At the time of writing, the DXY USD Index (circa 98.00) is actually little changed from pre-Iran war (Feb 28) levels.

- So, a relatively shock event has proved no game changer just yet with the big focus being on the volatile OIL price. That has gapped/spiked from circa Usd 70/brl to near 120 by March 9. Now, amid so much uncertainty and speculation surrounding de-escalation, ceasefire, resolution or fresh escalation the psychological 100 mark looks like a bearish-bullish gauge in terms of risk and the next path for net energy exporters vs net energy importers.

- Recently, we were wary of the late week USD drop (and OIL etc) on conflict resolution hopes. We struggle with this apparent market complacency, but also acknowledge those moves do imply/indicate that the market is looking to sell broad USD if they get fresh chance.

- This USD bearishness could be Fed and Trump related. A conflict-end could hasten Fed easing, while the US president presides over his tariffs; debt and government shutdown worries/uncertainty; perceived threat to Fed's independence and latterly fallouts with traditional allies over support for the war.

- Such volatile behaviour only goes to raise questions over the existing global financial order. So, markets then look for signs of diversification, debasement et al. Certainly, there has been signs of the latter during the presidency so far when GOLD traded above Usd 5500/oz for the first time in late January.

- At this stage, we envisage few big range breaks as we wait to see the fallout from the war. One pertinent question will surely be which economies ride out the war storm best? Which growth outlooks will be most resilient, vulnerable to higher energy costs, supply shocks etc?

- We're also gearing up for Warsh's confirmation as next Fed chair. Recently, he has been quoted suggesting strong productivity growth and the government’s deregulation agenda are disinflationary and justify lower interest rates.

- Some notable tops in EUR/USD, but uptrend remains very much intact.

- Are both BOJ rate hike expectations and the YEN underpriced?

- GBP outperforms still, but the politics weight lurks.

- Some bulls eye a march on 0.7500 for the RBA fuelled AUD/USD.

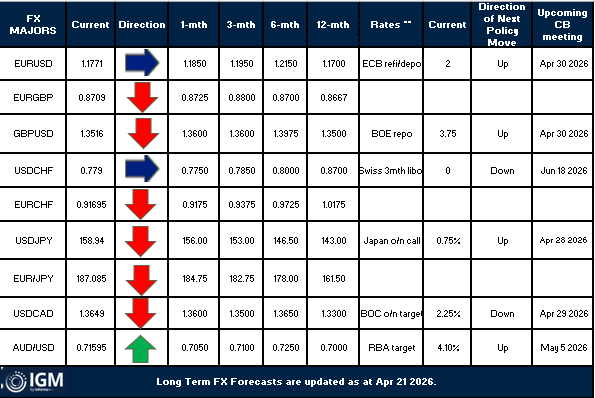

EUR/USD - Three notable tops of 1.2081, 1.1927-29 and latterly at 1.1849, but we still back the uptrend (so long as there is no big escalation in the war, which could threaten market optimism over the Euro zone's 2026 growth outlook). Yield differentials are a prop, with investors still eyeing at least one Fed rate cut this year, while the ECB is tipped to hike as early as June. Flows also matter and Reverse Yankee issuance could be stratospheric in 2026, perhaps Usd 100bln-plus. This could at the very least be viewed as an example of global investors diversifying away from US assets towards in this case the EU.

Unchanged. War duration dependent.

USD/YEN - War and a frothy OIL price has worked to prop in this battle between energy exporter and energy importer. Verbal intervention though is at least working to restrict topside beyond 160.00-46 currently. USD/YEN is the only Dollar winner so far in 2026 and we find the JPY arguably undervalued. Q1's Tankan showed resilient business sentiment, while there is tightness in the labour market and rising wages. So, current BOJ tightening expectations could be underpriced and we do not rule out a semi-surprise hike in H1. Of course, if this is accompanied by Fed easing, a move on 150, perhaps below, could be hastened.

Unchanged. Not prepared to raise estimates whilst price is is sat inside the MOF line in the sand region between 157 - 160.

GBP/USD - A relative outperformer through the conflict so far even as a net commodities/energy importer. Oil/energy price spikes has led to a revision in market thinking on the BOE monetary policy outlook, with a full +25BPs priced by September. However, last week, MPCers Bailey stated we’re not going to rush to judgments and Taylor remarked there’s a high bar to voting for hikes. It's a big week on the UK macro front. We stay date dependent. Politics remains a potential weight, particularly after the Greens' seismic win in late Feb's by-election; Trump's rebuke of the PM on his lack of support for the Iran war and Starmer is under attack on the Mandelson appointment. A leadership challenge stays a possibility and markets' biggest worry of a lurch way left in government cannot be ruled out.

Unchanged. Sub-1.40 trade looks set to continue.

USD/CHF - Real Swiss interest rates remain unattractive, at around 0%, but most other drivers stay net CHF supportive. In early 2026, USD/CHF has made a big sub-0.8000 return to hit fresh multi-year lows of 0.7605. The far bigger watch for the SNB, EUR/CHF, has been relatively stable above 0.9000 for the most part amid speculation of some official Swiss sales of the Franc. The SNB slightly upgraded the 2026 growth outlook after Washington lowered tariffs on Swiss exports and other CHF props through the USD debasement story include Switzerland's persistent trade surplus and thereby inflows; budgetary status (vs France!!) and its neutral ongoing safe haven position (amid; fragile economic growth outlooks).

Unchanged. Looking for 0.7500 to provide some sort of base through the period.

USD/CAD - The Loonie remains a war-time outperformer and no wonder after OIL spiked to fresh multi-month highs of Usd 119.50/brl last month. At this juncture and a CAD prop, the BOC is priced to at least keep its target rate at 2.25%, with a +25BPs about priced for Q4. That might be overdone! Sustained higher oil prices should boost Canada GDP and headline inflation albeit from fairly cool levels. We cannot turn overly bullish here, particularly with the big event risk of USMCA negotiations ahead, as the relationship between the two leaders, Carney and Trump, seemingly remains less than warm.

Estimates unchanged.

AUD/USD - The second best performer since the war started and through 2026 so far. With the Antipodeans viewed as relatively sheltered from the war and a decent chance of a third straight RBA rate hike in May further gains beyond current highs of 0.7222 could be in the offing. If this is accompanied by increased Fed rate cut expectations, big bulls could well target 0.75 over the forecast period, particularly as China growth beat expectations in Q1 at 5.0%. We are on amber alert to raise on a big 0.7200-plus break, but we're also relatively cautious on risk sentiment and the ongoing equities charge. Are pullbacks due?

Estimates unchanged, but on amber alert, particularly if 0.7283-00 goes.