Is the market overreacting to the US-China trade war?

Ahead of RiskMinds Asia in Singapore this October, we asked Alicia Garcia Herrero, Chief Economist, Asia Pacific at Natixis to explore the market's reaction to the US-China trade war.

On July 6th, the US-China trade war fired the first round of tangible bullets on $34 billion worth of imports both from US and China sides. The financial market had been snubbing the risk of a trade war at the beginning, but such optimistic sentiment has dissipated since mid-June 2018. The escalation of the trade war has caused an abrupt fall across various stock markets, especially in China. Emerging market currencies are also under huge depreciation pressure from capital outflows.

To help evaluate whether the market response is warranted or exaggerated, this article aims at measuring the trade impact of additional import tariffs based on standard economic theory, namely two key parameters:

- Tariff pass-through rate: Under a tariff shock, an exporter with a certain monopoly power may not fully pass through the marginal cost to the local price. For example, for a 25% tariff, it is possible for an exporter to raise the price by 5% (denominated at local currency) and reduce its profits for another 20%.

- Price elasticity of demand: With a price hike from import tariffs, US consumers will reduce its demand for the product. A usual elasticity above one indicates a more-than-one-to-one adjustment of the exports than prices.

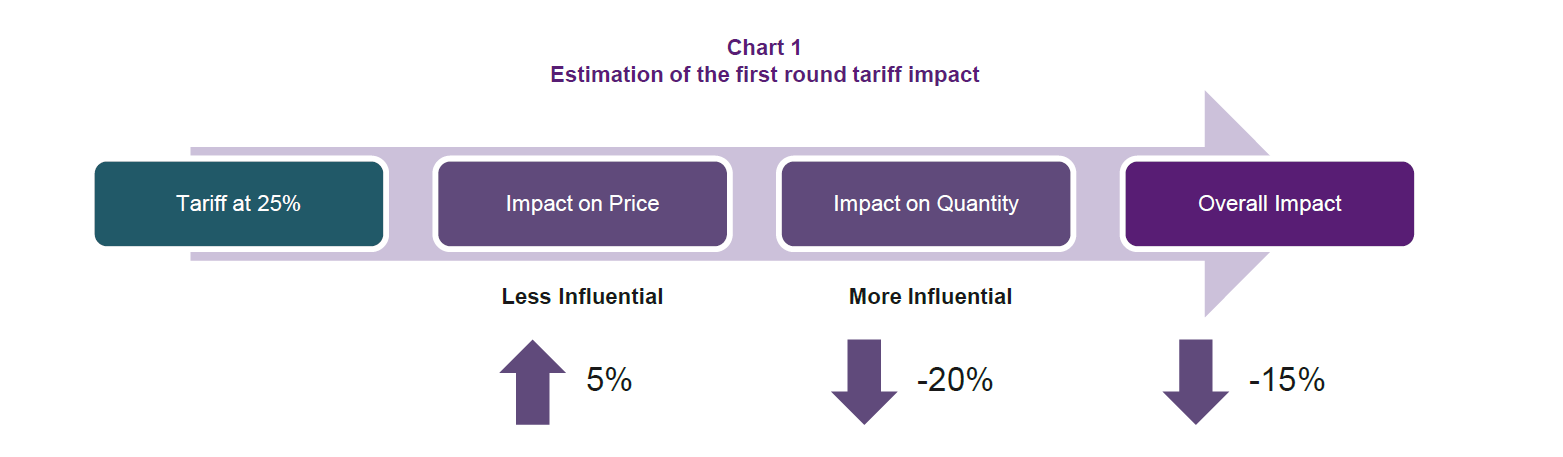

Limited impact of the first round tariffs

The existing trade theory offers a few empirical estimates of these parameters, which can help us understand the magnitude of the impact of import tariffs. A detailed description of some of the estimates is summarized in Table 1.

First, the tariff pass-through rate is usually low, ranging from 10% to 30%. We take a mid-point of 20% for our calculation. That said, from a rough estimate multiplying the tariff pass-through rate (20%) by the tariff rate (25%), a 5% price increase would be induced for the targeted products in both China and the US. Second, the price elasticity of demand is typically more influential. The average estimate is between 2 and 6, and we again take the mid-point of 4 for estimation. This means 1% change in price will reduce 4% in demand. As such, the induced 5% increase in price would reduce the import quantity by 20%, and thus the import value by 15% (20% - 5%).

However, we believe the real impact may be even smaller than 15%. One point that the above analysis overlooks is trade is not only bilateral but other countries can substitute. In other words, the effect stemming from the substitutability of imports by third countries can offset the reduced imports from China or the US (1). The choice of products for the US is to avoid the goods which are hard to substitute immediately, and therefore the price impact is even smaller, especially for the US side.

Admittedly, the product affected by the tariffs may also pass through to other industries via the vertical industry linkages, possibly exacerbating more general price hikes. For example, a hike in steel price may cause rising construction service prices. But on the other hand, the rising cost may also squeeze the profits for the downstream sectors, which might lead to reduction in the price of the intermediate imports in some industries. So far, there is no consensus among economists on the ultimate effects of the additional industry linkages. The usual convention is that the general equilibrium effects might not change the magnitude of our baseline results. (As Krugman (2018) put it, “trade policy analysis using partial equilibrium – ordinary supply and demand – usually gets you more or less the right answer”).

All in all, the trade impact of the first round of the tariff should have a very limited impact on China’s exports to the US, with the maximum loss of $5 billion (15% of $34 billion). There is leeway that both countries can take with the rerouting through the third countries at this stage, such as exporting through Hong Kong or other locations with free trade agreement with either side. Therefore, the impact on both countries’ aggregate external trade will be even smaller. In this scenario, the trade impact of the first round tariff is tiny for both countries. The real worry should instead be the continuous escalation through additional tariff measures. Beyond trade, further investment restrictions, and probably a full-fledged technology arm race, would bring even more uncertainties to the world.

Read the original note here >>