We are in the midst of a profound disruption. This technological singularity is expected to cause dramatic and irreversible changes to human civilisation, far beyond typical generational shifts like the smartphone or even the internet.

After extensive research, our conclusion is clear:

Artificial Intelligence is not just another run-of-the-mill innovation; it is a fundamental reconfiguration of how work is performed.

And it’s not just knowledge work. The profit pool from real-world, physical AI—think autonomous cars and robots—is expected to vastly exceed that of agentic AI. To navigate a disruption of this magnitude consensus thinking is the enemy. Passive (and benchmark cognisant) investing face severe challenges as these strategies inevitably must own both the disruptors and the disrupted by design.

The Contrarius edge: Combating groupthink

When Contrarius was founded in 2008, we looked across an investment landscape paralysed by groupthink and uniformity. Our firm was built to be different. We are independent and staff-owned, ensuring our team is completely aligned with our contrarian, bottom-up, valuation-based philosophy. Our already independent-minded research analysts are also physically located in multiple global offices to further minimise groupthink. When it comes to investment research, we shun sell-side brokers and do not meet with company management, ensuring our judgment remains unclouded by corporate narratives.

In a rapidly shifting AI market, this structural independence and rigid, long-term focus, are our greatest assets. It is this approach that directly informs how we are positioning both our Equity and Balanced Strategies, prompting us to currently view the entire universe of listed shares through the lens of three distinct buckets: AI-Winners, AI-Proof, and AI-Threatened.

Bucket 1: AI-Winners

Our first bucket targets the direct beneficiaries of this technological leap. Leading semiconductor shares such as NVIDIA, TSMC, Micron Technology, and SK hynix have been meaningful holdings of the Contrarius Funds at times in the past year. However, the ultimate champions may not be the current consensus favourites. We believe that the largest opportunities (and those with the largest competitive moats) lie in the beneficiaries of real-world AI, which is why our highest-conviction holdings include Tesla and EchoStar (which has exposure to SpaceX). These companies maintain a massive lead in physical applications like autonomous driving, humanoid robotics, and Low Earth Orbit (LEO) operations (such as Starlink).

However, because this landscape changes at warp speed, we must remain extremely nimble. Being unemotional matters. Recently, as valuations in the broader tech sector rose, we took some profits off the table (including from some semiconductor related stocks) and redeployed them in Bucket 2.

Bucket 2: AI-Proof

In recent months we have allocated capital toward companies whose business models are rooted in enduring human behaviours—businesses we believe are highly insulated from AI disruption over the next 5 to 10 years, and beyond.

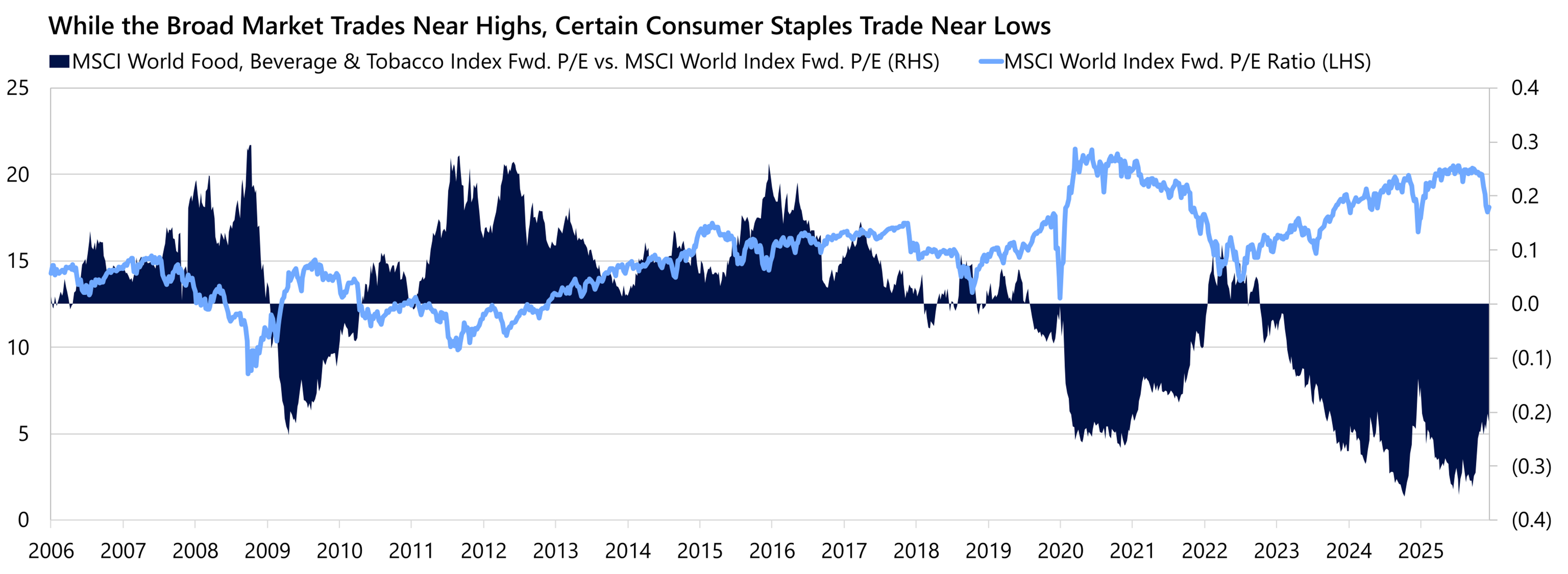

One such area is defensive consumer staples shares. While the broader MSCI World Index trades at above-normal earnings multiples, many of these branded consumer staples companies are offering extremely compelling long-term value.

Source: Bloomberg, MSCI, Contrarius Research. Data as at 31 March 2026.

Source: Bloomberg, MSCI, Contrarius Research. Data as at 31 March 2026.

The Contrarius Funds’ Top 10 holdings now feature some enduring consumer staples shares, including Diageo and British American Tobacco. These cash-generative companies are trading below the levels of a decade ago. While no companies are fully AI-Proof, we believe that companies like these provide an excellent opportunity to preserve and grow investor capital when paired with our high conviction AI-Winners.

Bucket 3: AI-Threatened

Crucially, our contrarian discipline extends to what we actively exclude. The third bucket, AI-Threatened shares, consumes a vast amount of our analytical resources. Our research suggests that a staggering number of listed companies, unfortunately, face fundamental disruption. This bucket includes everything from traditional internal combustion engine automakers to ride-sharing platforms and software application companies. The list is however very long. Most companies are likely to face disruption—many just don’t know it yet. While some of these threatened companies have already seen their share prices fall, we continue to avoid them as they are likely to be insidious value traps.

The power of non-consensus thinking

At Contrarius, we refuse to paint ourselves into a corner. We are perfectly comfortable owning profoundly innovative disruptive forces, such as Tesla or EchoStar alongside a relatively slow-growing liquor or tobacco stock.

The common denominator is that they are trading below our assessment of their underlying value. We are value investors. Full stop. But how one defines “value” matters. We are free from typical consensus considerations of what constitutes “value” and this allows us to go to where we believe the opportunities lie. By balancing our higher conviction AI-Winners with those companies we believe to be AI-Proof—while avoiding the many that are AI-Threatened—we believe that we are positioning the Contrarius Funds to thrive in a fundamentally reconfigured world.

By consistently applying our contrarian philosophy through varying market conditions over time, the Contrarius Global Equity Fund (Institutional Class) has delivered returns of 14.8% per annum net of fees since its inception in January 2009, outperforming the benchmark world index by 3.5% per annum and the average global equity fund by 6.1% per annum (as at 31 March 2026).

For further insights, find Contrarius at FundForum 2026 from 22 - 24 June at The Grimaldi Forum, Monte Carlo, Monaco.

Disclaimer: This is a marketing communication. Please refer to the Contrarius Funds’ Prospectus, Supplemental Prospectus, and Key Investor Information Document before making any final investment decisions. Past performance is not a reliable indicator of future results. Returns may increase or decrease as a result of currency fluctuations. Investments in Contrarius Funds involve risk and places your capital at risk. The value of investments and the income from them may go down as well as up, and investors may not get back the amount invested. This article reflects the views of Contrarius as at 31 March 2026 and is subject to change. This article is for informational purposes only and does not constitute investment advice or an offer or solicitation to sell shares in the Contrarius Funds in any jurisdiction where such offer, solicitation, or sale would be unlawful. Individual securities are discussed for illustrative purposes and do not represent a recommendation to buy or sell. The Contrarius Funds, Contrarius related entities and employees of the Contrarius Group are not subject to restrictions on dealing in relevant securities ahead of the dissemination of this article. Please refer to the Contrarius Funds’ Prospectus, Supplemental Prospectus, and Key Investor Information Document before making any investment decisions. These documents are available in English on our website (www.contrarius.com). Issued by Contrarius Investment Management Limited, regulated by the Jersey Financial Services Commission.

Performance disclosure: Performance data is for the initial series for the Institutional Class units of Contrarius Global Equity Fund, a Sub-Fund of Contrarius ICAV, with inception date of 1 January 2009. Other classes may have higher fees and lower returns. Returns are calculated net of fees in USD, with income reinvested. The fund’s benchmark is the MSCI World Index, net income reinvested. The average global equity fund is the Morningstar category EAA Global Large-Cap Blend Equity.

Source: Contrarius, MSCI, and Morningstar as at 31 March 2026.