High yield bonds closed higher in the Index today (Apr 24) by + 0.058% but lower for the week by - 0.195%. Spreads stabilized and were slightly wider on the week.

Managed funds had a positive but smaller inflow for the third week in a row. The largest HY ETF's also showed a smaller inflow for this past measured week. War negotiations over the Strait of Hormuz are tenuous Israel with the possibility further US / Iran negotiations in Pakistan on Friday night. Negotiations on the Iran nuclear program could be long and drawn out, but the markets hold optimism for steps toward a lasting resolution.

Six new issues in seven USD tranches were priced this week totaling $7.125bn in volume.

HY Spreads were modestly wider over the last five trading sessions. The Average was widened by three basis points, CCCs widened by six basis points to +918. Bs were wider by six at +309, and BBs widened by one basis point at +175. Within the ICE/ BofA US HY Index, the Average return month-to-date is + 1.820%%. Month-to-date, CCCs outperformed, higher at + 2.799%. For this past week, the BB rated sector was lower by - 0.162%, Bs are lower by - 0.257%, and CCCs are lower by - 0.192%

The featured deal of the week was $3.30bn [Core Scientific Finance I LLC] (COREZ) 144a for life / Reg S 5nc2 senior secured note. __ / BB / tbd (S&P / Fitch). Proceeds will be used to fund the Debt Service Reserve Account, and the remaining proceeds to pay a distribution to Parent. Denoms: 2k x 1k. Investor call at 10:30AM EST today, April 21, for expected pricing mid-week. Biz: Core Scientific Finance I LLC is developing six data center facilities across five sites that have been 100% contracted with CoreWeave. The Projects are expected to support an aggregate of ~590 MW of critical IT capacity, with 185MW already online, and represent ~$10Bn in potential revenue over the 12-year base contract term. The bonds were priced at 7.75% coupon, $99.25. 7.933%, +399 vs UST 1.625% 05/15/2031. The deal was priced the day after the $1.30bn 5nc2 EDGCOM issue, which opened flat once free-to trade (post syndicate). COREX was priced with incremental spread after EDGCOM deal traded heavily in 2ndry trading, The COREX deal has more size and priced with 41bps of additional spread.

The sentiment in the primary market is positive and welcoming to new production bonds. The primary market is open for business and mainly financing clean well-established or good story issuers.

Treasury yields closed the week higher. The 2-year was higher by +7.0bps to 3.778%. 5-year was higher by +6.8bps to 3.915%. 10-year higher by +5.6bps to 4.301%, and the 30-year was higher by -+2.3bps to 4.907%. The 2s-10s curve narrowed - 2.0bps to 52bps

Stocks were higher at today (04/17) and mixed for the week. The Dow was lower for the week by - 0.16%, S&P 500 + 0.55%, NASDAQ + 1.50%, and the Russell 2000 finished the week + 0.36%. Month-to-date (April), the Dow is higher by + 6.23%, S&P 500 + 9.75%, NASDAQ + 15.03%, and the Russell 2000 is higher by + 11.64%. The VIX was higher for the week by +1.23 points to 18.71. The Philadelphia Semiconductor Index gained for unprecedented 18h straight day.

In this week's economic data releases, Retail Sales surprised to the upside, Pending Home Sales were higher, Initial & Continuing Jobless Claims were in-line, the S&P US PMI complex all exceeded forecasts, and the UMich Sentiment / Current Conditions / Expectations complex reported higher numbers with the Inflation data little changed.

Weekend event risk of fears have improved from earlier in the week with Iran and Lebanon still in a limited ceasefire.

New negotiations could take place on Friday night (hopefully). Iran will likely slow talk its nuclear plans The Strait of Hormuz remains closed to all commercial vessels. The US Navy blockade remains in place to monitor military activity and plans to remain in the region until a satisfactory end is in met. Oil (WTI Jun26) was lower today by -$1.45 to $94.40 per barrel.

NEW ISSUES THIS WEEK (04/20- 04/24) :

This week, (Apr 20- Apr 24, there were six (06) USD high yield deals priced in seven tranches. Volume for the week was $7.125bn. Month-to date volume is $28.90bn. 2026 year-to-date volume is $106.75bn vs $72.85bn in 2025. 2026 volume is ahead of last year (2025) by + 46.5%

Avg | -$0.220 | |||

Issue | Price | Bid | Ask | Δ |

AITWOR 8 3/4 04/30/34 | 100.000 | 100.500 | 101.500 | +$0.500 |

VSTJET 8 3/4 01/15/32 | 99.473 | 98.500 | 99.000 | -$0.973 |

CORZ 7 3/4 05/15/31 | 99.250 | 99.625 | 99.875 | +$0.375 |

EDGCOM 7 1/2 04/30/31 | 100.000 | 98.875 | 99.250 | -$1.125 |

ENQLN 9 7/8 04/30/31 | 99.038 | 101.250 | 101.750 | +$2.212 |

MINAU 6 05/01/32 | 100.000 | 99.125 | 99.375 | -$0.875 |

MINAU 6 1/4 05/01/34 | 100.000 | 98.875 | 99.376 | -$1.125 |

TIHLLC 7 1/8 06/01/31 | 100.375 | 100.250 | 100.750 | -$0.125 |

TODAY'S MARKETS:

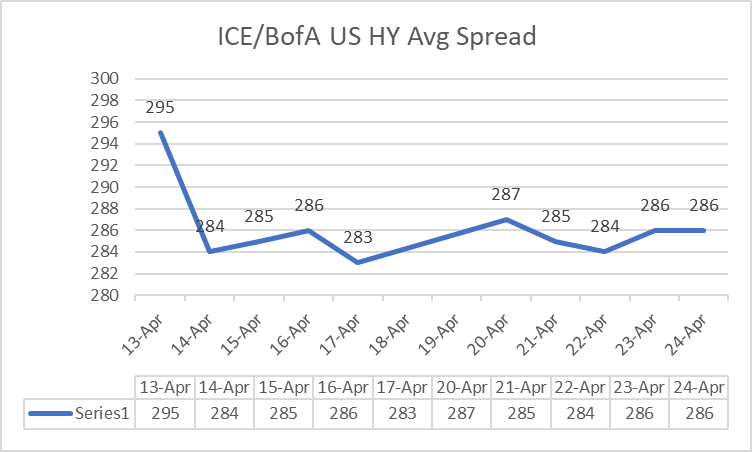

- High-Yield ICE / BofA index is HIGHER today (4/24) by +0.058%. The average spread was unchanged on 04/24 (+ 00) basis points at 286. The BB sector spread widened by one (+ 01) at 175, The B sector was unchanged (+ 00) at 309. The CCC sector was wider (+ 03) at 918.

- Over the prior past five trading days, the Average spread is wider by three basis points, (+ 03), BB's are wider + 01, B's are wider + 06ps, and CCCs are wider by + 06bps.

- The largest HY ETFs are HIGHER today (04/24) by + 0.13% on average and are LOWER by - 0.18% over the past five trading days, on average.

- The CDX HY Index is HIGHER today, Apr 24 by 0.021 at 107.093. The best performers are Organon & Co (OGN), Xerox Corp. (XRX), and iHeartCommunications Inc. (IHRT). The worst performers are Tenet Healthcare Corp. (THC), Gray Media Inc. (GTN)., and Kohl's Corp. (KSS)

- Oil (WTI Jun26) is LOWER today by -$1.45 at $94.40 per barrel.

- The Dollar Index (DXY) is LOWER today by - 0.251% at 98.510.

- Spot Gold is HIGHER today by +$15 at $4710 per ounce.

ICE / BofA US HY Index 10-day Average Spread

* HY ETF Fund Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Apr 22 | 767m | -2.673bn |

| Apr 15 | 3.44bn | 2.55bn |

| Apr 08 | 940m | 3.793bn |

| Apr 01 | -2.853bn | -2.253bn |

* HY Managed Funds Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Apr 22 | 587m | -2.293bn |

| Apr 15 | 2.80bn | 1.992bn |

| Apr 08 | 807.5m | 3.368bn |

| Apr 01 | -2.56bn | -0.59bn |

Access IGM’s podcasts and webinar series that features a dynamic mix of insights from IGM analysts and influential market practitioners.

Podcasts: "Credit Matters" (co-hosted with Bruce Clark, Head of U.S. Rates Market Coverage at IGM)

👉 Explore the latest episodes covering key trends and developments in the credit market

Webinars: "Market Insiders"

👉 Explore our full webinar library and discover what you've been missing