Private equity wakes up to the industrials opportunity

For private equity investors, the question is no longer whether industrials matter. It’s whether the market has fully recognized their value-creation potential—and who is best positioned to capture it.

Ahead of SuperReturn International, Brookfield Private Equity CEO Anuj Ranjan explores the tailwinds driving industrial opportunities and why expanding margins through operational improvements is now imperative for driving returns.

Some of the most attractive private equity investment opportunities today can be found in market-leading industrial companies that create products customers can’t do without—such as car batteries, freeze-resistant pipe coating and cardboard box machinery.

These are not traditional growth stories. They are durability stories, defined by pricing power, entrenched market positions and consistent cash flow. Within this sector, businesses with mission-critical products and deep customer relationships offer the most value.

At the same time, many of these companies have reached an inflection point. Operational transformation expertise and artificial intelligence (AI) innovation are creating upside opportunities that the market has historically undervalued.

In a sense, industrials have been hiding in plain sight for years as investors gravitated toward flashier technology companies. That dynamic is reversing. With volatility rising amid geopolitical tensions and concern that AI could disrupt some software business models, investors are increasingly shifting their attention to manufacturing companies.

This is known as the HALO trade, or “heavy assets with low obsolescence.” Examples include essential industrial products, critical supply-chain components, oil and gas pipelines, and railroad networks. These businesses tend to operate in regulated markets with high barriers to entry, producing often technically complex products that last for years with high replacement costs.

For Brookfield, HALO is not a new discovery. We have invested in industrials as a core part of our private equity strategy for 25 years, owning and operating essential businesses across the real economy. We have seen first-hand that industrials require significant time, capital and expertise to manage successfully and are built to endure across market cycles, not just outperform within them.

A convergence of tailwinds

Industrials are benefiting not just from positive sentiment but from an alignment of multiple structural tailwinds:

- Portfolio rationalization is accelerating

Globally—but particularly in the U.S. and Europe—conglomerates are shedding noncore assets, including industrial businesses that require reinvention but lack the capital and expertise to transform. This dynamic is creating compelling carveout opportunities, especially in sectors such as building products, specialty chemicals, aerospace and defense, the automotive aftermarket and capital goods.

At the same time, public market volatility is driving many industrial management teams toward privatization, recognizing that meaningful transformation requires a long-term outlook rather than quarter-over-quarter earnings scrutiny. This has created attractive take-private opportunities for private equity managers. - AI-led digitalization is moving from concept to capability

Artificial intelligence has emerged as a critical transformation lever globally, especially for manufacturing companies that are among the world’s least digitized assets. For these businesses, AI models will increasingly play an outsized role in cutting costs, addressing labor shortages, upgrading product lines and optimizing supply chains. In fact, some are calling this the Fourth Industrial Revolution. Industrial leaders can adopt AI to extend their advantages, while more commoditized players must implement AI to simply survive. - Deglobalization is reshaping supply chains

For decades, industrial companies opted for the lowest-cost solutions—such as just-in-time deliveries—to acquire the raw materials needed to make their products. These preferences led to complex and globally fragmented supply chains.

Successive shocks—Covid, Ukraine, tariffs and the Middle East conflict—have elevated supply-chain resiliency to a board-level priority. The current environment reinforces why companies are continuing to reshore critical operations and localize supply chains. This transition requires capital, strategic planning and execution expertise—areas where private equity is well positioned to play a central role. - The AI infrastructure buildout is creating downstream demand

Total spending on AI-related infrastructure is expected to exceed $7 trillion in the next 10 years, including investments in chips, data centers, power plants and transmission lines. But for that level of spending to pay off, industrial businesses must translate it into real productivity gains.

As AI expands and costs fall, it will enable widespread adoption across manufacturers to optimize supply chains, improve product yield and enhance predictive maintenance. These gains, which we estimate will exceed $2 trillion annually, will ultimately help justify the sizable infrastructure investment.

The companies that benefit from these gains won’t just be the technology platforms building the AI models but, importantly, the industrial companies adopting AI to reinvent their operations. Individually, these trends are powerful. Together, they are creating a rare industrial transformation window.

Operational excellence in the new private equity era

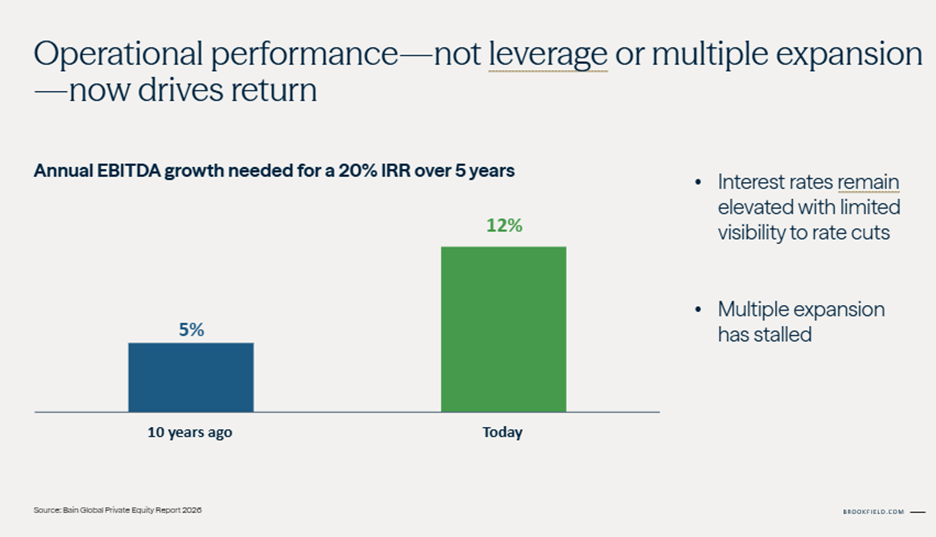

The common denominator for capitalizing on these trends is operational expertise. When interest rates were low and debt was cheap, private equity managers benefited from market growth and expanding multiples.

That era has passed. With today’s higher borrowing costs and lower leverage, value creation now requires operational improvement and margin expansion.

The latest Bain Global Private Equity Report reinforces this reality. In the report’s “12 is the new 5” analysis, Bain notes that a hypothetical buyout a decade ago with a 6-7% interest rate required 5% earnings growth to achieve a 20% return over five years. That same buyout today, with an 8-9% interest rate and less leverage, would require more than twice the earnings growth—in the 12% range—to achieve that same outsized return.

In other words, we’ve moved from roll-the-dice private equity to roll-up-your-sleeves private equity. Managers that consistently expand margins - through productivity gains, digital transformation and commercial execution - will be best equipped to deliver attractive outcomes.

Industrials: From overlooked to essential

Short- and long-term trends are converging to create a favorable industrials outlook, drawing increasing attention from private equity managers.

Carveouts and take-privates are on the rise, companies are rebuilding supply chains and AI is beginning to modernize some of the world's most critical—but least-digitized—businesses. Over the long term, AI’s unstoppable advance will help outdated industrials transform into more nimble global competitors.

This is not a cyclical opportunity. It’s a structural reinvention of the industrial economy.

For private equity investors, the implication is clear: The next phase of industrial value creation will require expertise to modernize, operate and grow the businesses that keep the real economy running, positioning them to compete for decades to come.

Endnotes

- Estimated capital requirement over the next 10 years based on Brookfield internal research.

- Internal Brookfield estimates.

Disclosures

This commentary and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, a solicitation of an offer to buy, or an advertisement for, any securities, related financial instruments or investment advisory services. This commentary discusses broad market, industry or sector trends, or other general economic or market conditions. It is not intended to provide an overview of the terms applicable to any products sponsored by Brookfield Asset Management Ltd. and its affiliates (together, "Brookfield").

This commentary contains information and views as of the date indicated and such information and views are subject to change without notice. Certain of the information provided herein has been prepared based on Brookfield's internal research and certain information is based on various assumptions made by Brookfield, any of which may prove to be incorrect. Brookfield may have not verified (and disclaims any obligation to verify) the accuracy or completeness of any information included herein including information that has been provided by third parties, and you cannot rely on Brookfield as having verified such information. The information provided herein reflects Brookfield's perspectives and beliefs.

Investors should consult with their advisors prior to making an investment in any fund or program, including a Brookfield-sponsored fund or program.