IGM Global Credit Snapshot - August 2025

By Gavin KendrickShareshare

IGM's Global Credit Snapshot is best viewed in the original PDF format available here: August 2025

Key take-aways:

Europe

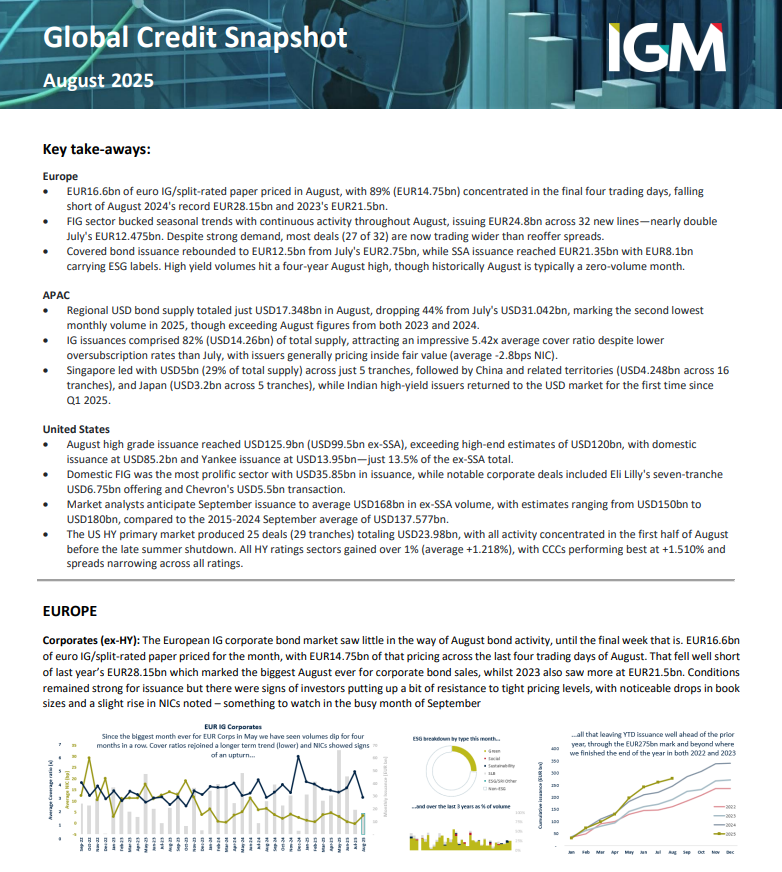

- EUR16.6bn of euro IG/split-rated paper priced in August, with 89% (EUR14.75bn) concentrated in the final four trading days, falling short of August 2024's record EUR28.15bn and 2023's EUR21.5bn.

- FIG sector bucked seasonal trends with continuous activity throughout August, issuing EUR24.8bn across 32 new lines—nearly double July's EUR12.475bn. Despite strong demand, most deals (27 of 32) are now trading wider than reoffer spreads.

- Covered bond issuance rebounded to EUR12.5bn from July's EUR2.75bn, while SSA issuance reached EUR21.35bn with EUR8.1bn carrying ESG labels. High yield volumes hit a four-year August high, though historically August is typically a zero-volume month.

APAC

- Regional USD bond supply totaled just USD17.348bn in August, dropping 44% from July's USD31.042bn, marking the second lowest monthly volume in 2025, though exceeding August figures from both 2023 and 2024.

- IG issuances comprised 82% (USD14.26bn) of total supply, attracting an impressive 5.42x average cover ratio despite lower oversubscription rates than July, with issuers generally pricing inside fair value (average -2.8bps NIC).

- Singapore led with USD5bn (29% of total supply) across just 5 tranches, followed by China and related territories (USD4.248bn across 16 tranches), and Japan (USD3.2bn across 5 tranches), while Indian high-yield issuers returned to the USD market for the first time since Q1 2025.

United States

- August high grade issuance reached USD125.9bn (USD99.5bn ex-SSA), exceeding high-end estimates of USD120bn, with domestic issuance at USD85.2bn and Yankee issuance at USD13.95bn—just 13.5% of the ex-SSA total.

- Domestic FIG was the most prolific sector with USD35.85bn in issuance, while notable corporate deals included Eli Lilly's seven-tranche USD6.75bn offering and Chevron's USD5.5bn transaction.

- Market analysts anticipate September issuance to average USD168bn in ex-SSA volume, with estimates ranging from USD150bn to USD180bn, compared to the 2015-2024 September average of USD137.577bn.

- The US HY primary market produced 25 deals (29 tranches) totaling USD23.98bn, with all activity concentrated in the first half of August before the late summer shutdown. All HY ratings sectors gained over 1% (average +1.218%), with CCCs performing best at +1.510% and spreads narrowing across all ratings.

To receive this analysis plus much more, subscribe to IGM. Request your free trial of the service today.