Since the January 14 update, increased volatility has been the theme.

- The broader USD suffering a decline towards Jan's month-end and fresh multi-month DXY USD Index losses (Feb 2022).

- In the interim, there was a return to the “Sell America” theme, with Trump’s disruptive policies generating a reluctance to not only add to US assets among investors, but to diversify and seek alternatives.

- EUR/USD traded above 1.2000; AUD/USD 0.7000-plus and USD/YEN dropped from near 160 to just north of 152 and a -4% slide. The latter coincided with reports the Fed might have participated in USD/JPY selling intervention.

- A USD crisis of sorts panned out amid other US related negatives of Fed independence worries; tariffs, raised geopolitical heat and government shutdown fears.

- Some of those fears have been allayed since. DXY bottoms for now at 95.55 (Jan 27) in a rapidly evolving broader market backdrop, which has seen a big beat in Jan NFPs of 130k (and possible stabilisation in the weakening jobs market) as US growth remains reasonably strong. A school of thought has emerged that much of the USD negatives could now be about priced - a credible Warsh as next Fed chair, a small drop in the geopolitical temperature, a little bit of quiet on the tariffs front.

- Still, the expected two Fed rate cuts in 2026 (but remaining data dependent) should be consistent with net USD bearishness though a dip rather than a lasting collapse.

- The Aussie is standout performer in 2026, independently buoyed by the RBA raising its cash rate target by +25BPs to 3.85% in Feb, as largely expected.

- The YEN has been supported by PM Takaichi's emphatic election win in the Lower House and increasing her mandate.

- EUR/USD remains bid, supported by investor confidence on global growth in 2026 and a continued Eurozone recovery, led by Germany's massive infrastructure and defence spending boost.

- GBP/USD has followed the pack higher, but there are political worries over UK PM Starmer's future and possible lurch (far?) left in the governing Labour Party.

- We get the US mid-term elections in November, which looks another potential ugly obstacle for the fragile USD further out.

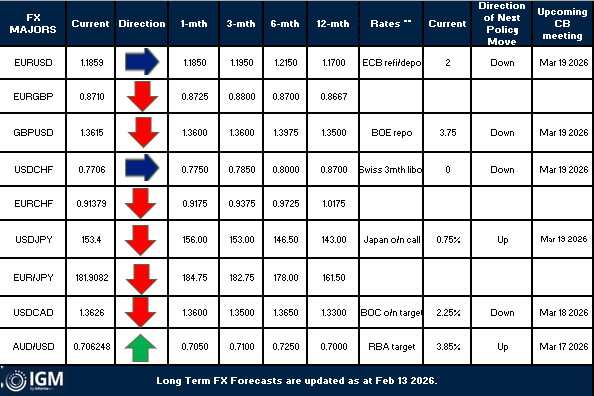

EUR/USD - Last time out, we wrote staying bullish, expecting a 1.20-plus move in 2026. That panned out by Jan 27 to a 1.2081 best since June 2021!

A beneficiary of broad USD weakness though at times it has seemed to miss out on 'flight to quality' flows. If a USD crisis deepens in 2026, the EUR should be primed to benefit more medium-term given the EU is the second most liquid market; viewed as a genuine alternative. Also, while relative optimism persists on the global growth environment, it should continue to favour higher USD hedge ratios. However, ECB's Kocher's has warned the Bank would need to consider another rate cut if further increases in EUR's value (1.25?) start affecting inflation forecasts, while ECB's Villeroy stated EUR's value is an element that will guide policy; USD drop sign of US unpredictability.

Unchanged. Staying bullish, expecting more 1.20-plus moves in 2026.

USD/YEN - A whipsaw start to the year and net sustaining a dive from just shy of 160.00. Biggest negative impacter were reports the Fed might have participated in USD/JPY selling intervention. Such a possible unprecedented step added to the cocktail of weights in the latest USD crisis and sell America theme. Meanwhile, the YEN has been supported by PM Takaichi's emphatic election win in the Lower House, which has increased her mandate. Some firms believe there have been positive signals for more market-friendly policies and there may be a delay of the promised consumption tax cut. Much will depend on Tokyo's ability to keep JGB markets calm. If so, a next BoJ hike could come as soon as March, which would likely be warmly welcomed by Washington as the countries prepare for Takaichi's US visit next month.

Unchanged, but will respond to a sustained fresh selloff through 152.00-10, 150.00.

GBP/USD - Records fresh four years-plus highs of 1.3863, citing the positives of Nov's credible UK budget and the government reaching out to the EU and towards closer relations. Politics though remains a mostly negative focus. This week, Claire Ainsley, who was PM Starmer's policy chief when in opposition, stated the PM is "not out of the woods yet". Betting markets show a 70% probability of Starmer resigning by June 30 and concerns over a lurch left by the Labour Party is unnerving markets and GBP, given the potential fiscal implications. There is a school of thought the BOE stance and market expectations also underprice a pronounced more dovish turn. Latest (Dec, prel Q4) GDP data underwhelmed. Next week's jobs, CPI data are key. We maintain sub-1.40 views for the very most part across the horizon.

Forced to raise near-term estimates pre-data, but stay sub 1.40 for now.

USD/CHF - Real Swiss interest rates remain unattractive, at around 0%, but most other drivers continue very CHF supportive. In the last month, USD/CHF has made a big sub-0.8000 return to hit fresh multi-year lows of 0.7605. In comparison, the far bigger watch for the SNB EUR/CHF, has been relatively stable above 0.9000, and so the perceived intervention threat has been minimised. Last time out, we noted the SNB slightly upgraded the 2026 growth outlook after Washington lowered tariffs on Swiss exports. Other Franc props through the USD debasement story include Switzerland's persistent trade surplus and thereby inflows; budgetary status (vs France!!) and its neutral ongoing safe haven position (amid concerning geopolitics; fragile economic growth optimism story).

- Just small lowering of estimates (so long as 0.7500 holds for the most part!).

USD/CAD - Something to keep an eye on, Wednesday, The House voted to end President Trump’s tariffs on Canada as six Republicans crossed the aisle, signaling growing anxiety over his economic agenda. The move increases pressure on Trump to change course just months before the mid-terms (Bbg). Trump-Carney relations remain cool ahead of upcoming expected tricky USMCA renegotiations, which could lean on business and consumer sentiment. Despite oil continuing to struggle beyond Usd 70/brl and those late 2025 unwarranted more hawkish BOC expectations paring, the CAD has been a beneficiary of USD weakness. However, we have described this as one of the uglier currencies. We stand by that, seeing CAD/Crosses underperformance, as interest rate players continue to focus on employment reports.

Near-term estimates lowered.

AUD/USD - Standout performer in 2026, independently buoyed by the RBA raising its cash rate target by +25BPs to 3.85% in Feb, as largely expected. At least two more +25BPs are priced this year even though Governor Bollard gave minimal guidance, as inflation forecasts were raised, but growth estimates stay cool. Data dependent. Yiield differentials have proved a winner, as has the belief that Antipodean (and Scandi) markets are relatively sheltered from the US-led storm. It could be argued that AUD gains might have come too easy and too quickly. But, net, Aussie does look good above 0.7000 and particularly 0.6767-00 for further gains beyond current 0.7147 multi-month highs.

Raising what we considered were our previously bullish forecasts.