Defensive positioning into 2020: solving your US Large Cap Equity problem

By many metrics, the stock market may be considered overvalued, which presents investors and their advisors with a dilemma: how do you continue allocating to U.S. equities in a prudent way? Ed Lopez, Head of ETF Product, VanEck explores this crucial discussion ahead of Inside ETFs Florida next year.

You may not have realized it, but you have a large cap problem. The current bull market that started in March 2009 is now the longest bull market in modern stock market history. By many metrics the market could be considered overvalued, which presents investors and their advisors with a dilemma: how do you continue allocating to U.S. equities in a prudent way?

Forward-looking focus on valuation

At this point of the market cycle, it may be hard for some investors to justify putting new money to work in companies whose valuations have been stretched to elevated levels.

A more selective approach that seeks to allocate to companies trading at a lower relative valuation may provide more of a cushion in the event that markets take a tumble while also offering the potential for greater upside if equity markets continue to rise.

Traditionally, most valuation strategies are backward looking, in that they incorporate historical fundamental metrics such as earnings and book values to determine current valuations.

We believe valuations should also include an assessment of a company’s business and its prospects for future profit generation.

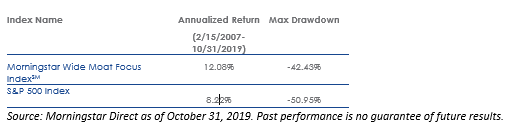

Morningstar Wide Moat Focus Index is designed to include companies with Wide Economic Moats, or companies Morningstar deems to have competitive advantages that are sustainable for at least the next 20 years.

The Morningstar Wide Moat Focus Index incorporates a forward-looking price-to-fair value metric to select at least 40 stocks trading at the lowest relative price, and rebalances quarterly. By including a forward-looking valuation metric into its investment thesis, investors may be able to better protect themselves from high-flying valuations, potentially boosting returns and allowing for a more favorable risk/return profile.

Tactical strategies may offer protection from sustained bear markets

One of the oldest, most popular applications of a tactical strategy is trend following. Trend followers aim to be invested during the good times, when the market is going up, and to sit it out during the bad times, when the market is falling.

Moving averages (MA) are commonly known trend following indicators, where the MA is an average of prices over a predetermined time horizon, whether that’s 200-days or 50-days.

Moving average strategies can help investors gauge whether the market is trending upwards or downwards, and simple moving average strategies can help to protect investors from sustaining major losses during a long bear market.

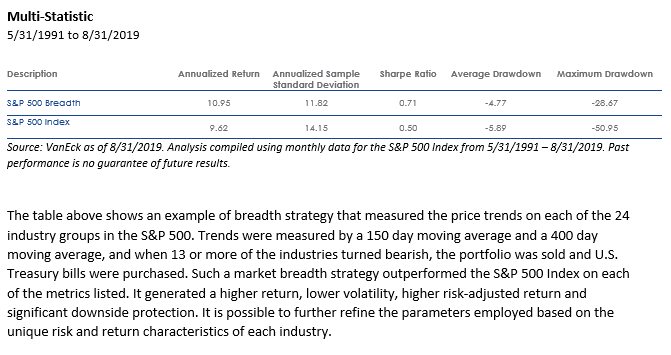

Market breadth is another form of trend following that we explored in a recent whitepaper. It provides investors with additional information, by measuring the price trends of the underlying index components of the broad market in an attempt to more accurately differentiate between small and large market corrections.

A market breadth strategy may provide investors with a more robust signal, because the strategy signals are incorporating more granular data (i.e., sector price trends) when compared with single top-line index returns.

The table above shows an example of breadth strategy that measured the price trends on each of the 24 industry groups in the S&P 500. Trends were measured by a 150 day moving average and a 400 day moving average, and when 13 or more of the industries turned bearish, the portfolio was sold and U.S. Treasury bills were purchased.

Such a market breadth strategy outperformed the S&P 500 Index on each of the metrics listed. It generated a higher return, lower volatility, higher risk-adjusted return and significant downside protection. It is possible to further refine the parameters employed based on the unique risk and return characteristics of each industry.

All of the up, none of the down... doesn't exist

Unfortunately, there is no magic bullet that will solve late-cycle investment questions for investors. Predicting the future is impossible. A bear market is inevitable, and trying to time the market using human intuition is a fruitless project.

Instead of trying to call the top, or catch a falling knife, we believe that investors should thoughtfully consider a range of options to account for numerous outcomes. Those options could include incorporating more robust forward-looking valuation metrics that helps to protect against overvalued companies.

Another option would be to incorporate a tactical strategy which could potentially protect investors during a sustained bear market scenario. Rather than trying to predicting a bear market, we believe investors should instead position themselves to be prepared for one.

VanEck's whitepaper is ready for reading now. Ed Lopez will also be speaking at Inside ETFs in Florida later this month. Join us to hear his expert views on building a defensive portfolio.

Please note that Van Eck Securities Corporation (an affiliated broker-dealer of Van Eck Associates Corporation) offers investment products that invest in the asset classes discussed herein.

The Morningstar® Wide Moat Focus IndexSM consists of U.S. companies identified as having sustainable, competitive advantages and whose stocks are attractively priced, according to Morningstar.

The S&P 500® Index consists of 500 widely held common stocks covering the leading industries of the U.S. economy.

Effective June 20, 2016, Morningstar implemented several changes to the Morningstar Wide Moat Focus Index construction rules. Among other changes, the index increased its constituent count from 20 stocks to at least 40 stocks and modified its rebalance and reconstitution methodology. These changes may result in more diversified exposure, lower turnover, and longer holding periods for index constituents than under the rules in effect prior to this date. Past performance is no guarantee of future results

The Morningstar® Wide Moat Focus IndexSM was created and is maintained by Morningstar, Inc. Morningstar, Inc. does not sponsor, endorse, issue, sell or promote the VanEck Vectors Morningstar Wide Moat ETF and bears no liability with respect to that ETF or any security. Morningstar® is a registered trademark of Morningstar, Inc. Morningstar® Wide Moat Focus IndexSM is a service mark of Morningstar, Inc

The S&P 500® Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Van Eck Associates Corporation. Copyright ©2019 S&P Dow Jones Indices LLC, a division of S&P Global, Inc., and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of S&P Global and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. Neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors shall have any liability for any errors, omissions, or interruptions of any index or the data included therein.

This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.