High yield bonds closed higher in the Index today (May 08) by + 0.030% and higher for the week by + 0.051%.

Spreads have stabilized and were slightly wider on the week. Managed funds continue a positive inflow for the fifth week in a row. The largest HY ETF's also showed a solid inflow for this past measured week.

Nineteen new issues in nineteen USD tranches were priced this week totaling $12.58bn in volume. Month-to-date volume is $12.58bn.

HY Spreads are mainly wider over the last five trading sessions. The Average was widened by four basis points, CCCs widened by sixteen basis points to +920. Bs are wider by two at +307, and BBs widened by four basis point at +173. Within the ICE/ BofA US HY Index, the Average return for April was + 0.051%%, Bs outperformed, higher by + 1.210%. BBs returned +0.064% and CCCs returned - 0.299%

Primary market activity is diverse and welcoming to new production bonds.

The primary market is actively financing clean or good story issuers. Issuers this week include glass packaging, logistics, airplanes / airline, a retailer, energy, financials, storage services, telecommunications, casino / hospitality, manufacturing, and technology.

The featured deal of the week was $600m (from $1.175bn) [Pioneer OpCo LLC] (VENRES) 144a for life / Reg S 7nc2 (from 7nc3) senior secured note. B2 / B. via Bookrunners: JPM+. along with $1.175bn TLB, to refinance existing capital structure. Priced at 7.00%, +279 vs UST 4.125% 04/30/2033. The bond side was downsized in favor of upsizing the TLB, which received favorable terms, ultimately pricing at +325, 50bps through discissions. The Venetian Resort was purchased by Apollo Global Management in 2022. Apollo isusing these transactions to refinance the capital structure. Bonds traded up +1.25pts in secondary trading

Treasury yields closed the week modestly lowers, in general. The 2-year was higher by +0.8bps to 3.885%. 5-year was lower by -1.2bps to 4.002%. 10-year lower by -1.6bps to 4.354%, and the 30-year was lower by -2.4bps to 4.934%. The 2s-10s curve narrowed - 2.5bps to 47.5bps. Strong economic data and sticky inflation continue to divide sentiment. FOMC members signaled a shift to neutral to hawkish stance from a prior easing bias.

Stocks were higher at today (05/08) and higher for the week.

The Dow was higher for the week by + 0.22%, S&P 500 + 2.22%, NASDAQ + 4.51%, and the Russell 2000 finished the week + 1.72%. Markets continue to focus on positive price trends as investors are still willing to look past the war in Iran. The VIX closed today at 17.19, higher by + 0.20 for the week.

In this week's economic data releases, Factory Orders beat expectations, Durable Goods were higher and in-line, Capital Goods Orders & Shipped were higher and in-line, Imports faded while, Exports were a slight beat, Services and Composite PMI were below expectations, ISM Services complex was softer than expected, JOLTS data was higher but with higher layoffs, New Home Sales jumped, ADP Employment was lower than forecasts, Productivity was higher and Labor Costs lower, Initial and Continuing Jobless Claims were low, Nonfarm Payroll s were higher but Hourly Earnings missed. UMich Sentiment and Current Conditions slipped, and the Inflation expectations component was lower.

Weekend event risk of fears are uncertain. Iran continues to chastise US demands, while President Trump continues to threaten. Military readiness in region is building, but the blockade goes on. Oil markets seem encouraged, with prices were little moved on Friday (WTI Jun26 +$0.61 at $95.42 per barrel. and Brent just over $100).

NEW ISSUES THIS WEEK (05/04- 05/08) :

This week, (May 04- May 18, there were nineteen (19) USD high yield deals priced in nineteen tranches. Volume for the week was $12.58bn. Month-to date volume is $12.58bn. 2026 year-to-date volume is $126.95bn vs $79.45bn in 2025. 2026 volume is ahead of last year (2025) by + 59.8%.

Avg | +$0.348 | |||

Issue | Price | Bid | Ask | Δ |

| YAHOOO 11 05/15/31 | 100.000 | 101.750 | 102.000 |

+$1.750 |

APG 5 3/4 06/01/34 | 100.000 | 100.000 | 100.625 | +$0.000 |

BSCOAT 7 1/8 06/15/33 | 100.000 | 100.250 | 100.750 | +$0.250 |

ALK 6 1/2 06/01/31 | 100.000 | 99.500 | 99.875 | -$0.500 |

FRSEAG 7 1/4 08/15/32 | 100.000 | 100.750 | 101.250 | +$0.750 |

HARMID 6 3/4 05/15/34 | 100.000 | 101.000 | 101.250 | +$1.000 |

HLT 5 1/2 09/15/31 | 100.000 | 100.250 | 100.500 | +$0.250 |

VENRES 7 05/15/33 | 100.000 | 101.250 | 101.750 | +$1.250 |

STDCTY 6 1/8 05/15/31 | 100.000 | 100.000 | 100.250 | +$0.000 |

KRAOIG 7 1/8 05/15/31 | 100.000 | 99.875 | 100.125 | -$0.125 |

LVLT 7 1/2 02/15/37 | 100.000 | 101.250 | 101.500 | +$1.250 |

PODLLC 8 3/4 05/15/31 | 100.000 | 100.000 | 100.125 | +$0.000 |

SLM 6.495 05/15/32 | 100.000 | 99.750 | 100.000 | -$0.250 |

BXMT 6 1/4 06/01/31 | 100.000 | 99.500 | 99.750 | -$0.500 |

SEI 6 3/8 05/15/31 | 100.000 | 100.875 | 101.125 | +$0.875 |

ACALTD 5 7/8 05/15/31 | 100.000 | 100.000 | 100.750 | +$0.000 |

BBDBCN 5 7/8 01/15/35 | 100.000 | 100.375 | 100.875 | +$0.375 |

DKL 6 7/8 06/01/34 | 100.000 | 100.250 | 100.750 | +$0.250 |

OI 9 1/2 06/01/33 | 100.000 | 103.000 | 103.500 | +$3.000 |

TODAY'S MARKETS:

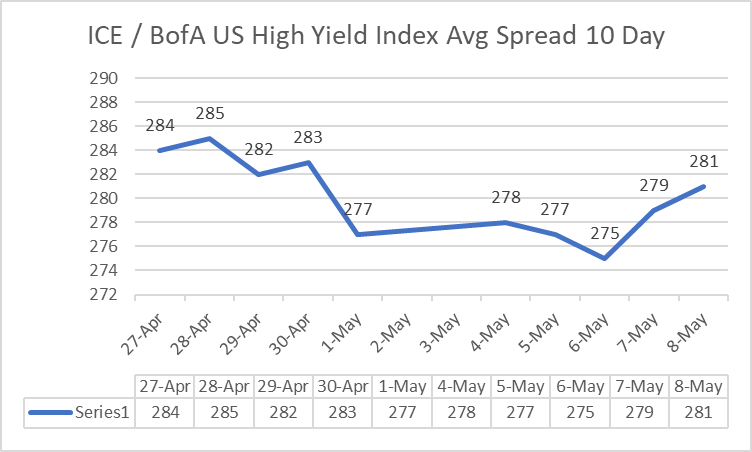

- High-Yield ICE / BofA index is HIGHER today (5/08) by +0.030%. The average spread was widened on 05/08 (+ 02) basis points at 281. The BB sector spread widened by two (+ 02) at 173, The B sector widened (+ 02) at 307. The CCC sector was wider by five (+ 05) at 920.

- Over the prior past five trading days, the Average spread is wider by four, (+ 04), BB's are wider (+ 04), B's are wider by two (+ 02)bps, and CCCs are wider (+ 16)bps.

- The largest HY ETFs are HIGHER today (05/08) by +0.31% on average and are HIGHER by + 0.10% over the past five trading days, on average.

- The CDX HY Index is HIGHER today, May 08 by + 0.114 at 107.385. The best performers are CSC Holdings LLC (CSCHLD), Domtar Corp. (UFS), and Unisys Corp. (UIS). The worst performers are Goodyear Tir & Rubber Co. (GT), Asurion LLC (ASUCOR), and Nabors Industries Inc. (NBR),

- Oil (WTI Jun26) is HIGHER today by +$0.61 at $95.42 per barrel.

- The Dollar Index (DXY) is LOWER today by - 0.228% at 97.843.

- Spot Gold is HIGHER today by + $30 at $4715 per ounce.

ICE / BofA US HY Index 10-day Average Spread

* HY ETF Fund Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| May 06 | 1.096bn | 280m |

| Apr 29 | 816m | 49m |

| Apr 22 | 767m | -2.673bn |

| Apr 15 | 3.44bn | 2.55bn |

* HY Managed Funds Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| May 06 | 643.2m | -847m |

| Apr 29 | 1.49bn | 903m |

| Apr 22 | 587m | -2.293bn |

| Apr 15 | 2.80bn | 1.992bn |

Access IGM’s podcasts and webinar series that features a dynamic mix of insights from IGM analysts and influential market practitioners.

Podcasts: "Credit Matters" (co-hosted with Bruce Clark, Head of U.S. Rates Market Coverage at IGM)

👉 Explore the latest episodes covering key trends and developments in the credit market

Webinars: "Market Insiders"

👉 Explore our full webinar library and discover what you've been missing