Posted by Sherry Madera on 01 March 2021

Will this be the year of the Green Ox in Asia?

As the Chinese new year begins, and the country recovers from the worst of the COVID-19 pandemic, will the Year of the Ox become synonymous with ESG and the 'going green' of the Asian investment management landscape.

Sherry Madera, Chief Industry & Government Affairs Officer, London Stock Exchange Group explores.

Will the Niu year bring fortune in green finance?

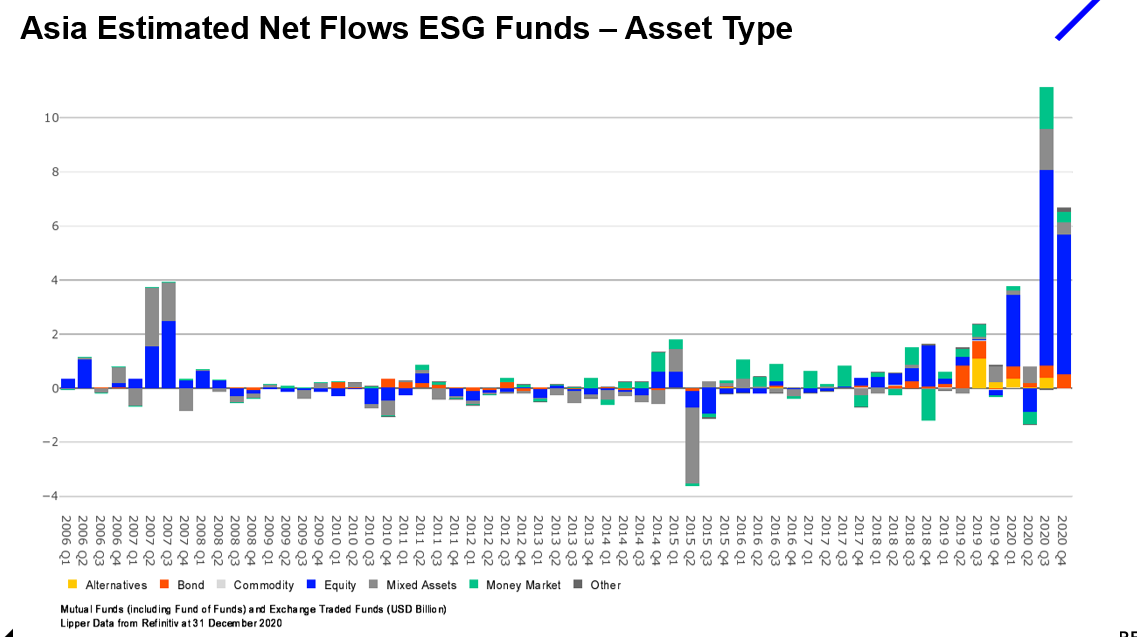

Global fund flows into ESG investments have skyrocketed in 2020 compared to 2019 with the global pandemic seeming to accelerate the trend. For example, U.S. ESG mandated assets under management (AUM) rose by roughly $5 trillion in just two years, according to data from Refinitiv.

Investor demand for sustainable investing is also evidenced in Asia. In fact net flows into ESG funds in Asia hit an record high in 2020, with tens of billions pouring in, according to Lipper data.

Asia Pacific deal making involving sustainable companies accounted for 40 percent of mergers and acquisition activities for the first half of 2020 by deal value, with China accounting for 20 percent of total sustainable deal making activity during this period by number of deals.

What will 2021 hold for sustainable investment in Asia? All of the indications point towards an increasing trend to sustainability. Some trends to watch are as follows.

Regulation – China moves to mandatory disclosures – who will follow?

A decade ago, few would have anticipated that China would be a pioneer in green finance. Today, China is one of the largest markets for green bonds as well as being home to an array of other green finance products, such as green funds, insurance products, ETFs and ABSs.

ESG information disclosure in China consists of mandatory disclosure for pollutants, voluntary disclosure guidelines, and voluntary disclosure by listed companies in annual reports and social responsibility reports.

We’ve seen the Chinese regulators begin to detail the mandatory disclosure requirements for listed companies on their environmental information. China’s stock exchanges have also issued market guidance for information disclosure. ESG awareness, monitoring and disclosure in China are on track to accelerate and drive the market to new heights.

These trends all sounds promising for both the financial industry and the planet. However, there are some bear traps to watch for so that our Green Ox does not stumble.

As a result, an increasing number of Chinese companies now release annual ESG reports. In 2019, 85% of Chinese Securities Index (CSI) 300 companies did so, an improvement from 54% in 2013. Good news, but there is more to do. Only 12% of those companies that disclose ESG data have audited reports. On average the scope and quality of ESG disclosures among CSI300 companies in Mainland China are ranked lower than companies that are part of the major stock market indices such as FTSE and S&P.

Evolving Taxonomies – Taxomania? Or Global trend for good?

Currently, the EU Sustainable Taxonomy is often in the news. Less well know is the fact that China published its Green taxonomy (called the Green Bond Endorsed Project Catalogue) in 2015. There are many differences between these two taxonomies but also many encouraging similarities. Globally, taxonomies are developing quickly in various jurisdictions with varietals developing including transition-based taxonomies. Asia is joining the taxonomy trend.

Countries in the region, including Japan, Malaysia and Singapore, have announced plans to step up work on developing taxonomies. While we should all embrace the drive towards more specific definitions for sustainable finance – especially to eradicate greenwashing. However, we should strive to map these taxonomies to each other and their underlying data set requirements. Particularly a transparent mapping across Asia would help investment strategies to remain interoperable between jurisdictions.

Looking beyond the green bond

Many new investment products are hitting markets including Green ETFs, Green Private equity, green loans and other listed and unlisted products. This broadens the options for investors to implement their sustainable strategies. Asia would do well to keep up, to innovate and to create liquidity in local markets for new green financial products.

As we enter the year of the Ox, one thing is certain – sustainable investing has made an irreversible leap into the mainstream. Pairing this momentum with the view that Asian markets will recover ahead of the rest of the world, indicates funds will continue to flow into green investment categories across the Asian markets.

These trends all sounds promising for both the financial industry and the planet. However, there are some bear traps to watch for so that our Green Ox does not stumble.

Filling the data gaps and data holes

According to the latest report by the Future of Sustainability Data Alliance (FoSDA) in Dec 2020, 98% of Global Institutional Investors take ESG and sustainability data into consideration when deciding to invest in a company, yet nearly 83% cite data as the obstacle to effective assessment.

FOSDA’s report identified the challenges of lack of standardisation in company reporting and proposed recommendations that fall into 3 broad categories:

(i) An appeal for identifying and creating a path to filling ESG data gaps and data holes

(ii) A call to accurately map datasets to sustainability taxonomies and policies

(iii) An identified need to develop ESG data talent globally

On 17 Feb 2021, FOSDA announced the establishment of a Data Council. The Data Council will convene global data expertise – bringing together Refinitiv, S&P Global and Moody’s ESG Solutions Group, and other new members, to act as a much-needed industry and regulatory sounding board focused on the ESG data needs for a sustainable future.

Asia leading the COVID economic recovery may flood markets

There is good evidence already that Asian markets will recover economically more quickly than other regions. In Q3 2020, China returned to its pre-COVID GDP growth levels. The US is not predicted to return to pre-COVID levels until Q2 2021 at the earliest, and Europe lags significantly further behind.

Investment funds flowing to Asia from global centres seeking yield may flood the markets and cause valuations to be overinflated. Sustained demand for green investment options, could lead to perverse outcomes including increased risk of Asian greenwashing based on poor definitions of sustainable finance products and transparency of use of funds.

No one standard to rule them all

Fragmentation in standards of disclosure, global taxonomies and regulatory requirements will cause inefficiency and drag on the markets globally – this applies in Asia as well. The global markets are initiating work to create a global standard for some disclosures, but the work is not yet complete. TCFD continues to be a critical well-adopted framework to build towards globally useful standards – at least to lock in comparability if harmonization remains a while off.

As we enter the year of the Ox, one thing is certain – sustainable investing has made an irreversible leap into the mainstream. Pairing this momentum with the view that Asian markets will recover ahead of the rest of the world, indicates funds will continue to flow into green investment categories across the Asian markets.

While recognizing there is no such thing as Asia and each country and market will offer different opportunities, financial products and regulatory policies, the region looks generally set to thrive. With due focus on transparency and financial market prudence, it could be a very prosperous year for those investing in the Green Ox.