January’s record issuance volume fails to dent oversubscription and pricing

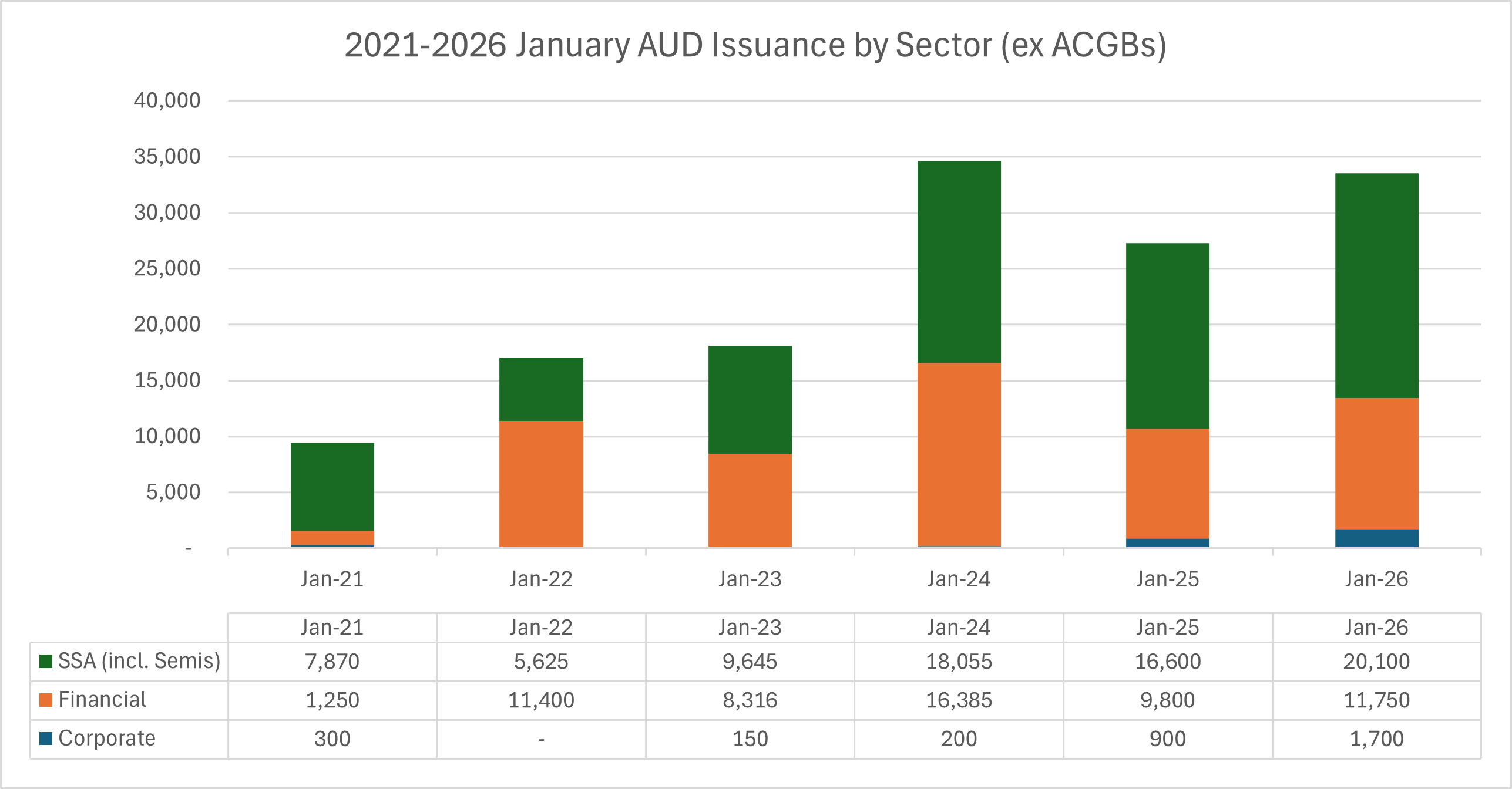

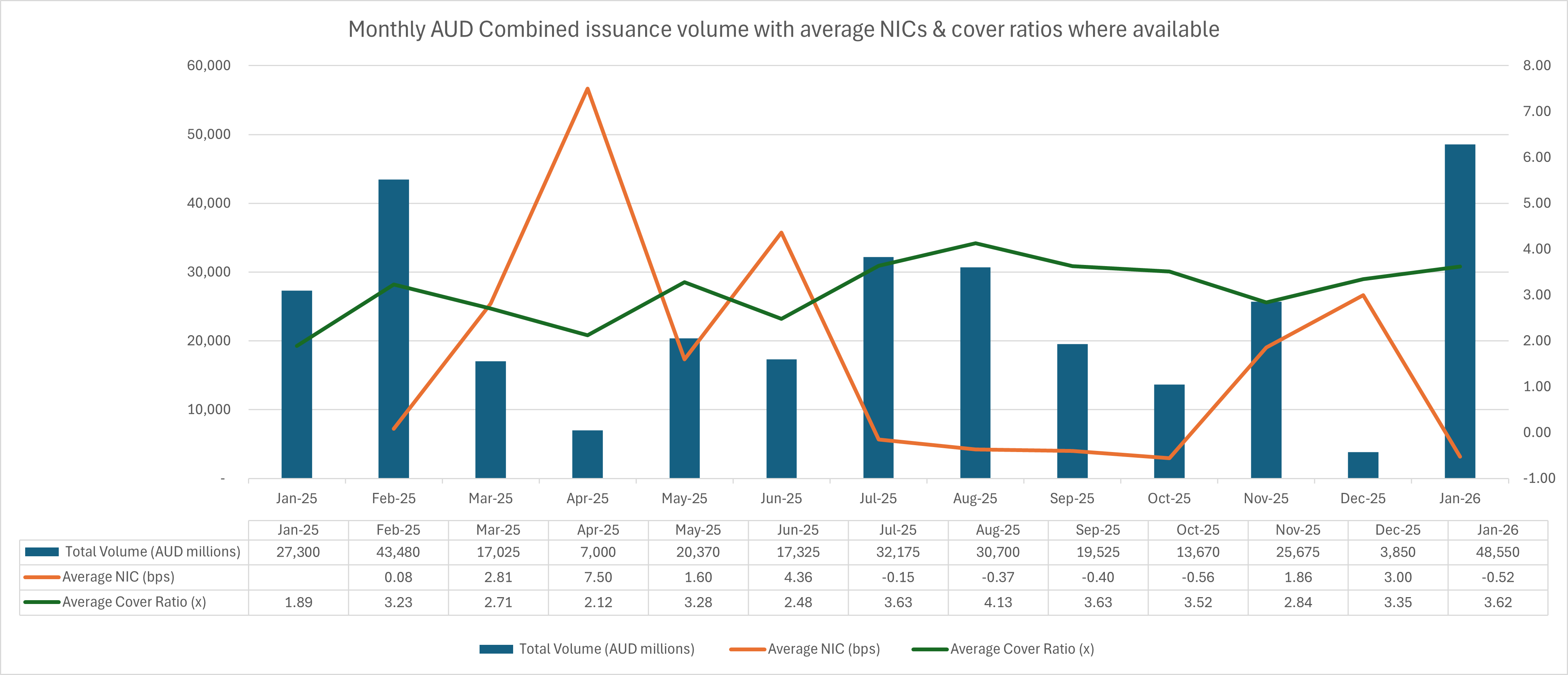

January once again lived up to its reputation as a frenetic issuance month in the AUD primary market, with 26 issuers collectively raising A$48.55bn. That surpassed the A$43.48bn recorded in February 2025, setting a new historical monthly record. And even if we strip out the A$15bn ACGB deal, supply still stood at an impressive A$33.55bn, well above the rolling five-year January average of A$21.3bn and only marginally below the previous record of A$34.64bn set in January 2024. See the chart at the end of this section for more details.

Supply was unsurprisingly led by the SSA sector at A$26.35bn, underpinned by the A$15bn ACGB transaction. Financials followed with A$11.75bn, while Semis and Corporates contributed A$6.75bn and A$1.7bn respectively.

Despite the heavy supply, pricing metrics were equally striking. Investors evidently had fresh cash to deploy in the new calendar year, as reflected in the average cover ratio of 3.62x- the highest monthly figure since we began tracking oversubscription levels in February last year.

And that solid demand allowed issuers to secure attractive funding costs in January, highlighted by an average new issue concession (NIC) of negative -0.54bps. That was fractionally wider than the -0.56bps recorded in October last year- the smallest NIC seen in any month in 2025, but well inside last year's average of +1.79bps.

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

SSA Kangaroo borrowers set fresh volume milestones as spreads grind tighter

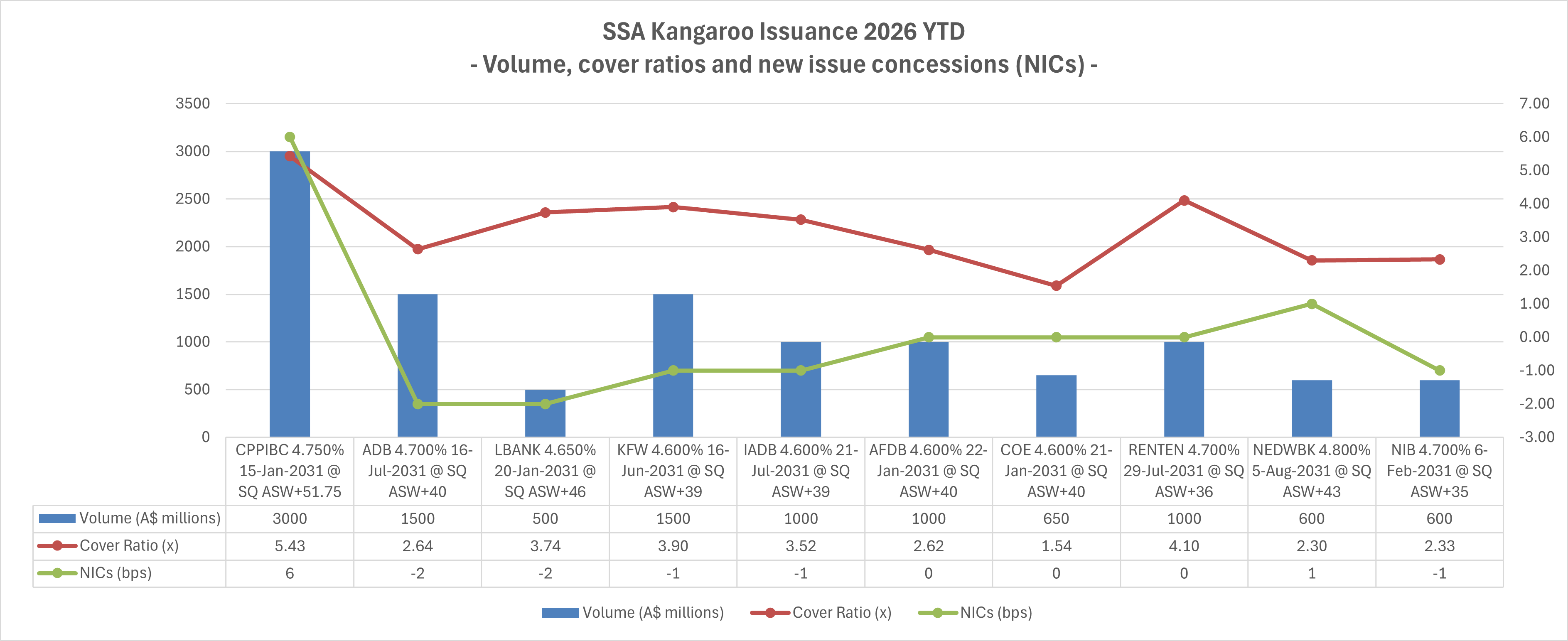

10 of January's 26 transactions came from SSA Kangaroo issuers, generating a combined A$11.35bn of supply. That is broadly in line with last January 2025, when the same number of transactions produced A$11.5bn.

Standing out last month in terms of demand was CPPIB Capital Inc's A$3bn 4.75% 15-Jan-2031 Kangaroo bond. The deal attracted a final orderbook in excess of A$16.3bn, setting a new record for the largest ever orderbook for an AUD transaction (ex-ACGBs), according to IGM's data. The deal also achieved a robust cover ratio of 5.43x- the highest on record for an SSA Kangaroo transaction when excluding sovereign deals from Indonesia and South Korea.

That, however, shouldn't take the shine off the outcomes of other SSA Kangaroo transactions in January, which were also impressive. Alongside CPPIBC, peers including ADB, IADB, AfDB, COE and Rentenbank all printed their largest-ever AUD-denominated transactions in January. And let's not forget NEDWBK and LBANK, which staged successful comebacks with their first AUD benchmark issuance in four years.

Despite record issuance volumes, pricing levels continued to tighten as the month progressed. Mid-curve transactions from ADB, IADB and KFW priced at +40-41bps in the first week of January, while Rentenbank followed with a 5.5-year deal at +36bps in the third week of the month, before NIB wrapped up the month with an even tighter +35bps 5-year print.

And the strong momentum seen for SSA Kangaroo issuance in January is expected to continue as we move into the month of February, with the next wave of names expected to include the likes of BNG, EIB, IFC and KBN, given that those borrowers have typically been active in the AUD primary market early in the year, issuing in four of the past five months of January, according to IGM's data.

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

Financials lock in attractive funding costs as highlighted by tight average NIC of -1.42bps

The financial sector saw A$11.75bn raised by eight issuers in January 2026, exceeding the A$9.3bn recorded in the same month last year. Supply was anchored by CBA’s jumbo A$5bn three-part Senior Unsecured offering, which was the second-largest transaction in January after the A$15bn ACGB issuance.

Despite a relatively modest average oversubscription rate of 2.88x, financial borrowers managed to lock-in funding at an impressive average NIC of negative -1.42bps, marking the second-tightest monthly reading for financial supply over the past twelve months, following the aggregate NIC of -1.56bps in August 2025.

That was supported by BFCM’s A$300m two-part tap of its Jan-2031 lines and Mizuho Sydney’s A$500m 3-year FRN, which both delivered the tightest NIC of the month at -4bps. The latter priced at 3mBBSW+58bps, edging out CBA’s 3-year print at +60bps to become the tightest financial print in that tenor last month. Also notable was UOB Sydney’s A$2bn two-part 5-year fixed and floating-rate transaction, where the reoffer spread of +72bps marked the tightest mid-curve print in the sector in January.

As with SSAs, several volume milestones were achieved by financial borrowers in January. Banco Santander's A$1bn 5-year dual-tranche notes, Newcastle Greater Mutual Group's A$500m 5-year FRN and OCBC Sydney's A$1.2bn 3-year FRN marked the trio's largest-ever AUD transactions.

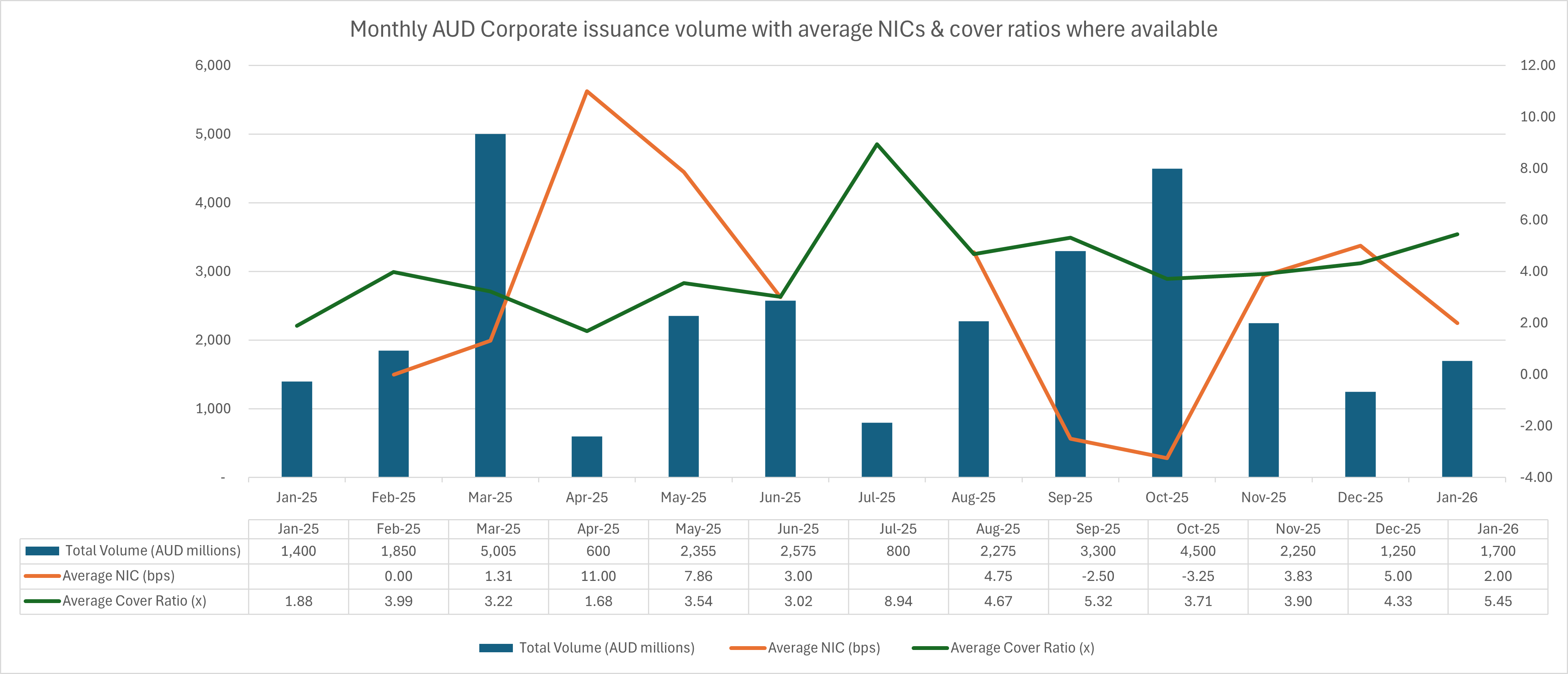

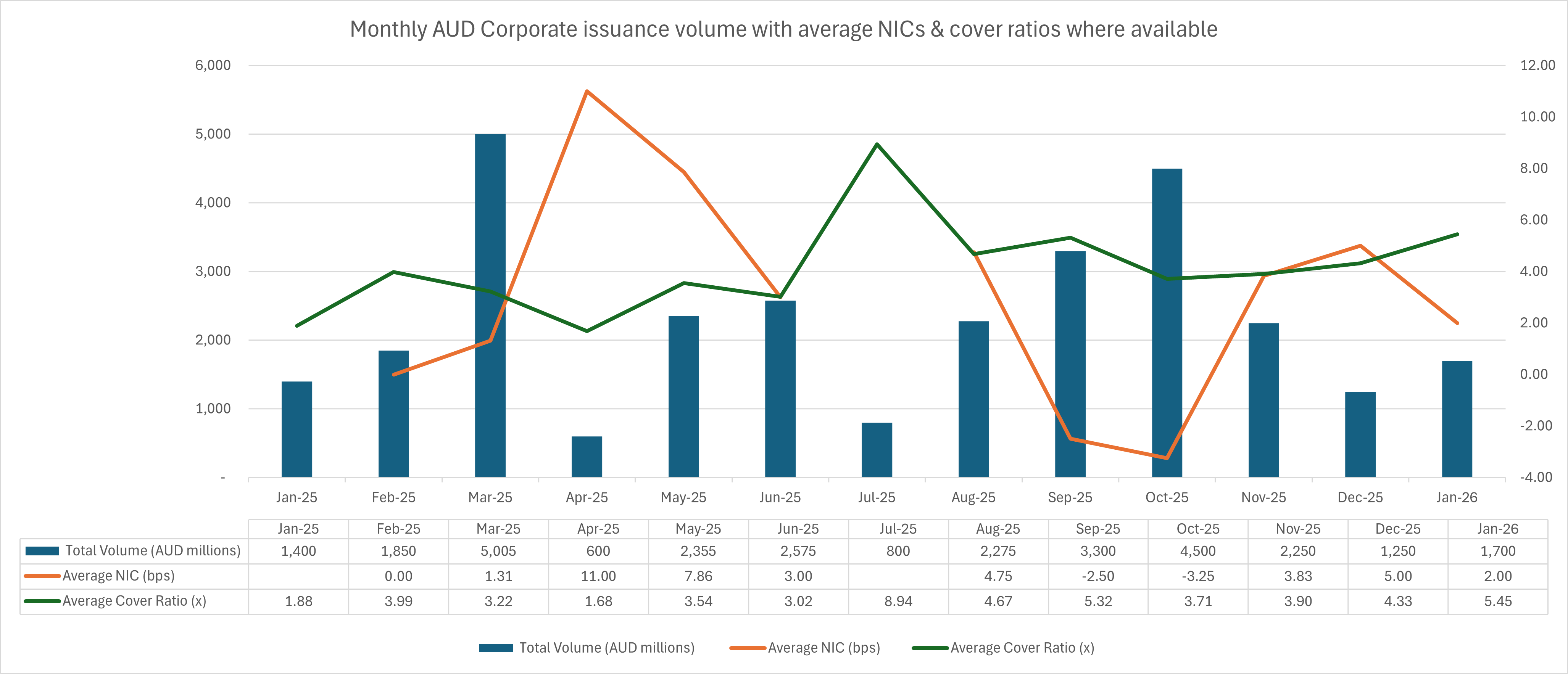

Corporates spring back to life amid AusNet’s blow-out Sub deal and Aroundtown’s debut

It was a relatively subdued month for corporates, with issuance limited to transactions from domestic energy firm AusNet and European real estate company Aroundtown S.A, totalling a combined A$1.7bn. We therefore place less emphasis than usual on the sector’s average NIC (+2bps) and cover ratio (5.45x), given the small sample size.

That said, AusNet's A$1.1bn 30NC10 two-part Subordinated transaction was a blow-out. The sole Subordinated deal of the month across all sectors commanded a robust orderbook of >A$9.04bn, triggering an average cover ratio of 8.18x across the two tranches, setting a monthly record spanning all sectors. This comes as corporate hybrids continue to appeal to yield-seeking investors, amid APRA’s plans to phase out domestic banks’ AT1 supply.

Meanwhile, one of January’s two debuts came from Aroundtown S.A., which closed out the month with its maiden A$600m two-part Senior transaction. Backed by a final orderbook of >A$1.6bn, pricing was slashed by a hefty 18bps and 15bps to reoffer spreads of +167bps and +200bps on the 5- and 10-year tranches respectively.

The other debutant in the AUD primary market in January was state-owned MTR Corporation with an evenly split A$2bn 5- and 12-year Kangaroo transaction. The deal attracted a massive A$12.5bn of orders, enabling pricing to be slashed by a hefty 17bps and 18bps during execution on the 5- and 12-year tranches respectively. The A$1bn 5-year tranche also boasted the second highest cover ratio in January across all issuances at 8.00x.

Issuers expected to front-load in the first half of February ahead of CNY holidays

Looking ahead, we expect February to be a month of two halves, with borrowers likely to front-load issuance ahead of the Chinese New Year (CNY) holidays, which commence on 17th February.

Based on IGM's historical data, it typically takes at least a week after CNY for benchmark issuance to resume. For reference, it took 14 days, 10 days and nine days after the first day of the holidays in 2025, 2024 and 2023 respectively before the primary market saw its first benchmark supply.

Meanwhile, a potential headwind to near-term AUD issuance could be a paucity of issuers in the pipeline. Currently, Auckland-based Watercare Services Ltd is the only confirmed issuer, having commenced a roadshow which is scheduled to conclude this Thursday, 5th February. A potential inaugural 5.5- or 10-year AUD-denominated fixed-rate Senior Secured benchmark may follow, subject to market conditions.

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)

Source: Informa Global Markets (IGM)