the European Union, this material has been approved by either Goldman Sachs Asset Management Funds Services Limited, which is regulated by the Central Bank of Ireland or Goldman Sachs Asset Management B.V, which is regulated by The Netherlands Authority for the Financial Markets (AFM).

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Asset Management Schweiz Gmbh. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Asset Management Schweiz Gmbh, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited and in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

- Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

- Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

- Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

- Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

FOR DISTRIBUTION ONLY TO FINANCIAL INSTITUTIONS, FINANCIAL SERVICES LICENSEES AND THEIR ADVISERS. NOT FOR VIEWING BY RETAIL CLIENTS OR MEMBERS OF THE GENERAL PUBLIC.

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law (“FIEL”). Also, Any description regarding investment strategies on collective investment scheme under Article 2 paragraph (2) item 5 or item 6 of FIEL has been approved only for Qualified Institutional Investors defined in Article 10 of Cabinet Office Ordinance of Definitions under Article 2 of FIEL.

FOR INTENDED AUDIENCES ONLY – NOT FOR WIDER DISTRIBUTION

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

FOR INTENDED AUDIENCES ONLY – NOT FOR WIDER DISTRIBUTION

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser.

These materials are presented to you by Goldman Sachs Saudi Arabia Company ("GSSA"). GSSA is authorised and regulated by the Capital Market Authority (“CMA”) in the Kingdom of Saudi Arabia. GSSA is subject to relevant CMA rules and guidance, details of which can be found on the CMA’s website at www.cma.org.sa.

The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

FOR INTENDED AUDIENCES ONLY – NOT FOR WIDER DISTRIBUTION

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

FOR INTENDED AUDIENCES ONLY – NOT FOR WIDER DISTRIBUTION

Qatar: This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

France: FOR PROFESSIONAL USE ONLY (WITHIN THE MEANING OF THE MIFID DIRECTIVE)- NOT FOR PUBLIC DISTRIBUTION. THIS DOCUMENT IS PROVIDED FOR SPECIFIC INFORMATION PURPOSES ONLY IN ORDER TO ENABLE THE RECIPIENT TO ASSESS THE FINANCIAL CHARACTERISTICS OF THE CONCERNED FINANCIAL INSTRUMENT(S) AS PROVIDED FOR IN ARTICLE L. 533-13-1, I, 2° OF THE FRENCH MONETARY AND FINANCIAL CODE AND DOES NOT CONSTITUTE AND MAY NOT BE USED AS MARKETING MATERIAL FOR INVESTORS OR POTENTIAL INVESTORS IN FRANCE.

Compliance code: 457724-OTU-2363868

Date of first use: September 25, 2025