High yield bonds closed lower in the Index today (Apr 10) by - 0.110% but higher for the week by + 0.917%.

Spreads have experienced aggressive tightening, and managed funds had a positive inflow for the first time in eight weeks. The largest HY ETF's also saw a positive inflow for this past measured week.. Market forces exhale into week's end and wait ahead of this weekend's ceasefire negotiations in Pakistan. While both the US and Iran will likely keep some of their cards close to the vest, the world waits with some optimism for steps toward a resolution.

Three new issues in three USD tranches were priced this week totaling $4.05bn in volume.

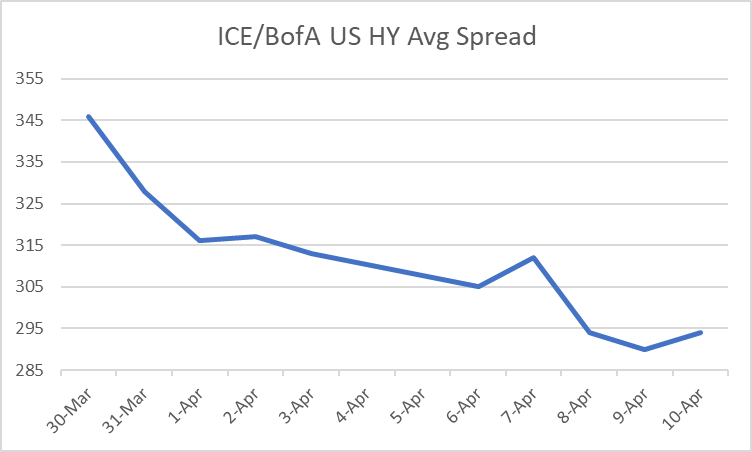

HY Spreads were narrower over the last five trading sessions. The Average was narrower by nineteen basis points, CCCs narrowed by thirty-five basis points to +954. Bs were narrower by twenty-two at +320, and BBs narrowed by seventeen basis point at +177. Within the ICE/ BofA US HY Index, the Average return month-to-date is + 1.323%%. Month-to-date, CCCs outperformed, higher by + 1.504%. For this past week, the CCC rated sector was higher by + 1.274%, Bs are higher by + 0.930%, and BBs are higher by + 0.854%

The featured deal of the week was an upsized $1.75bn (from $1.25bn) CoreWeave Inc. (CRWV) 144a for life / Reg S 5.5nc2.5 senior unsecured note. B1 / B / BB-. via Bookrunners: JPM / MS / GS.. Proceeds from the offering of the Notes for general corporate purposes, including, without limitation, repayment of outstanding indebtedness, and to pay fees, costs and expenses in connection with the offering of the Notes. Priced at 9.75%, +586 vs UST 3.875% 03/31/2031, as 9.75% 10/01/2031 $100.00 9.75% +586. CRWV announced an addition $21bn deal with META to provide cloud AI services. the deal was in conjunction with $3.5bn 5y convert issue. The spread was beyond generous for a tech name with a stable equity price and solid B rating.

The sentiment in the primary market is focused. The primary market is open for business, but it takes a clean well-established or good story issuer to gain investor acceptance to issue notes.

Treasury yields closed the week lower.

The 2-year was lower by -4.5bps to 3.795%. 5-year was lower by -4.2bps to 3.943%. 10-year lower by -2.4bps to 4.317%, and the 30-year was higher by + 0.4bps to 4.909%. The 2s-10s curve added +2bps to 51.5bps

Stocks were mixed at today (04/10) and higher for the week. The Dow was higher for the week by + 3.04%, S&P 500 + 3.56%, NASDAQ + 4.68%, and the Russell 2000 finished the week + 3.97%. Month-to-date (April), the Dow is higher by + 3.40%, S&P 500 + 4.42%, NASDAQ + 6.08%, and the Russell 2000 is higher by + 5.38%. The VIX was higher for the month of March by +5.29 points to 25.25.

In this week's economic data releases. the ISM Services showed higher Prices Paid and New Orders but lower Employment, Decent ADP Employment data, higher Durable Goods Orders Ex-Trans, higher capital Goods Orders / Shipped, FOMC minutes showing risks to both sides of policy mandate from Iran war, lower Personal Income and Spending, in-line but higher Core PCE, moderate to lower Initial and Continuing Jobless Claims, softer GDP, lower real Average Weekly and Hourly Earnings, higher CPI MoM but lower YoY, lower Real Avg Weekly and Hourly Earnings YoY, and UMich Sentiment/Current Conditions/Expectations diving lower.

Weekend event risk of fears continues as the war with Iran at a limited ceasefire. Negotiations will take place in Pakistan this weekend, but Iran says that it will not cease to enrich uranium, and the US says they will not allow Iran to do such. The Strait of Hormuz continues to be highly restricted and contested by the US. US military assets plan to remain in the region until a satisfactory end is in met.

NEW ISSUES THIS WEEK (04/06 - 04/10) :

This week, (Apr 06- Apr 10), there were three (03) USD high yield deals priced in three tranches. Volume for the week was $4.05bn. Month-to date volume is $7.15bn. 2026 year-to-date volume is $85.00bn vs $65.95bn in 2025. 2026 volume is ahead of last year (2025) by + 28.9%.

Avg | +$1.083 | |||

Issue | Price | Bid | Ask | Δ |

UVN 8 7/8 04/15/33 | 100.000 | 101.500 | 101.750 | +$1.500 |

CHBANI 6 3/8 04/15/34 | 100.000 | 101.000 | 101.500 | +$1.000 |

CRWV 9 3/4 10/01/31 | 100.000 | 100.750 | 101.125 | +$0.750 |

TODAY'S MARKETS:

- High-Yield ICE / BofA index is LOWER today (4/10) by - 0.110%. The average spread was wider on 04/10 (+ 04) basis points at 294. The BB sector spread widened by two (+ 02) at 177, The B sector was widened by four (+ 04) at 320. The CCC sector was widened by eight ( +08) at 954.

- Over the prior past five trading days, the Average spread is narrower - 19bps, BB's are narrower - 17bps, B's are narrower - 22bps, and CCCs are narrower by - 35bps.

- The largest HY ETFs are LOWER today (04/10) by - 0.35% on average and are HIGHER by + 0.52% over the past five trading days, on average.

- The CDX HY Index is LOWER today, Apr 10 by - 0.172 at 106.488. The best performers are Domtar Corp. (UFS), The Hertz Corp. (HTZ), and Organon & Co. (OGN). The worst performers were Weatherford International Ltd (WFT), Bath & Body Works Inc. (BBWI), and Hilcorp Energy I LP (HILCRP).

- Oil (WTI May26) is LOWER today by - $1.30 at $96.57 per barrel.

- The Dollar Index (DXY) is LOWER today by - 0.121% at 98.698.

- Spot Gold is LOWER today by -$17 at $4750 per ounce.

ICE / BofA US HY Index 10-day Average Spread

* HY ETF Fund Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Apr 08 | 940m | 3.793bn |

| Apr 01 | -2.853bn | -2.253bn |

| Mar 25 | -600m | 1.409bn |

| Mar 18 | -2.09bn | 1.24bn |

* HY Managed Funds Flow Data *

Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Apr 08 | 807.5m | 3.368bn |

| Apr 01 | -2.56bn | -0.59bn |

| Mar 25 | -1.97bn | 1.42bn |

| Mar 18 | -3,39bn | -1.86bn |

View the latest Credit Matters podcast.

Bond Issuance Summary Table

Company | Size | Structure | Rating | IPT/Price Talk | Bookrunners | Use of Proceeds | Timing |

| Apr 13 week | |||||||

| [Muvico, LLC] (AMC) | $1.73bn | 144a /Reg S for life first lien 5nc2 senior secured note. | Caa2 / CCC+ | Bookrunners: DB (Left Lead / WFS TLD Left Lead) / Citi / GS | net proceeds from the Offering, together with the proceeds from the New Term Loan Facility, and cash on hand, will be used to (i) fund the redemption in full of $400 million aggregate principal amount of 12.750% Senior Secured Notes due 2027 (the “Odeon Notes”) issued by Odeon Finco PLC (“Odeon”), a wholly-owned direct subsidiary of Odeon Cinemas Group Limited and an indirect subsidiary of AMC, (ii) refinance the Company’s existing term loan facility in full, and (iii) pay related fees, costs, premiums and expenses in connection with such transactions. | tbd |