High yield bonds closed higher in the Index this week.

Two solid credits priced earlier in the week, but lower rated, riskier deals are leaking into the primary market as risk aversion tests the waters like MIK and CPS this week and BLOCKC last week. AMC Entertainment is expected this coming week. The Index was higher for the week by + 0.186%.

One new issue was priced today:

$1.10bn [Cooper-Standard Automotive Inc.] (CPS) 144a / Reg S for life 5nc2 first lien senior secured note. B3 / CCC+ 1L via Bookrunners: BofA / GS / MUFG / JPM. Guaranteed on a senior secured basis by, CS Intermediate HoldCo 1 LLC and certain of the Issuer's domestic subsidiaries that guarantee certain other indebtedness. The Notes will also be guaranteed on a senior unsecured basis by Cooper-Standard Latin America B.V., which also guarantees the Issuer's senior asset-based revolving credit facility. UoP: net proceeds from the Notes offering, together with cash on hand, to (i) redeem all of its existing and outstanding 13.50% Cash Pay / PIK Toggle Senior Secured First Lien Notes due 2027, 5.625% Cash Pay / 10.625% PIK Toggle Senior Secured Third Lien Notes due 2027 and 5.625% Senior Notes due 2026 at the applicable redemption prices including premiums, if any (collectively, the "Redemptions"); and (ii) pay fees and expenses related to the Notes offering and the Redemptions. Investor call at 11:30AM EST today (02/17). Roadshow through week of Feb. 16, expedited pricing today, 02/20. Biz: global leader in delivering advanced sealing and fluid handling systems for transportation and industrial markets. Hq'd in Novi, MI. IPT: mid-hi 9s%. LAUNCH: $1.10bn at 9.25%. Calls: :03/01/2028 @ 104.625%, 03/01/2029 @ 102.313%, 03/01/2030 @ 100.000%. mw+50. 144a CUSIP: 216762AK0. ISIN: US216762AK06. Reg S ISIN: USU20608AH57. Priced at 9.25% +558 vs UST 4.125% 03/31/2031. s/d 03/04 (t+8).

| IPT | LAUNCH | PRICED |

| mid-hi 9s% | $1.10bn at 9.25% | $1.10bn 9.25% 03/01/2031 $100.00 9.25% +558 nc 03/01/2028 mw+50 |

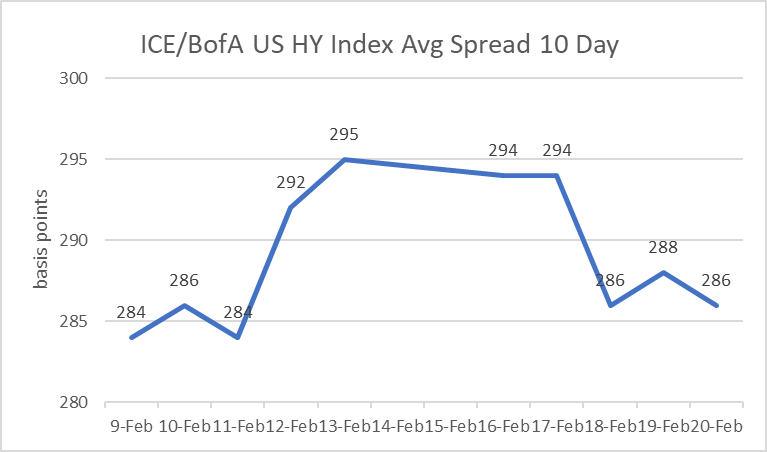

HY Spreads were firmer this week and narrowed by nine basis points to +286 in the Average. CCCs narrowed by nineteen basis point to +887. Bs were narrower by eleven to +312, and BBs narrowed by eight at +170 Within the ICE/ BofA US HY Index, the Average return is higher for the week by + 0.186%. For the week, BBs outperformed. The CCC rated sector was higher for the week by + 0.165%, and. Bs were higher by + 0.184%. BBs closed higher by + 0.196%....

One of the more interesting new issues this week from issuer Michaels Stores. Although the issue did not trade well on the break, it took strong work from the underwriters to get the deal over the line. $2.0bn (from $1.70bn) / $750m (from $950m) Michaels Cos Inc. (MIK) 144a / Reg S 7nc3 first lien senior secured note and 8nc3 2L SN 2-part. B1 / B- 1L. Caa1 / CCC 2l.. via Bookrunners: UBS (B&D) + 1L. JPM (B&D) 2L. UoP: together with borrowings under the Issuer’s new senior secured first lien term loan facility and cash on hand, intended to fund the consummation of the Existing Secured Notes Redemption, the repurchase of all Existing Unsecured Notes tendered in the Tender Offer and the Existing Unsecured Notes Redemption (including any related satisfaction and discharge) and the repayment of the Existing Term Loans and pay related transaction fees and expenses. Both tranches were secured, one 1L and the other 2L. 2L tranche one year longer in tenor, but the spread differential of 250bps shows the sensitivity of the credit and the assets backing the debt. MIK refi package, including $1.0bn 7y TL, will be used to refinance outstanding bonds and the existing Term Loan. The new bonds and loan give MIK a new clean debt package. Moody's gave a one notch upgrade prior to pricing and S&P awarded them a positive outlook. This leaves it up to the company and management to make it work in a niche business. Bonds went out this week $99.25 / 99.50 on the1L tranche, and $96.75 / 97.00 on the 2l tranche (i know, not good). order books were 4.1bn on the 1L, and 1.8bn on the 2L.

The sentiment in the secondary market remains forward looking and isn't reacting to distractions from economic data or geopolitical pressures. Spreads have widened a bit, but not substantially. BBs are outperforming Bs and CCCs.

Treasury yields were higher today by one to two basis points as the data showed mixed results and the Supreme Court struck down President Trumps format for tariffs. The 2s-10s curve was slightly narrower on Friday but flatter on the week by - 4bps to close at 60. Economic data remains relatively solid overall. In today's data, the Q4 GDP missed estimates by a lot at 1.4% and was calculated as high as 5.4% earlier in month by ATL Fed. The low read is hard to reconcile against hot Q4 earnings season.

Stocks were higher for the week after AI spending concerns and its relation to business disruptions subsided. For the week, the DOW was higher by + 0.35%, the S&P + 1.12%, NASDAQ + 1.20%, and the Russell 2000 faded by + 1.83%. The VIX was lower for the week by 1.51 points, closing at 19.09.

In this week's economic data releases was highlighted by a stronger ADP Employment Change, better than expected Durable Goods, strong Dec Housing Starts / Permits, lower to in-line Initial / Continuing Jobless numbers, and good Personal Income / Spending / Consumption data, an solid New Homes Sales. Q4 GDP missed estimates by a lot at 1.4%, PCE and Core PCE were stubborn, and the UMich complex was on the softer side overall.

Weekend event risk of fears has resurfaced. The possibly of an attack on Iran is unlikely, but possible, as negotiations continue and Ramadan is being observed. The US military presence continues to build but the timing of any potential action is uncertain.

NEW ISSUES THIS WEEK (02/16 - 02/20) :

This week, (Feb 16- Feb 20), there were four (04) USD high yield deals in five (05) tranches priced. Volume for the week was $5.10bn. Month-to date volume is $21.29bn. 2026 year-to-date volume is $49.46bn vs $39.98bn in 2025. 2026 volume is ahead of last year (2025) by + 24%.

| ISSUE | PRICE | BID | ASK | CHANGE |

| CPS 9 1/4 03/01/31 | 100.000 | n/a | n/a | |

| MIK 8 1/2 03/15/33 | 100.000 | 99.250 | 99.500 | - 0.750 |

| MIK 11 03/15/34 | 100.000 | 96.750 | 97.000 | - 3.250 |

| GEL 6 3/4 03/15/34 | 100.000 | 100.750 | 101.000 | + 0.750 |

| CNX 5 7/8 03/01/34 | 100.000 | 1000.125 | 100.375 | + 0.125 |

TODAY'S MARKETS:

- High-Yield ICE / BofA index is HIGHER today (2/20) by + 0.026%. The average spread was narrower on 02/20 (- 02) basis points at 286. The BB sector spread narrowed (- 02) at 170, The B sector narrowed (- 02) at 312. The CCC sector was narrower (- 01) at 887.

- Over the prior past five trading days, the Average is narrower by - 09bps, BB's are narrower by - 08bps, B's are narrower by - 11bps, and CCCs are narrower by - 19bps.

- The largest HY ETFs are HIGHER today (2/20) by + 0.07% on average and are HIGHER by + 0.27% over the past five trading days, on average.

- The CDX HY Index is HIGHER today, Feb 20 by + 0.052 at 107.830. The best performers are Xerox Corp. (XRX), CSC Holdings LLC (CSCHLD), and Domtar Corp. (UFS). The worst performers are NCL Corp. Ltd (NCLH), Staples Inc (SPLS), and Avis Budget Group Inc. (CAR)

- Oil (WTI Mar26) is HIGHER today by + $1.24 at $66.34 per barrel.

- The Dollar Index (DXY) is OWER today by - 0.149% at 97.785

- Spot Gold is HIGHER today by + $111 at $5107 per ounce.

ICE / BofA US HY Index 10-day Average Spread

* HY ETF Fund Flow Data *

| Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Feb 18 | 769m | -120m |

| Feb 11 | 889m | 917m |

| Feb 04 | -28k | -616m |

| Jan 28 | 588m | 735m |

* HY Managed Funds Flow Data *

| Week Ending | Weekly Flow ($) | Weekly Trend ($) |

| Feb 18 | -152m | -68m |

| Feb 11 | -84m | -505m |

| Feb 04 | 421m | 188m |

| Jan 28 | 233m | 1.653bn |

To receive this analysis plus much more, subscribe to IGM. Request your free trial of the service today.