Only two issuers accessed the high-grade primary market today, though volume told a different story as the pair raised a combined $27.6bln across 11 tranches.

The outsized day helped set the tone for a week in which syndicate desks are calling for $41bln in new issuance.

Oracle led the day with a jumbo $25bln eight-part offering, following its announcement over the weekend that it plans to raise up to $50bln across debt and equity markets in 2026 as it accelerates investment in cloud infrastructure to support demand from the AI computing industry. The transaction spanned maturities from three to 40 years and generated record peak orderbooks of $129.45bln, equating to 4.3x oversubscription once books ultimately settled at $108.64bln. “It shows there is a lot of liquidity out there looking for a home and that solid market technicals continue to outweigh everything else,” said one senior syndicate banker.

The transaction priced through secondary levels, carrying a negative 0.86bp new issue concession. It marked the firm’s second jumbo visit to the primary market in the past five months following a $15bln ten-part deal at the end of September.

GE Vernova completed the day’s issuance with a $2.6bln three-part debut offering tied to its acquisition of the remaining 50% stake in Prolec GE for $5.3bln, announced last October.

The transaction became the fifth M&A-linked deal of the year, lifting total M&A-related issuance to $12.45bln, well ahead of the $4.8bln seen across three deals at the same point last year. The offering saw even stronger demand than the Oracle deal, with orderbooks settling at 8.2x oversubscribed.

Away from credit, robust corporate earnings and stellar economic data helped stocks overcome a wobbly start Monday. With about one-third of the S&P 500 reporting, year-on-year earnings growth jumped ahead of estimates to 11.9%, on track for a fifth consecutive quarter of double-digit returns.

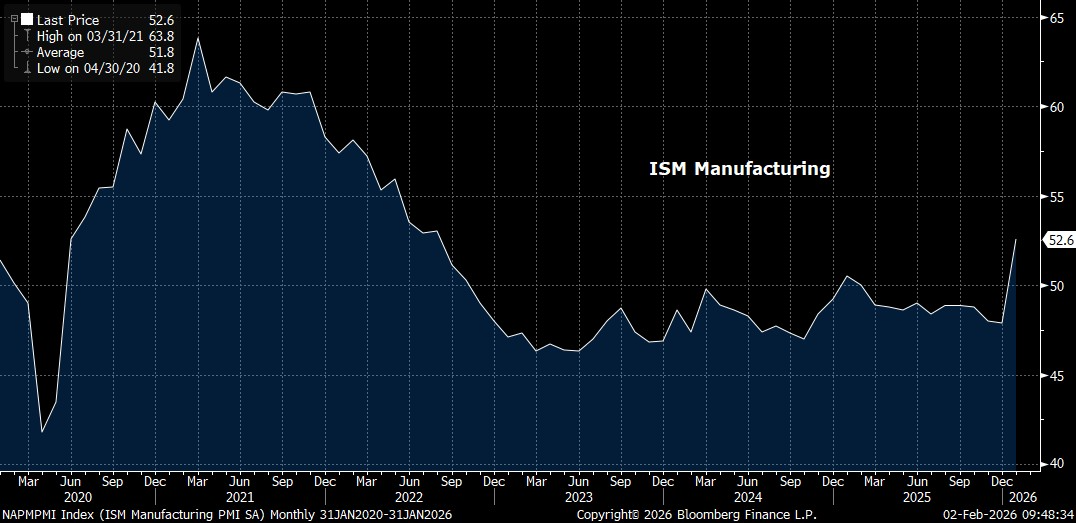

However, the bright spot in the session came from a huge and unexpected rebound in the January ISM manufacturing survey, expanding by the most since 2022 behind a surge in demand. Most analysts appear to have forgotten that a key provision of the budget (Big Beautiful Bill) signed last summer was full and immediate write-off of capex for buildings, equipment, machinery, software, etc., rather than over time, beginning on Jan 1.

In Washington, the partial government shutdown that nobody noticed entered its third day as parties remain deadlocked over funding for departments not covered by the November 2025 resolution. Politicians from both sides suggested that there’s no appetite for a prolonged standoff, but they always say that. Nevertheless, the BLS just said the January jobs report will NOT be released on Friday as scheduled.

Meanwhile, Kevin Warsh has yet to offer public remarks since being tapped by President Trump for Fed chair. Even so, Warsh’s reputation as a policy hawk destroyed the narrative that Trump was stacking the Fed with easy policy ideologues, giving a boost to the US dollar and laying waste to popular hedges in gold, silver, and crypto.

Looking ahead to tomorrow, issuance is expected to broaden as Oracle’s jumbo transaction sidelined several borrowers today who are expected to revisit the market in the morning. PacifiCorp is also considered a potential issuer after completing investor calls.

ORACLE CORP

$25bln Oracle Corp (ORCL) SEC registered 8-pt (3yr FXD/FRN (2/4/29), 5yr (2/4/31), L7yr (5/4/33), 10yr (2/4/36), 20yr (2/4/46), 30yr (2/4/56), 40yr (2/4/66) senior unsecured notes. Baa2/BBB/BBB (n/n/s). BofA(30yr & 40yr)/CITI/HSBC/GS(B&D 3yr, 5yr, long 7yr, 10yr, 20yr)/JPM. UOP: General Corporate Purposes, which may include capital expenditures, repayment of indebtedness, future investments or acquisitions and payment of cash dividends on or repurchases of common stock. Denoms 2k x 1k. MWC. Par call 1 month (3yr FXD, 5yr), 2 months (long 7yr), 3 months (10yr), 6 months (20yr, 30yr, 40yr) prior to maturity. Sales to Canada: yes. CUSIP: 68389X DV4 / 68389X DW2 / 68389X DX0 / 68389X DY8 / 68389X DZ5 / 68389X EA9 / 68389X EB7 / 68389X EC5. ISIN: US68389XDV47 / US68389XDW20 / US68389XDX03 / US68389XDY85 / US68389XDZ50 / US68389XEA90 / US68389XEB73 / US68389XEC56. S/D: 2/4. (I)

IPT(s): +125 area, SOFR Equivalent, +145 area, +160 area, +175 area, +200 area, +210 area, +225 area.

GUIDANCE: +95#, SOFR Equivalent, +115#, +130#, +145#, +170#, +180#, +195#.

LAUNCHED: $3bln 2/4/29 +95, $500m 2/4/29 SOFR+111, $3.5bln 2/4/31 +115, $3bln 5/4/33 +130, $5bln 2/4/36 +145, $2.25bln 2/4/46 +170, $5bln 2/4/56 +180, $2.75bln 2/4/66 +195.

PRICED:

$3bln 4.55% 2/4/29 99.872 4.596% +95 MW T+15 (TSY 3.50% 1/15/29)

$500m 2/4/29 SOFR+111

$3.5bln 4.95% 2/4/31 99.834 4.988% +115 MW T+20 (TSY 3.75% 1/31/31)

$3bln 5.35% 5/4/33 99.951 5.354% +130 MW T+20 (TSY 4.00% 1/31/33)

$5bln 5.70% 2/4/36 99.782 5.729% +145 MW T+25 (TSY 4.00% 11/15/35)

$2.25bln 6.55% 2/4/46 99.912 6.558% +170 MW T+30 (TSY 4.625% 11/15/45)

$5bln 6.70% 2/4/56 99.82 6.714% +180 MW T+30 (TSY 4.75% 8/15/55)

$2.75bln 6.85% 2/4/66 99.81 6.864% +195 MW T+30 (TSY 4.75% 8/15/55)

BOOKS: final books: 3yr FRN $2.1bln, 3yr FXD $12.05bln, 5yr $14.27bln, 7yr $13.65bln, 10yr $23.0bln, 20yr $10.3bln, 30yr $20.5bln, 40yr $12.77bln. Peak books: 3yr FRN: $2.8bln, 3yr FXD: $12.2bln, 5yr: $15.75bln, 7yr: $16.6bln, 10yr: $25.4bln, 20yr: $15.1bln, 30yr: $24.2bln,

40yr: $17.4bln.

COMPS:

ORCL 4.8% Aug 2028 at T+99, G+91

ORCL 6.15% Nov 2029 at T+110, G+104

ORCL 4.45% Sep 2030 at T+100, G+103 $98

ORCL 2.875% Mar 2031 at T+117, G+115 $91

ORCL 4.8% Sep 2032 at T+135, G+117

ORCL 5.2% Sep 2035 at T+140, G+141

ORCL 5.875% Sep 2045 at T+172 $91

ORCL 5.95% Sep 2055 at T+178

ORCL 6.1% Sep 2065 at T+192

NIC:

3yr: Flat FV: 95 (add a few points for curve to 28s)

5yr: Flat FV: 115 (add and then cut a few points from Mar 31s)

7yr: Neg 1bp FV: 131 (10-15bp away from Sep 32s)

10yr: Flat FV: 145 (add a few points for curve to to 35s)

20yr: Neg 3bp FV 173 (add a few points for curve low dlr price to 45s)

30yr: Neg 2bp FV: 182 (add few points for curve to 55s)

40yr: Flat FV: 195 (add few points for curve, low dollar price to 65s)

GE VERNOVA

$2.6bln GE Vernova (GEV) 3-pt (5yr (2/4/31), 10yr (2/4/36) & 30yr(2/4/56)) SEC Registered senior unsecured notes.NR/BBB/BBB+ (P/P). CITI(B&D 5yr)/JPM(B&D 10yr)/MS(B&D 30yr). UOP: General corporate purposes, including financing a portion of the acquisition of the remaining 50% percent stake of Prolec GE that is expected to close on February 2, 2026. MWC. Par call 1mo (5yr), 3mo (10yr), 6mo (30yr). prior to mat. CoC @ 101%. Marketing: www.dealroadshow.com Passcode: PILLAR2026. Offering Memorandum: The Preliminary Offering Memorandum will be made available via NetRoadshow. Upon completion of this transaction, please log in to NetRoadshow for the distribution of any unregistered Final Offering Memorandums. CUSIPs: 5y: 36828A AA9 10yr: 36828A AB7 30yr: 36828A AC5. ISINs: 5yr: US36828AAA97 10yr: US36828AAB70 30yr: US36828AAC53. Sales to Canada: YES. Denoms 2k x 1k. S/D 2/4 (I) (M&A) (DEBUT)

IPT(s): +75 area, +95 area, +110 area.

GUIDANCE: +45#, +65#, +78#.

LAUNCHED: $600m 2/4/31 +45, $1bln 2/4/36 +65, $1bln 2/4/56 +78.

PRICED:

$600m 4.25% 2/4/31 99.835 4.287% +45 MW T+10 (TSY 3.75% 1/31/31).

$1bln 4.875% 2/4/36 99.578 4.929% +65 MW T+10 (TSY 4.00% 11/15/35).

$1bln 5.50% 2/4/56 97.239 5.693% +78 MW T+15 (TSY 4.75% 8/15/55).

BOOKS: final books: $4.75bln, $7.05bln, $9.55bln.

COMPS: n.a.

NIC: n.a.