Accelerating venture climate investments in Southeast Asia

Did you know that Southeast Asia’s climate tech scene is booming? From soaring investments to corporate champions, discover how the region is greening its future. Yet, amidst the growth, challenges loom—like balancing returns with impact. Join us as we navigate the highs, lows, and regulatory twists shaping SEA's climate revolution.

Climate tech investing is on the rise in Southeast Asia (SEA). The sector is seeing growing interest from investors, with the share of climate tech deals as a proportion of all venture funding expanding from 3.2% in 2019 to 9.5% in 20231. The volume of climate tech equity deals also saw a compound annual growth rate of over 15% from 2019 to 2023[2], and almost 30 climate-specific funds with full or majority allocations in Southeast Asia have emerged since 2020, raising over $830M in committed capital[3].

Early-stage venture rounds (i.e. prior to Series B) historically account for most of the climate tech equity deals in Southeast Asia, consistently comprising an average of 85%[4] of deal volume in recent years, with only a handful of companies completing rounds surpassing US$100M[5]. These up-and-coming startups will require mid-stage funding support as they mature in the coming years. However, most climate-focused venture funds with full or majority allocations to Southeast Asia have an early-stage focus, with less than 15% of funds having raised more than $100M as at end-2023[6]. Later-stage funds including Decarbonization Partners, Leapfrog Investments, and GenZero have only partial allocations to SEA.

Energy corporates are also an active part of the climate tech landscape in Southeast Asia, mirroring a global trend. For instance, Banpu[7] and Schneider Electric have through their venture arms been actively allocating to climate startups in recent years, investing in distributed solar, carbon markets, cross-market battery optimization, battery recycling, and automated energy trading beyond their home countries. Thailand’s PTT[8] has begun joint ventures in submersible robotics, serving renewable energy corporates in offshore businesses across the region. Malaysia’s Petronas[9], Indonesia’s Pertamina[10] and PTT are also actively collaborating on methane emissions measurement in the region[11]. This propensity towards cross-border coordination suggests robust intra-ASEAN cooperation in the climate tech space as all stakeholders push towards Net Zero.

Given these dynamics, venture capitalists actively allocating to climate startups at the venture growth stage with a strong local presence in and understanding of Southeast Asian markets, as well as intimate relationships with corporate actors, are expected to play an increasingly important role in bridging the gap between early-stage climate tech startups and late-stage capital providers.

In addition to climate-focused funds and strategic corporates, climate investing in Southeast Asia still relies on the involvement of generalist VCs, which participated in over 80% of the climate tech equity deals[12] in 2023.

Generalist VCs primarily prioritize opportunities based on return profiles within fund lives[13] without substantially taking into consideration the abatement potential of specific technologies or platforms. The two parameters are unfortunately not always aligned. Models with high abatement impact, such as green hydrogen and carbon capture, can face more issues with lagging traction and low Technology Readiness Level (TRL) scores than in other more technologically mature sectors such as fintech and healthtech; and market size and adoption readiness play a significant countervailing role in investment decisions.

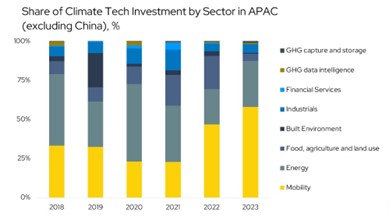

The consequence has been a delinking of decarbonization potential with investment allocation in this space. For instance, investment into mobility continues to grow in the region, rising from 23% of total climate tech investment in 2020 to 58% in 2023[14], taking priority over sectors with higher regional decarbonization potential such as peatland conservation[15]. SEA climate deals are also heavily skewed towards major markets, with Singapore and Indonesia accounting for over 90% of the total deal value in SEA in 2023[16], with the balance split between the Philippines, Vietnam, Thailand, and Malaysia; even though the latter group accounts for 2.92% of the world’s greenhouse gas emissions versus the combined 2.44% of the former[17].

To propel more effective participation by generalist, returns-focused VCs in climate investing, GPs need to be steered towards decarbonization impact, propelled by Governments and other strategic capital providers leveling up the potential returns profile for investments in hard-to-abate sectors. The sector is in urgent need of diverse de-risking financial instruments including but not limited to venture debt, working capital loans, and blended finance, coupled with strategic supporting initiatives such as Singapore’s Food Tech Innovation Centre that enable product innovation and commercialization with lower asset risk.

The success of climate tech startups is furthermore more uniquely tied to regulatory tailwinds relative to other sectors, given the market-creating nature of climate regulations. Europe and the US, for instance, have seen a rise in carbon accounting and ESG reporting platforms hoping to support disclosure requirements like the EU’s Corporate Sustainability Reporting Directive (CSRD) and Sustainable Finance Disclosure Regulation (SFDR), as well as the SEC’s 2024 climate disclosure rules. These new mandates have accelerated investments into climate software, evidenced by the latest rounds of funding into Watershed (US$100M Series C at a US$1.8B valuation in 2024) and Persefoni (US$50M C-1 in 2023, following a US$101M Series B in 2021). In Southeast Asia, the notable acceleration in mobility deals has similarly been fueled by favorable regulatory developments across the region, with incentive schemes in Singapore, Thailand, Malaysia, Indonesia and the Philippines and looming restrictions on ICE vehicles in Singapore (2030), Thailand (2035), Vietnam (2040), and the Philippines (2040) stoking investor interest in the space.

The climate tech space in Southeast Asia has room still to mature, with multiple uncertainties compounding risk in the space. Governments, asset owners, and investors alike play crucial but heterogeneous roles in ensuring that emerging climate innovation in the region is suitably supported and sustained.

References

[1]The State of Climate Tech in Southeast Asia 2023, DealStreetAsia.

[2]See footnote 1

[3] See footnote 1. Includes VC, growth, buyout funds. Excludes private credit and infrastructure funds.

[4] Median value of early stage (up to Series A+) deals as proportion of all climate tech equity deals within the year from 2019 - 2023. Source: Crunchbase, Openspace research.

[5] Including e.g. eFishery, Sunseap, SunCable, 800Super. Source: Crunchbase, Openspace research.

[6] See footnote 1.

[7] Banpu Public Company Limited, an energy solutions company operating in Asia Pacific and listed on the Stock Exchange of Thailand (SET).

[8] PTT Public Company Limited, a majority state-owned Thai oil and energy company listed on the SET.

[9] Petroliam Nasional Berhad, a Malaysia-headquartered multinational oil and gas company.

[10] PT Pertamina, an Indonesian state-owned energy company.

[11] Source: Petronas.

[12] By deal count. Source: Crunchbase, Openspace research.

[13]Typically, 10 years.

[14] State of Climate Tech 2023, PwC.

[15] As identified in Southeast Asia's Green Economy 2024 Report, Bain & Company.

[16] See footnote 1. First 11 months of 2023.

[17] European Commission - Emissions Database for Global Atmospheric Research.

Authors:

- Shane Chesson, Founding and General Partner, Openspace Ventures

- Jaclyn Seow, Director and Head of ESG, Openspace Ventures

- Claudia Zeisberger, Professor of Entrepreneurship & Family Enterprise, INSEAD

Want to hear more? Register for SuperReturn Emerging Markets now!