The winds of change affecting global institutions

After recent tumultuous times, is it time to experience a fresh breath of air in the asset management industry? Jonathan Libre, Principal EMEA Insights, Broadridge Financial Solutions, explains what we will experience on the winds of change.

2018 was certainly a tumultuous year across the global asset management industry. With a sample of nearly $50trn in assets to examine thanks to our integrated dataset, covering retail and institutional business (after any FoF and sub-advisory double counts are stripped away) we are able to see what state the industry was left in as we entered 2019.

Looking purely at the stock of assets, the Americas region clearly leads the way with $30trn but was flat in organic growth terms.

While the APAC region is the smallest with $7trn of assets, it is the most important growth market, with an organic growth rate of 6% over 2018. EMEA, by contrast, shrank in organic terms. It is no surprise therefore that many asset managers are pivoting towards APAC.

While is tempting to focus on the headlines, dissecting the underlying trends produces interesting insights into the behaviours of investors within each region. Some behaviours across different institutional segments are particularly interesting, and three key pervasive trends jump to the fore.

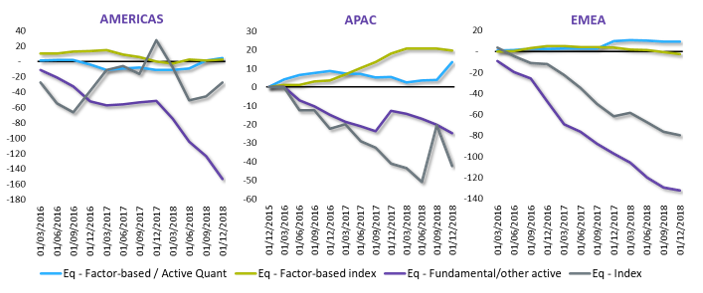

Equities: tailwinds for systematic; headwinds for traditional

Traditional passive and fundamental equities strategies have seen mass redemptions from institutional investors in recent years across all three regions.

Firstly, institutions with fixed liabilities have been de-risking, and this is particularly true for defined benefit (DB) plans in the US and the UK, where the focus has shifted to liability-driven investment. Secondly, institutions often access their equity exposure through other means: DC plans may access it through multi-asset or target date funds, while larger US foundations are increasingly using private markets.

"Many other institutional investors remain in the early stages of ESG adoption. In the US, the zero-sum-game argument that ESG integration necessarily compromises investment performance, has in general not been rebutted."

A third reason for traditional strategies falling out of favour is through the changing composition of equity portfolios, and again this is prevalent across all three regions. In the US and Europe, active quant and smart-beta factor strategies have been protected from these outflows; these strategies are therefore taking up a larger piece of a shrinking equity pie.

In APAC, the story is more positive, and these strategies are actually seeing large inflows. For example, a Taiwanese Official Institution recently issued a large dynamic multi-factor index mandate split across five external managers.

Graph: Cumulative net flow within equities - 2016-2018 - $bn.

ESG: a breath of fresh air

Institutional investors are increasingly incorporating environmental, social considerations (ESG) into their investment portfolios. This trend is also playing out globally, but at different speeds across each region.

EMEA is very much at the vanguard. This is partly driven by the investors themselves, with the large pension institutions in the Netherlands and the Nordics having developed sophisticated internal policies.

In other markets it is driven more by regulation: in France Article 173 asks institutions not just how they are accounting for ESG related risks but are also how they are contributing to a low carbon economy, and in the UK new regulations are forcing ESG onto pension trustees’ agendas.

It is more of a mixed bag in APAC. Some of the largest Australasian pension institutions have developed highly sophisticated ESG polices, supported by internal capabilities spanning integration of ESG factors, positive and negative screening, and even impact investments.

For Japan’s Government Pension Fund, corporate governance issues are key, which is symptomatic of the dominance of large conglomerates over the Japanese economy.

Many other institutional investors remain in the early stages of ESG adoption. In the US, the zero-sum-game argument that ESG integration necessarily compromises investment performance, has in general not been rebutted.

Fiduciaries of corporate pension plans are therefore wary of the risk of litigation associated with ESG adoption leading to inferior investment return outcomes.

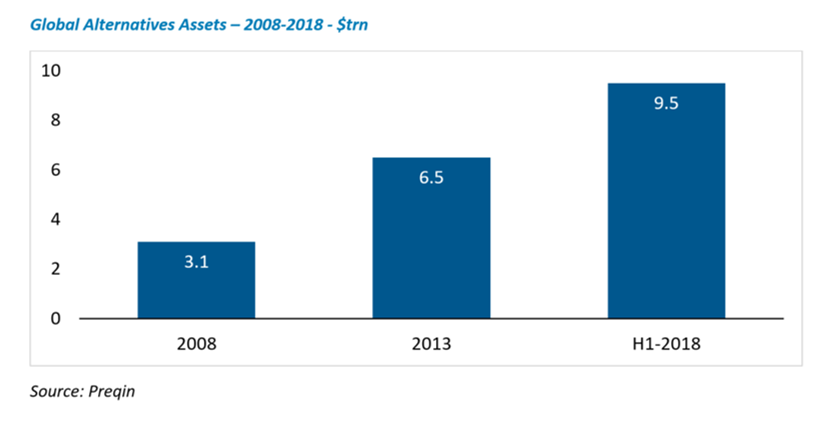

Alternatives: blown away

The one area that has really picked up steam across all three regions is that of the growing interest in alternatives. Over the past 10 years, alternatives assets have more than tripled, from $3.1trn to $9.5trn, and while this phenomenon can be seen globally, the US is very much at the forefront. Some large foundations, for example, are known for allocating more than 50% of their portfolios to alterative assets.

Institutional investors have shown positive allocation intentions to alternatives for 2019, particularly for real assets such as infrastructure, and private markets assets such as private equity and private debt.

In general, these are the asset classes that have enjoyed the greatest degree of client satisfaction, but they also well with growing demands not just for diversification benefits, but also income generation or return enhancement from alternatives allocations.

Systematic strategies, ESG and alternatives are three key drivers of change that are blowing across the institutional asset management industry, but there many more.

For asset managers to compete successfully within global institutional, it is more important than ever to be cognisant of these trends. Just as important, however, is the need to understand the nuances in terms of how how these trends are materialising in different ways across different markets.