Private debt in 2018: the has-been trends and the rising stars

There has been a significant change in the activities within the private debt market in the first quarter of 2018. Mezzanine and distressed lending have become the favourites, with direct lending activity remaining muted for the first time compared to the previous five years. Special situations funds, having attracted the most capital, has become the rising star in the private debt market. Raelan Lambert, speaker at SuperReturn Private Credit US 2018, gives us an update on the developments in the private debt space.

There has been a significant change in the activities within the private debt market in the first quarter of 2018. Mezzanine and distressed lending have become the favourites, with direct lending activity remaining muted for the first time compared to the previous five years. Special situations funds, having attracted the most capital, has become the rising star in the private debt market. Raelan Lambert, speaker at SuperReturn Private Credit US 2018, gives us an update on the developments in the private debt space.

Deal Flow

Private debt activity continues its five-year increasing trend and remains up year-over-year for the first quarter of 2018, with distressed and mezzanine raising more than direct lenders. The uptick in mezzanine is interesting, as many private debt managers and limited partners we engage with emphasise their focus on assets that are at the top of the capital structure.

What the Q1 2018 data may suggest, however, is that M&A activity may be a driver as incremental financing for companies that mezzanine lenders know well (and may have previously funded) prompts them to take a more subordinated position in the capital structure (and garner a higher yield at a time when yields have compressed dramatically). It may also suggest that the trend toward unitranche lending continues to increase. Given unitranche effectively blends senior and subordinated risk into one security, its placement in the capital stack is blurred and is likely inaccurately tracked in the data.

Another significant driver of deal flow is refinancing activity, which has been prolific. According to J.P. Morgan, refinancing composed approximately 75% of total new loan issuance in 2017, the most on record since 2009. Refinancing activity is the single most concern we hear managers cite in our discussions. Their concern is that it means a hypothetical $1 billion fund planning for a three-year loan tenor is now facing 12 month holding periods (and sometimes shorter), so they must deploy that capital 2.5 times to 3.0 times over the course of a three to four-year investment period.

Call protection is, therefore, imperative. As without it, private lenders are faced with finding a new company to lend to in an increasingly competitive environment characterised by compressing yields, ample liquidity and as a result, potentially inferior quality deal flow as covenants remain largely absent.

Fundraising

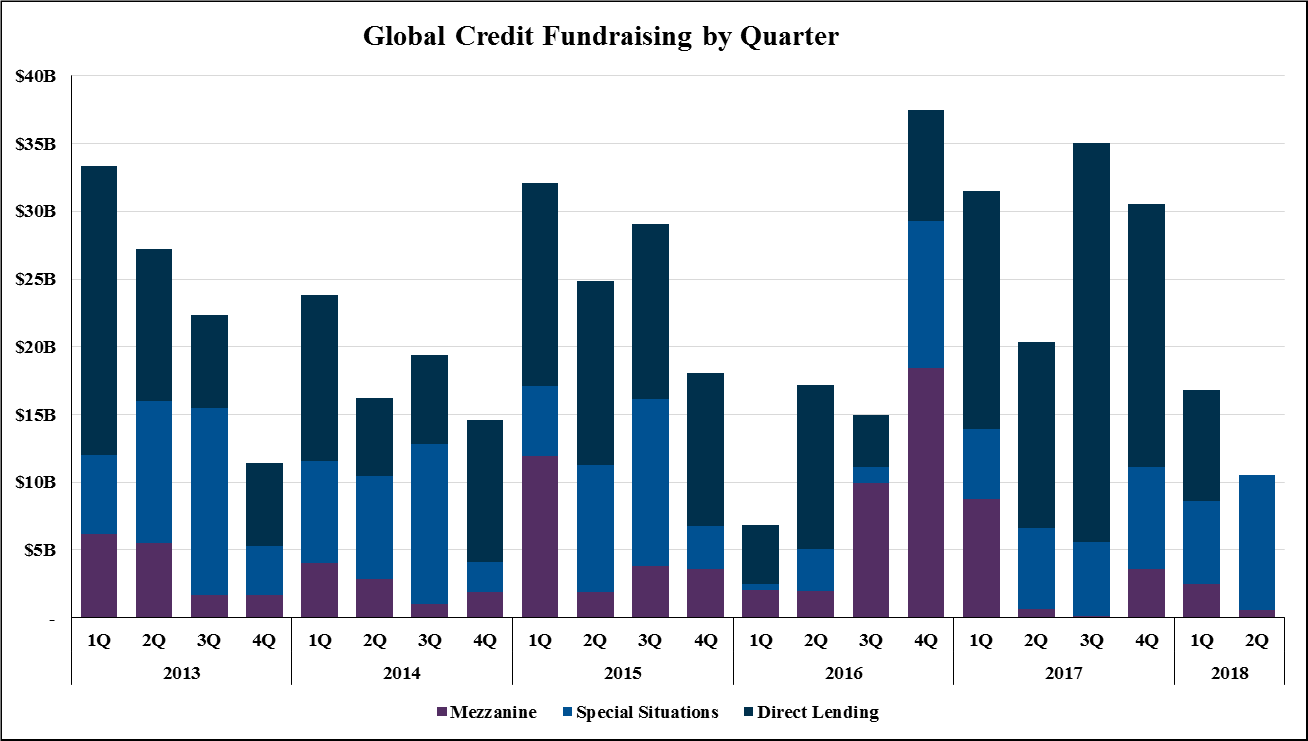

Whereas fundraising activity in 2017 was dominated by direct lending, Q1 2018 demonstrated that investors may be starting to take pre-emptive action in response to the risks building up, including the potentially “false safety” of some senior direct lending.

According to S&P, the amount of first lien debt is growing, which may erode recovery prospects for senior lenders. Lenders who underwrote deals poorly may face a situation where they might need to restructure their debt into more flexible structures, such as PIK toggles. This in turn reduces current income distributions to limited partners and delays the recovery of principal, or can even lead to its impairment in severe cases.

Special situations funds have attracted the most fundraising capital to-date in 2018, and we expect this trend to continue as rising interest rates and inflation strain weaker companies that may be unable to bear the heavier interest rate load. While nearly all private loans are floating rate instruments (coupon rates increase as interest rates rise), this feature is only as protective as long as companies can pay their coupons at the higher rates. Special situations managers will benefit from companies who find themselves in misaligned capital structures if growth slows, revenue declines and profit and cash flow margins compress.

SMAs & Leverage

There are two other factors not necessarily reflected in the fundraising figures that give us caution: (i) separately managed accounts (“SMAs”) and (ii) fund-level leverage. Fundraising data largely omits capital that is raised alongside commingled funds on behalf of specific mandates privately negotiated between fund managers and limited partners. SMA capital can be quite material in some cases, as many of the direct lenders raising funds today started after the Global Financial Crisis by way of SMAs. This additional capital is important because it adds to the amount of commingled fund capital the manager needs to deploy, and may put further pressure on the fund manager’s sourcing engine, which is already being strained by refinancing activity and competition with “volume” lenders who are driving yield compression and covenant relaxation.

Fund-level leverage is a prominent trend pervasive in the market and is fuelling both deal activity (managers can now deploy more with less equity) and fundraising (LPs can now garner higher net returns as their equity is magnified by fund-level debt). However, the disparity between managers’ usage of debt, articulation of the risks, and reliance on historical bank behaviour is alarming. Investors are encouraged to tread cautiously – as isn’t it strange that the return for a top quartile direct lending fund is 13.6% while the top quartile return for an opportunistic/special situations fund is 15.3%?

---

Important Notice Issued by Pavilion Alternatives Group®, which operates through Pavilion Alternatives Group, LLC, Pavilion Alternatives Group Ltd., Pavilion Alternatives Group (Singapore) Pte. Ltd. and a division of Pavilion Advisory Group Limited in Canada. Pavilion Alternatives Group, LLC and Pavilion Alternatives Group Ltd. are both registered investment advisors under the Investment Advisors Act of 1940 and the Form ADV Part II for Pavilion Alternatives Group, LLC and Ltd. are available upon request, and must be provided to prospective clients at least 24 hours prior to executing a contract. Pavilion Alternatives Group Ltd. is authorized and regulated in the UK by the Financial Conduct Authority and Pavilion Alternatives Group (Singapore) Pte. Ltd. is regulated by the Monetary Authority of Singapore. Pavilion Alternative Group Ltd. advises only clients who are, or agree to be treated as, Professional Clients as defined in the Financial Conduct Authority’s Conduct of Business Sourcebook. This document should not be distributed, published or reproduced, in whole or in part nor should its contents be disclosed by a recipient to any other person. This document has been prepared solely for the recipient and it may not be reproduced, in whole or in part not should it be transferred to any other person or used for any other purpose without the written consent of Pavilion Alternatives Group®. Pavilion Alternatives Group is a registered trademark of Pavilion Financial Corporation used under license by Pavilion Alternatives Group, LLC in the U.S., Pavilion Alternatives Group Limited in the UK, Pavilion Alternatives Group (Singapore) Pte. Ltd. in Singapore, and Pavilion Advisory Group Ltd. in Canada. © 2018 Pavilion Alternatives Group®