The push for sustainable infrastructure

Nick Langley, Managing Director, Portfolio Manager of ClearBridge Infrastructure Strategies, shares his views on how proliferating green new deals and the need to lower carbon emissions will drive investments and returns in infrastructure.

ClearBridge Investments were a recent sponsor of the IM|Power 2020 event. Two of ClearBridge team members, Elisa Mazen and Nick Langley, the author of this article, spoke at the event.

- Infrastructure will require substantial investments for the world to advance on lower carbon emissions targets and is well-positioned for the growing interest in stakeholder capitalism.

- While public policy will play a significant role in funding lower-emission infrastructure, we expect the world will rely on the private sector to fund many initiatives, likely with user-pays and regulated infrastructure.

- We believe it will be advantageous to be in the listed infrastructure space where capital can be allocated nimbly as public policy develops and global trends affect asset values.

The COVID-19 pandemic has meaningfully hit most countries in the world, bringing with it a toll on human lives and livelihoods. As governments mitigate the public health crisis and support economies through monetary and fiscal policy, infrastructure investment as a means of stimulus will rightly focus on smaller projects aimed at getting money into various smaller communities and regional centers.

Yet the need to lower carbon emissions is not going away; nor is the importance of upgrading and building new infrastructure to achieve lower emissions targets. And part of the world’s response to the pandemic, increasing the urgency of considering the needs of all stakeholders in planning business operations, also looks to be a positive for infrastructure’s outlook.

Infrastructure companies are well-positioned to manage a balance of stakeholder and shareholder interests that is a key tenet of the corporate response to the pandemic. They have done this for a long time. A utility, for example, interacts closely with a regulator, which, as one of its key stakeholders, looks after the customers who are connected with the utility. We expect many other corporations will look to the infrastructure sector to understand how best to undertake this approach going forward.

Green New Deals and the momentum for lowering emissions

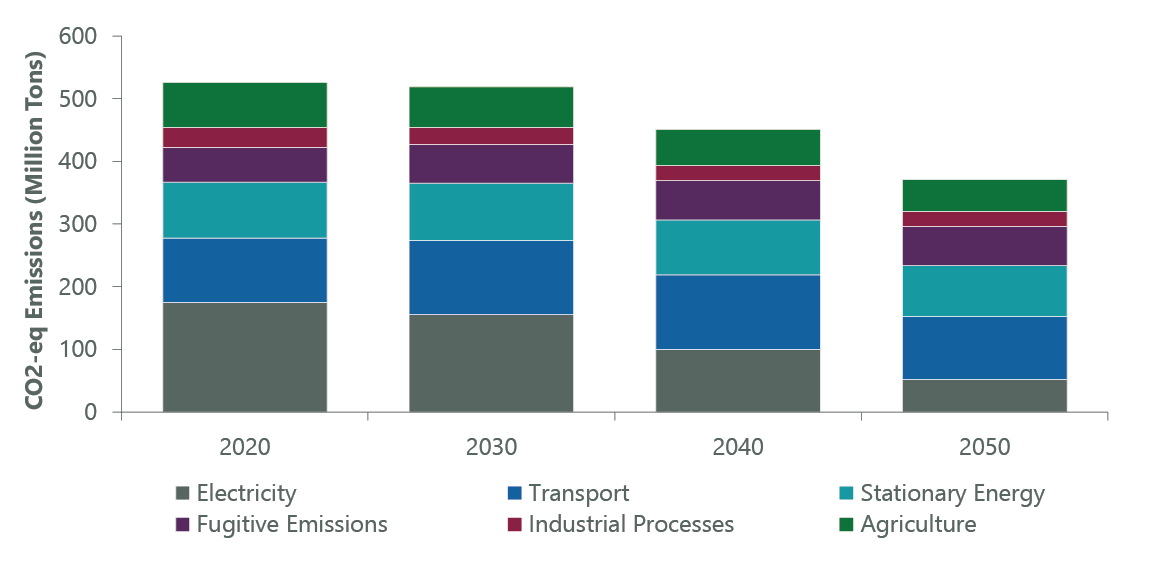

Globally, climate change is registering more and more as a critical concern, and taking climate change seriously will require substantial investment. In Australia, for example, under a business-as-usual emissions forecast, we see a considerable reduction in emissions. The decrease, which will be nowhere near net-zero by 2050, is mainly attributable to projected lower emissions in the electricity sector (Exhibit 1).

Missing from this scenario, however, are the tremendous opportunities for reducing emissions in other sectors. To meet net-zero 2050, the world will have to invest in reducing emissions in infrastructure.

Exhibit 1: Plenty of Room for Emissions Reductions Outside Electricity

Source: Energetics, Dr Gordon Weiss, 2019. Under business as usual, which assumes no new policy measures nor economic disruptions, particularly through the rise of new technologies. The forecast includes the impact of the Victoria Renewable Energy Target and Queensland Renewable Energy Target. Excludes Waste & Land Use related (de minimis and largely offsetting).

We expect a significant global push for a commitment to zero emissions by 2050 as more and more state entities make commitments. Europe, in particular, has comitted to going green on electricity generation via renewables, electric vehicles and energy conservation.

Climate change initiatives focused around repairing and upgrading infrastructure around the building sector are compelling. The U.S. loses 7,000 Olympic size swimming pools of water every day from leaking pipes and burst water mains. Bringing water infrastructure up to standard will require a massive amount of capital. Buildings will need to be made more efficient, and transport, manufacturing and agriculture sectors will also require significant investment.

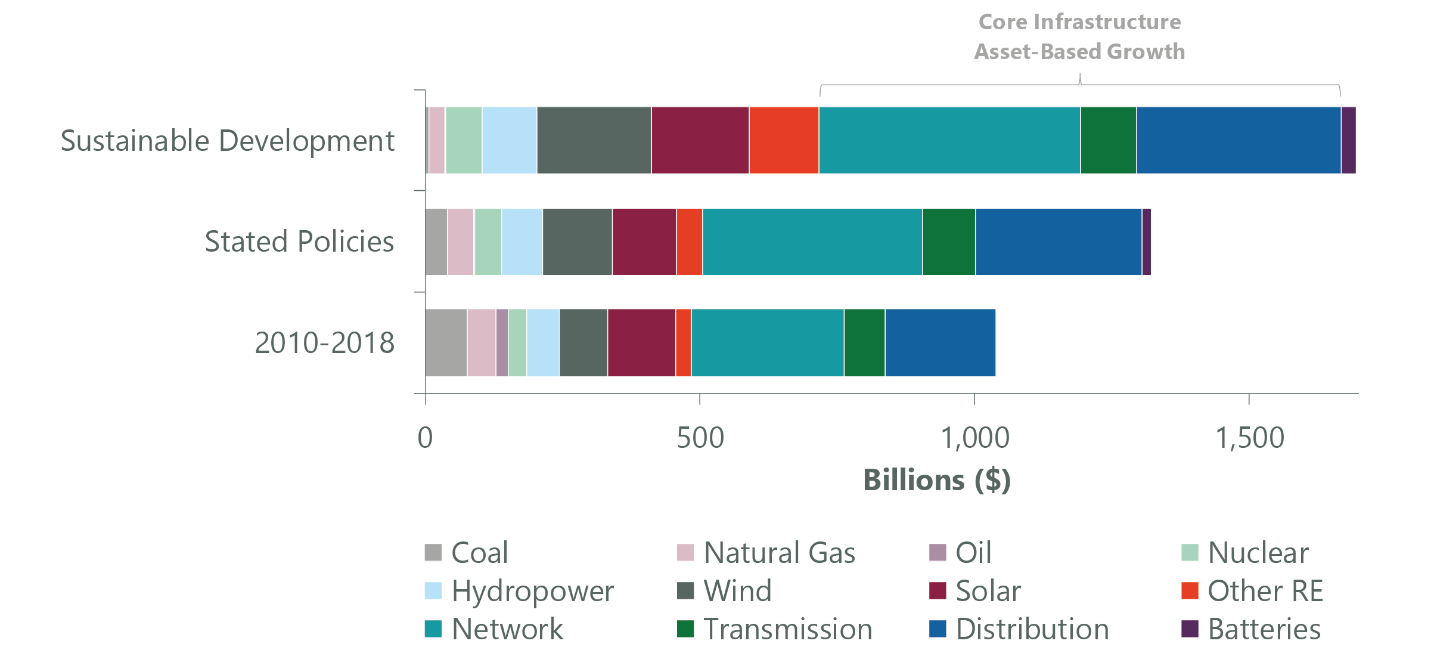

How much investment will be needed? The International Energy Agency produces an annual report on the projected amount of capital required in energy networks globally. The report focuses on two different cases: a stated policies case, i.e., that suggested by current policies, and a sustainable case, which accounts for spending required to lower emissions enough to keep with the UN’s climate change target of 1.5%–2% of warming. The first case sees roughly $1.3 trillion being spent annually over the next 20 years; the sustainable case would need $1.7 trillion (Exhibit 2).

Exhibit 2: Global Annual Average Power Sector Investment.

As of Nov. 21, 2019. Source: International Energy Agency. In constant 2018 U.S. dollars (billions).

Much of this spending will be on network, transmission and distribution and will be concerned with changing the way we use electricity and gas and other energy grids. This will mean growth in the underlying asset base for infrastructure companies and regulators, providing attractive returns to equity holders to help fund that growth. It is these areas, in particular, we think infrastructure investors should be most interested in and excited by.

While public policy will play a significant role, we expect the world will rely on the private sector to fund many of these initiatives with user-pays and regulated infrastructure. The policy response to the COVID-19 crisis — increased government borrowing and central bank balance sheets — is reinforcing central banks’ accommodative stances and resulting in lower-for-longer interest rates.

Lower rates offer upside to utilities P/Es, and we think these companies will be better able to attract capital to spend on their networks to help effect some of the network adaptation and mitigation against climate change moving forward. We believe this will help utilities act as a critical element of the private sector lining up to help fund much of the global infrastructure spending needed to combat climate change.

Infrastructure opportunity will not be uniform

A specialized knowledge of the infrastructure sector, with a rigorous approach to ESG analysis, will be necessary to manage risks and capitalize on opportunities as green infrastructure grows. The direction of public policy over time should have a large impact on the valuations, for example of pipeline companies. A corollary insight might apply to toll roads, where the growth of autonomous vehicles, rather than requiring many new roads to be built or stranding existing roads, will markedly increase capacity on existing roads, increasing their value.

In the listed markets, there is some volatility from time to time, as we have seen through the pandemic. But over the long term, the returns allowed by the regulators have come through in the returns reported by the companies and the returns received by investors. This gives us, as investors, confidence that as a bow-wave of investment into infrastructure to support climate change initiatives grows, we will see appropriate returns for shareholders.