High yield bonds closed higher in the Index this week thanks to a strong rally today (Friday) as investors came out to buy the dip in equities and buoying junk bonds.

The Index was higher on Monday by + 0.108%, then down all three days midweek before bouncing back today, (Friday) higher by + 0.168%. The Index was higher for the week by + 0.118%, with Monday and Friday serving as "bookends".

Stocks and rates rebounded today as markets bounced hard after an earlier capitulation in Asia as crypto and metals recovered Thursday looks like forced stop-loss selling of leveraged plays rather than meaningful downturn in economic outlook. Pro-cyclical shares in banking and energy jumped to record highs, as corporate earnings are running at double-digit growth for fifth consecutive quarter, and credit markets remain strong at record tight spreads.

The sentiment was soured this week, first after turning their backs on AI and software stocks causing a combined loss of over a trillion dollars in valuations before stepping back in to buy on Friday. Secondly, stocks took another leg down on Thursday after labor data showed some glaring weaknesses. A trio of weak employment reports yesterday rattled investors. Soft labor stats from JOLTS, Challenger, and Weekly Claims cast doubt on otherwise strong start to year.

Weekend event risk of fears of the past several weeks are not surfacing.

The possibly of an attack on Iran this weekend seems unlikely, and the government shutdown has been avoided. Tensions were elevated earlier in the week after Iran had a drone shot down by the US Navy. Iran reported today that talks have resumed and that there appears to be progress made.

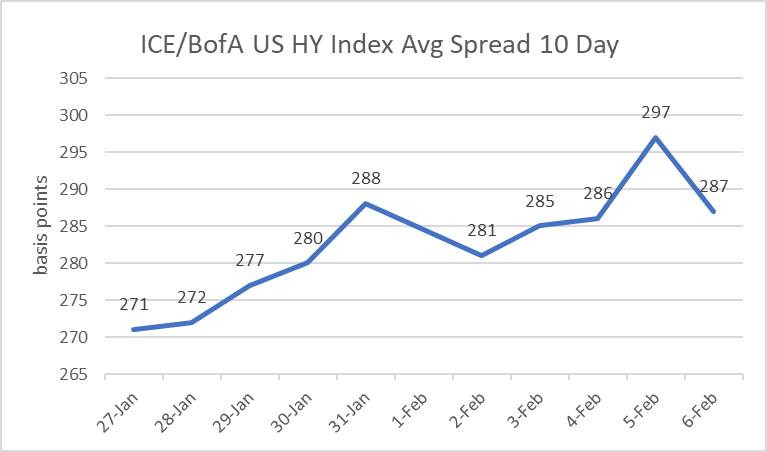

Today's stock rally advanced the high yield bond Index to close higher by + 0.176%. Spreads narrowed by ten basis points in the Average to 287, while CCCs narrowed by eight basis points to 892. The high yield market has been down seven out the past ten trading days. Bs and CCCs (especially) are getting hit the hardest. The HY market is still viewing the US economy with a telescope. That forward looking view has become much more aware of near-term volatility and potential headwinds. The primary market absorbed five new issues this week with one deal of the forward calendar.

HY Spreads were mainly soft this week and widened by seven basis points to +287 in the Average. CCCs widened by thirty-seven basis point to +892. Bs were wider by six to +312, and BBs were unchanged at +171 Within the ICE/ BofA US HY Index, the Average return is higher for the week by - 0.118%. For the week, BBs outperformed. The CCC rated sector was lower for the week by - 0.119% after tumbling on Thursday. Bs were higher by +0.073%. BBs closed higher by + 0.181%...

One of the better new issues this week was $2.0bn [Black Pearl Compute LLC] (BLKPRL) 144a for life / Reg S 5nc2 senior secured note. Ba2 / __ / BB-. via Left Lead & Sole Structuring Agent: MS. Bookrunners: GS / JPM / SANT / SMBC / WFS. UoP: Proceeds will be used to fund the construction of 216 IT MW data center at Black Pearl, to fund debt service reserves, reimburse Parent for prior capital expenditures, and to pay related fees and expenses. Priced at 6.125%, at par, +232 vs UST 5.375% 02/15/2031. s/d 02/11 (t+5). Bonds closed the week at $101.00 bid

Treasury yields were higher today by one to four basis points as the haven bid subsided as stocks, metals, and crypto snap back. Thursday’s action appears to be classic stop-loss capitulation of crowded leveraged trades, triggering flight to quality into Treasuries. The 2s-10s curve flattened on Friday as calm returned and economic data remains strong overall, In today's data, the UMich sentiment jumped to a six-month high while year-ahead inflation expectations fall to 13-month low at 3.5%. The Truflation CPI gauge ended the week below 1%

NEW ISSUES THIS WEEK (02/02 - 02/06) :

This week, (Feb 02- Feb 06), there were five (05) USD high yield deals in six(06) tranches priced. Volume for the week was $5.20bn. 2026 year-to-date volume is $33.37bn vs $23.22bn in 2025. 2026 volume is ahead of last year (2025) by + 21%.

Avg | +$0.345 | |||

Issue | Price | Bid | Ask | Δ |

AZORRA 6 1/4 02/15/34 | 100.000 | 99.625 | 100.000 | -$0.375 |

BLKPRL 6 1/8 02/15/31 | 100.000 | 101.000 | 101.250 | +$1.000 |

HHH 5 7/8 03/01/32 | 100.000 | 99.625 | 100.000 | -$0.375 |

HHH 6 1/8 03/01/34 | 100.000 | 99.625 | 100.000 | -$0.375 |

AVIAGP 9 1/2 01/28/31 | 101.951 | 102.000 | 102.250 | +$0.041 |

THS 7 3/4 02/11/33 | 100.000 | 102.000 | 102.375 | +$2.000 |

UAL 4 7/8 03/01/29 | 100.000 | 100.250 | 100.500 | +$0.250 |

TODAY'S MARKETS:

- High-Yield ICE/BofA index is higher today (2/06) by +0.168%. The average spread narrowed on 02/06 (- 10) basis points at 287. The BB sector spread narrowed (- 09) at 171 The B sector narrowed (- 11) at 312. The CCC sector was narrower (- 08) at 898.

- Over the prior past five trading days, the Average is wider by + 07bps, BB's are unchanged by + 0bps, B's are wider by + 06bps, and CCCs are wider by +37bps.

- The largest HY ETFs are HIGHER today (2/06) by + 0.34% on average and are LOWER by - 0.42% over the past five trading days, on average.

- The CDX HY Index is HIGHER today, Feb 06, by + 0.441 at 108.148. The best performers are CSC Holdings LLC (CSCHLD), The Hertz Corp. (HTZ), and Staples Inc. (SPLS). The worst performers are New Albertson's Inc. (NEWALB), Calpine Corp. (CPN), and iHeartCommunications Inc (IHRT)

- Oil (WTI Mar26) is HIGHER today by + $0.26 at $63.55 per barrel.

- The Dollar Index (DXY) is LOWER today by - 0.151% at 97.681

- Spot Gold is HIGHER today by + $185 at $4964 per ounce.

ICE / BofA US HY Index 10-day Average Spread

* HY ETF Fund Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Feb 04 | -28k | -616k |

| Jan 28 | 588m | 735m |

| Jan 21 | -147m | -1.097bn |

| Jan 14 | 950m | 269m |

* HY Managed Funds Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Feb 04 | 421m | 188m |

| Jan 28 | 233m | 1.653bn |

| Jan 21 | - 1.42bn | -1/049bn |

| Jan 14 | -371.3m | -649m |

Bond Issuance Summary Table

Company | Size | Structure | Rating | IPT/Price Talk | Bookrunners | Use of Proceeds | Timing |

| Feb 09 week | |||||||

| Block Communications Inc. (BLOCKKC) | $450m | 144a for life / Reg S 5nc2 senior secured note | B3 / B | BofA / JPM / PNC | together with a new four-year Super-Priority Revolving Credit Facility, to finance the existing revolver, TLB, and senior notes | Roadshow through next (02/09) week. |