(Some) Cryptos are here to stay – implications for bank risk managers

Periklis Thivaios is a founding Partner of True North Partners LLP (UK) and an adjunct professor at the University of Nicosia. Get more insights from Periklis Thivaios on the increasing rise of digital banking and what does this mean for traditional banking at RiskMinds Edge Europe on July 12.

The spectacular (albeit predictable) collapse of the Terra UST stablecoin and the sharp decline in crypto valuations has reignited the debate on the implications of cryptoassets and cryptoliabilities to financial institutions and the financial system as a whole.

While steering clear of the crypto universe may be the easiest (and largely most appropriate?) approach for regulated financial institutions, such a ‘strategy’ comes with its own risks – especially in a changing financial landscape. Therefore, it is better to be prepared for whichever way the future plays out.

We propose a simplistic (albeit pragmatic) framework for managing the risks of participation and non-participation alike. The framework is composed of three main pillars:

1. Monitoring regulatory and industry body developments

2. Monitoring and managing the risks of non-participation

3. Evaluating the risks associated with crypto related business models and, assuming the bank pursues one, managing them actively.

1 – Monitoring regulatory and industry body developments

Whether a financial institution is interested in offering crypto related services or not, it is paramount to stay on top of regulatory and industry body developments.

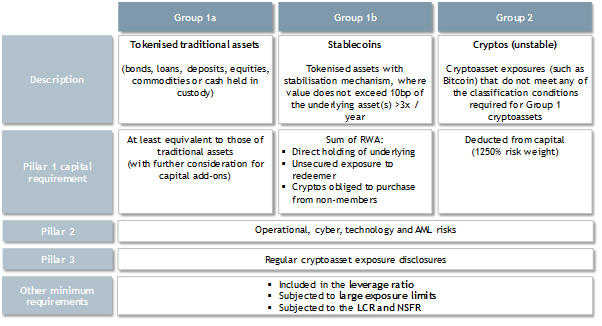

As expected, the most relevant publication comes from the Basel Committee on Banking Supervision (BCBS) [1], outlining their proposals on the prudential treatment of crypto asset and liability exposures (excluding CBDCs). As summarised in the following graph, crypto exposures are split in three groups (namely, tokenised traditional assets, stablecoins and uncollateralised cryptos) with differentiated Pillar 1 capital requirements for each group.

Even though the proposals have been challenged by a number of trade associations [2], the chair of the BCBS has indicated that they are likely to stand by their proposed tough stance [3].

2 – Monitoring and managing the risks of non-participation

Even if your institution has no intention of offering crypto related services, it is important to appreciate the risks of non participation. Such risks can be classified under the following categories:

A. Liquidity risks

a. HQLA availability: stablecoins use liquid assets that are ‘drained out’ of the banking system

b. Funding risks: crypto related firms or stablecoins may hold our certificates of deposit or commercial paper

B. Counterparty risks

a. Indirect credit exposure: due to prime brokerage activities; loans to VCs, family offices and other funds; and/or loans to companies that support the crypto ecosystem (e.g. miners)

b. Indirect investment exposure: to funds holding crypto related assets or stocks

C. Interconnectedness risks

a. Shadow banking: risks in the unregulated corners of the financial system “can quickly find their way to established and regulated institutions”[4]

b. Market shocks: turmoil in crypto markets may have repercussions to the wider economy

D. Business risks

a. Loss of deposits: customer funds may be diverted to cryptos and stablecoins

b. Loss of payment volumes: payment activity may be diverted to stablecoins

c. Loss of customers: younger (in particular) customers may choose to bank with an institution that also offers crypto services

Currently, regulated banks’ direct exposure to cryptos is limited to a handful of countries and constitutes less than 0.05% of RWAs. However, growing client interest and the facilitation of client transactions (clearing of crypto futures, custody, etc.) may result in crypto related services becoming more appealing, despite the risks that they carry.

3 – Assessing, selecting and risk managing crypto business models

Assuming your institution would like to pursue crypto related services, it is paramount to evaluate ex ante the risks associated with each business model, and continuously monitor them for the business models you choose to offer.

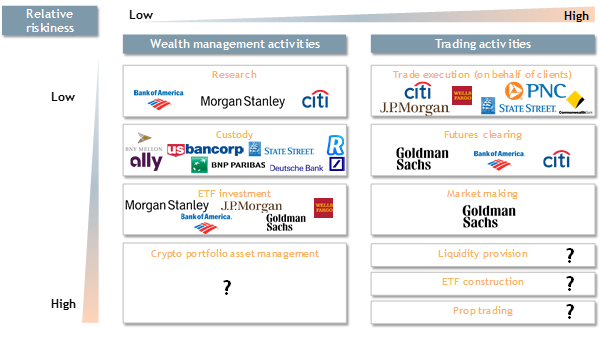

The following illustration summarises a number of crypto related business models, their relative riskiness and some of the regulated financial institutions that are currently offering them.

The first step in the assessment process is to analyse upfront the risks associated with each business model, our appetite, and our capacity for managing them. Subsequently, risks managers need to fine tune the proposed business model(s) and, once the service is being offered, continuously manage the exposures and risks associated with each of them. We have summarised the indicative financial and non financial risks associated with each business model in the following table.

Even though, theoretically, we can constantly fine tune our offering based on our ongoing assessments, attention has to be paid to the in-force ‘contracts’ and our ability to move out of them or our ability to change their terms.

Managing the risks of cryptos is for all banks!

In summary, we do not need to offer crypto related services in order to be exposed to the risks associated with cryptos. Proactive risk managers need to constantly monitor market developments from a customer preference and regulatory perspective alike, and engage in proactive scenario analyses and stress tests to evaluate direct, indirect and interconnectedness risks – at a minimum as part of our ICAAP process.

References

[1] https://www.bis.org/bcbs/publ/d519.pdf

[3] https://www.isda.org/a/ZDWgE/IQ-in-Brief-–-ISDA-AGM-Special.pdf

[4] https://www.bis.org/publ/work1013.pdf