The Research In Finance series: Alternative facts: Where are fund selectors looking to invest beyond traditional asset classes?

European investor demand for different asset classes and investment styles is constantly evolving. One area of growing interest – especially in the retail sphere – is alternative investments, including private assets. But tastes vary between investor type, market, and sector, so just where is new business likely to land?

According to the latest wave of the Research in Finance European Fund Selector Study (EuroFSS), for which we canvassed the views of nearly 900 fund selectors in Q1 2023, 30% of those selectors with allocations to alternatives intended to increase their exposure over the following six months, versus 18% who expected to reduce it, equating to a net change of +12%1.

Of course, each buyer will have their own unique view on this, which becomes more apparent when splitting the data by client type: aggregate responses from retail buyers reveal an expected net change of +14%, and those from institutional buyers show a net change of +10%. The divergence in enthusiasm towards the alternatives subset of private assets is even starker, with a net change of +11% in retail buyers’ allocation expectations, and just +2% for institutional buyers.

Not all alternatives are equal

Alternative investments have been getting a lot of airtime recently as potential inflation hedges. Other investment categories may currently elicit stronger allocation intentions, but EuroFSS highlights the positive overall demand for alternatives too, as investors seek greater portfolio diversification and access to additional areas of investment with strong performance records. From asset managers’ viewpoint, retail buyers’ growing appetite for alternative investments can diversify and expand their accessible client base.

Digging deeper, some rotational activity is in the pipeline, with infrastructure and private equity particularly favoured by European selectors, and with real estate receiving the cold shoulder. This reflects some of the challenges of the current market environment. Real estate valuations are in flux owing to a potent combination of impacts on demand and ease of financing from the Covid-19 pandemic as well as rising interest rates. In contrast, infrastructure holdings are appealing while investors look to inflation-proof their portfolios, as revenues from such investments are usually indexed to inflation.

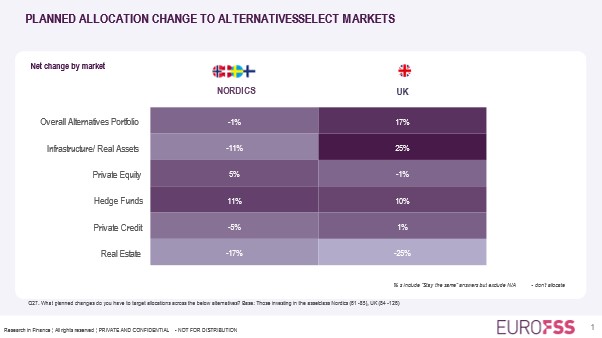

The intensity and direction of allocation intentions can vary across Europe. Neutral or negative demand for real estate is evident in all surveyed markets, with UK selectors particularly averse to that asset class at present (a net change in allocation intentions of -25%) and particularly positive on infrastructure (+25%). While selectors in most other markets are in favour of additional infrastructure investment, Nordic buyers are going against the grain with a negative net change in intentions (-11%). Hedge funds are currently the preferred alternative asset class there, providing a reminder of the Nordic region’s vibrant local hedge fund sector.

In other markets, demand for new allocations to infrastructure is equalled or slightly surpassed by interest in private equity, the exact form of which varies across investor types and markets. Institutional selectors currently rate private equity co-investments a little higher than primaries and secondaries as the most attractive route to accessing private markets, while retail selectors favour primaries over other types.

Breaking down barriers

The greater enthusiasm of retail selectors for alternative investments at present highlights the growth opportunity of increasingly opening such investments to individual investors. Recent changes in rules around European Long-term Investment Fund (ELTIF) investments in the European Union, and the introduction of the Long-term Asset Fund (LTAF) structure in the UK, are among the shifts taking place to make retail investment in alternatives an even more realistic prospect.

However retail and institutional investor cohorts unsurprisingly see different barriers to investing in the alternatives space. Focussing on private assets in particular, retail selectors are more concerned with the liquidity, transparency, and accessibility of these investments, while institutional selectors see regulatory issues as a bigger hurdle – as illustrated in the graph below.

Around two fifths of both retail and institutional investors see high fees as an obstacle to investing in private assets. Addressing these various issues will undoubtedly go some way to attracting further business to this part of the industry, while also helping retail clients to grow their slice of the alternatives pie.

Meet the team at IMpower Incorporating FundForum

We are very pleased to be attending IMpower Incorporating FundForum later this month. Our Founder and CEO, Toby Finden-Crofts will be mediating the FundForum Distribution special focus panel “New research: European brand perception vs reality in different markets”, in which he and a group of global distribution and market leaders from Candriam, Columbia Threadneedle Investments, PIMCO and SSGA will be discussing how to stand out from the crowd and strengthen market position. It promises to be a very thought-provoking discussion which will certainly produce some interesting insights. We look forward to seeing you there!

About EuroFSS

EuroFSS is designed to help asset managers track brand resonance, positioning against competitors and investment trends at both the pan-European and individual market levels. In this latest wave we reveal a rich collection of views expressed by 892 professional retail and institutional fund buyers across eight European markets in Q1 2023. If you’d like to find out more about how Research in Finance can help you with your research requirements, please do get in touch.

Research in Finance are Silver Sponsors of IMpower Incorporating FundForum 2023. Find out more about the event and agenda here >>

[1] NB The difference between the sum of respondents intending to increase or decrease their allocations and 100% is accounted for by those buyers intending to maintain allocations at existing levels.