High yield bonds closed lower today by - 0.318% and were lower in the Index this week.

The Index was lower for the week by - 0.734% in the Average. Seven solid deals were priced this in seven tranches creating $4.66bn volume for the week.

No new issues were priced on Friday. Seven single tranche deals were announced and pried this week. AMC Entertainment remains as the only announced deal on the forward calendar, still looking to price a $750m TLB and $1.73bn 5nc2 first lien senior secured notes (B3/B). Risk tolerances have continued to diminish, and underwriters have not yest secured the orders due to market volatility.

HY Spreads were wider on Friday, and also for the week.. CCCs widened by nineteen basis point this week to +978. Bs were wider for the week by fifteen at +360, and BBs widened by fifteen basis point at +206. Within the ICE/ BofA US HY Index, the Average return is lower for the week by - 0.734%. For the week, Bs outperformed. The CCC rated sector was lower for the week by - 0.661%, and. Bs were lower by - 0.604%. BBs closed lower by - 0.817%....

The featured deal of the week was $500m Moog Inc. (MOGA) 144a / Reg S for life 8.5nc3 senior unsecured note. Ba2 / BB. via Bookrunners: JPM +. Net proceeds from the offering, together with cash on hand, to redeem all $500 million aggregate principal amount outstanding of its 4.250% Senior Notes due 2027 (the “2027 Notes”), including any accrued and unpaid interest thereon. The maker precision motion control systems was priced at 5.50%, +147 vs UST 4.25% 11/15/2034 (narrower than I expected) and was bid up to $100.625% after breaking syndicate.

The sentiment in the secondary market is still welcoming despite geopolitical headwinds. Though not officially announced, deals are expected this coming week from Electronic Arts (EA), Sealed Air (SEE), and Nexstar Media (NXST).

Treasury yields closed the week higher due to inflation fears and fewer (if any) rate cuts this year from the FOMC. The 2-year was higher for the week by +15.6bps to 3.717%, the 5-year higher by 13.1bps to 3.858%, the 10-year +13.9bps to 4.277%, and the 30-year higher by 14.7bps to 4.904%.

Stocks were modestly lower on Friday and lower for the week on fears of supply disruptions and higher prices. The Dow was lower for the week by - 1.99%, S&P 500 - 1.60%, NASDAQ - 1.26%, and the Russell 2000 finished the week - 1.79%.

In this week's economic data releases, NY Fed Inflation Expectations were lower, Small Business Optimism was lower, ADP Weekly Employment exceeded expectations, Existing Home Sales were higher, CPI data was in-line, Average Hourly Earnings were up, Initial & Continuing Jobless Claims were in-line, Housing Starts were up / Building permits were lower, PCE and Core PCE were in-line, Durable Goods Ex-Trans was slightly lower, and Capital Goods Orders / Shipped were down. GDP 4Q and Consumption Second Read were lower. The GDP Price Index was higher, while Core PCE QoQ was in-line. UMich Sentiment and Current Conditions were higher, while Expectations and Inflation components were down. JOLTS Job Openings were higher, the Quits Level was in-line, and the Layoffs Level was lower

Weekend event risk of fears continues as the war with Iran presses on. Negotiations do not feel near as Iran says that it will not cease to enrich uranium, and the US says they will not allow Iran to do such. The US military actions continue to build, and the duration of the military action is likely last for longer than most expect..

NEW ISSUES THIS WEEK (03/08 - 03/13) :

This week, (Mar 08- Mar 13), there were seven (07) USD high yield deals in seven (07) tranches priced. Volume for the week was $4.66bn. Month-to date volume is $9.95bn. 2026 year-to-date volume is $66.81bn vs $51.73bn in 2025. 2026 volume is ahead of last year (2025) by + 29.2%.

Avg | +$0.018 | |||

Issue | Price | Bid | Ask | Δ |

CLMT 9 3/4 02/15/31 | 105.000 | 105.250 | 105.500 | +$0.250 |

ESAB 5 5/8 04/01/31 | 100.000 | 100.250 | 100.500 | +$0.250 |

CRC 7 01/15/34 | 100.000 | 100.000 | 100.250 | +$0.000 |

FAIRIC 6 1/4 09/15/34 | 100.000 | 99.125 | 99.375 | -$0.875 |

KGS 5 7/8 04/01/31 | 100.000 | 100.125 | 100.375 | +$0.125 |

MOGA 5 1/2 10/15/34 | 100.000 | 100.500 | 100.875 | +$0.500 |

PENN 6 3/4 04/01/31 | 100.000 | 99.000 | 99.250 | -$1.000 |

TODAY'S MARKETS:

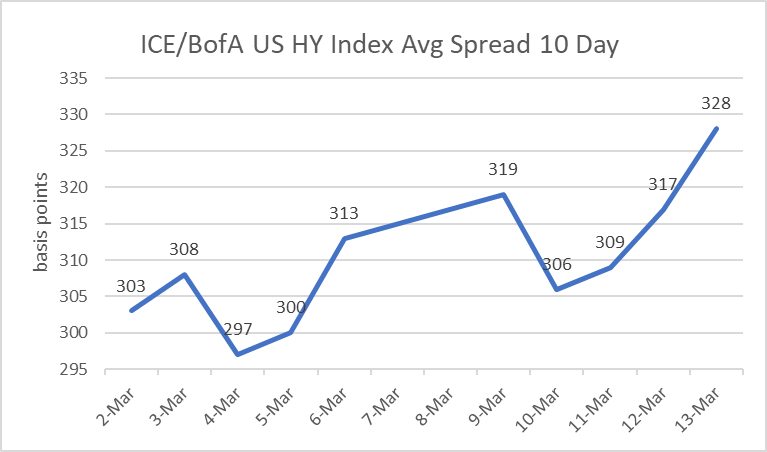

- High-Yield ICE / BofA index is LOWER today (3/13) by 0.319%. The average spread was wider on 03/13 (+ 11) basis points at 328. The BB sector spread widened (+ 09) at 206, The B sector widened (+ 11) at 360. The CCC sector was wider by (+ 17) at 978.

- Over the prior past five trading days, the Average is wider + 15bps, BB's are wider + 15bps, B's are wider + 15bps, and CCCs are wider by + 19bps.

- The largest HY ETFs are LOWER today (3/13) by - 0.21% on average and are LOWER by - 0.66% over the past five trading days, on average.

- The CDX HY Index is LOWER today, Mar 13 by - 0.3251at 104.974. The best performers are Xerox Corp. (XRX), Venture Global LNG Inc. (VENLNG), and CoreWeave Inc. (CRWV). The worst performers are Organon & Co. (OGN), Kohl's Corp (KSS), and MPT Operating Partnership LP. (MPW)

- Oil (WTI Apr26) is HIGHER today by $8.48 at $95.73 per barrel.

- The Dollar Index (DXY) is HIGHER today by 0.761% at 100.500.

- Spot Gold is LOWER today by - $60 at $5019 per ounce.

ICE / BofA US HY Index 10-day Average Spread

* HY ETF Fund Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Mar 11 | -3.33bn | -3.147bn |

| Mar 04 | -182.8m | 916m |

| Feb 25 | -1.099bn | -1.868Bn |

| Feb 18 | 769m | -120m |

* HY Managed Funds Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Mar 11 | -1.53bn | -1.588bn |

| Mar 04 | 58m | 464m |

| Feb 25 | -406m | -254m |

| Feb 18 | -152m | -68m |

Bond Issuance Summary Table

Company | Size | Structure | Rating | IPT/Price Talk | Bookrunners | Use of Proceeds | Timing |

| Mar 16 week | |||||||

| [Muvico, LLC] (AMC) | $1.73bn | 144a /Reg S for life first lien 5nc2 senior secured note. | B3 / B | Bookrunners: DB (Left Lead / WFS TLD Left Lead) / Citi / GS | net proceeds from the Offering, together with the proceeds from the New Term Loan Facility, and cash on hand, will be used to (i) fund the redemption in full of $400 million aggregate principal amount of 12.750% Senior Secured Notes due 2027 (the “Odeon Notes”) issued by Odeon Finco PLC (“Odeon”), a wholly-owned direct subsidiary of Odeon Cinemas Group Limited and an indirect subsidiary of AMC, (ii) refinance the Company’s existing term loan facility in full, and (iii) pay related fees, costs, premiums and expenses in connection with such transactions. | tbd |

To receive this analysis plus much more, subscribe to IGM. Request your free trial of the service today.