Palm oil biodiesel’s contribution to carbon emissions, explained

Linked to deforestation, peatland fires and habitat destruction in South East Asia, palm oil has become probably the world’s most censured monoculture cash crop.

Although it is found in a bewildering range of consumer products – from shampoo, to bread, to low fat margarine – over half of the palm oil supplied to the European Union is used to produce biodiesel, intended to help decarbonise the continent’s vehicle fleet.

Following on from a controversial decision by the European Commission to phase out palm oil biodiesel, we examine the evidence for its land use impacts and effect on net carbon emissions.

Last month, the European Commission moved to single out palm oil as the sole biodiesel feedstock at high risk of contributing to indirect land use change (ILUC).

As a result of this classification, palm oil’s contribution to European biofuels mandates will be capped at 2019 levels over the period from 2021-2023, after which it will be subject to a gradual phase out terminating in 2030.

The move away from high-ILUC biofuel feedstocks is in line with the EC’s previous commitments under the June 2018 revisions made to the Renewable Energy Directive – the key piece of legislation influencing the proportion of biofuels in the European energy mix.

The decision has been greeted with reserved approval by critics of palm oil biodiesel, including European biofuel producers and environmental groups. Although they agree with the core objectives of the act, critics also warn that loopholes left in its wording could still allow substantial quantities of palm oil to be used for fuel in the European Union.

These loopholes exempt palm oil grown by smallholders from the phase out, as well as permitting the use of palm oil by-products.

Want more articles like this? Sign up to the KNect365 Energy newsletter>>

On the other side of the fence are palm oil producers and the governments of the largest exporters, who have argued that phasing out palm oil biodiesel is misguided. Pressure from Malaysia and Indonesia, who between them account for over 85% of global production, was largely responsible for the inclusion of the exemptions.

As the oil palm has a higher yield per-acre than other oilseed crops – close to five times greater than rapeseed, six times greater than sunflower and more than eight times greater than soybean – palm oil producers say that switching to a different feedstock would place even more strain on limited land resources.

This line of argument has particular resonance given that the European Union is currently experiencing a biodiesel feedstock deficit. Biodiesel demand this year stands at 21 million tonnes, according to forecasting by commodity analysts F.O. Licht.

But due to rising demand for vegetable oils and drought damage to European rapeseed crops, there will be a structural vegetable oil deficit of 4.6 million tonnes this year, up 1 million tonnes year-on-year.

The European Union’s total palm oil imports for biodiesel production could top 2.5 million tonnes in 2019, say F.O. Licht, although not all this biodiesel is destined for European consumption.

If loopholes are closed, phasing out palm oil biofuel production over the next decade will bring more pressure to bear on the stretched feedstock market. Other sources will need to be scaled up – either waste feedstocks such as used cooking oil (UCO) and animal fat, or alternative oilseed crops such as soybeans.

Soybean imports from the US are a promising option. As a result of trade tensions, US soybean stockpiles climbed during the final months of last year while Chinese imports plunged. The US has looked to Europe to ease its domestic glut.

A European Commission rule change in January, which permits US soybeans to be used in the production of biofuels in the EU, will help clear the way. Under the previous rules, the EU had been shipping back soybean oil by-product after importing the crop to produce animal feed.

But turning to other crop-based feedstocks raises an important question. Does this approach really make sense when the oil palm produces more oil on less land – and substantially more at that?

The reason it does is that palm oil is at present an almost uniquely harmful feedstock. Yield per acre is not the best metric to use when assessing its contributions to net carbon emissions.

Because palm oil cultivation competes directly with the conservation of high-carbon stock land (such as peatland and virgin rainforest), it has a disproportionate impact on the climate relative to the area under cultivation.

This is not to say that there could be no role for palm oil biodiesel consistent with global climate targets if it were sourced sustainably. Indeed, a number of different sustainability certification systems for palm oil exist, with varying levels of credibility.

But genuinely sustainable palm oil production accounts for a vanishingly small percentage of the growth in global output. Establishing sustainability is also fraught with complications, from accurately tracing a given batch to the land on which it was grown, to the issue of demand for unsustainable palm oil simply being taken up by regions with lower sustainability requirements.

Land use impacts of palm oil cultivation

On the Union of Concerned Scientists’ very informative website, there is a table entitled “Each Country’s Share of CO2 Emissions”. Looking through it, you’ll see that the top four or five emitters are the world’s most industrially intensive economies.

Scroll further down, and at rank 13, sandwiched between Mexico and South Africa, is Indonesia. As only the 16th largest economy in the world, its more modest ranking seems appropriate.

It’s also somewhat misleading. A closer look at the table will show that what’s actually being ranked isn’t a country’s overall CO2 emissions, but its CO2 emissions from the combustion of fossil fuels. Often treated as the same thing, they are not.

Factor the full range of emissions sources in – most significant among them, land use changes – and suddenly things look very different. Indonesia is in fact the world’s fifth largest emitter of greenhouse gasses, due primarily to deforestation and the destruction of the country’s peatlands.

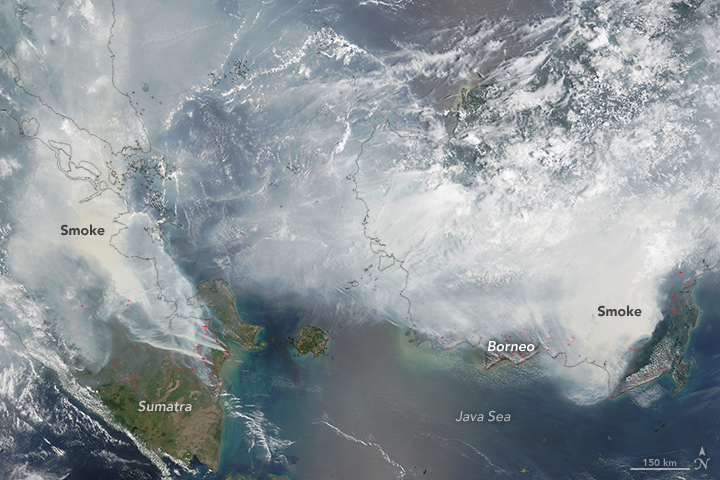

During the late summer and early autumn of 2015, these emissions reached crisis levels. Fires burning on the islands of Sumatra and Borneo released more carbon into Earth’s atmosphere over a single season than the Brazilian economy does over an entire year.

The smoke from these fires was clearly visible from space (as can be verified in the image below). It resulted in what became known as the 2015 Southeast Asian Haze, a persistent pall of polluted air that blanketed a large swathe of Asia for approximately four months.

Peatland fires over Indonesia. Source: Nasa Earth Observatory

One study estimates that the toll in pollution-related deaths taken by the 2015 South East Asia Haze may have been as high as 100,000.

Fires during Indonesia’s dry season are a natural phenomenon. But their impact has been greatly intensified by illegal slash-and-burn practices used to clear virgin forest and peatland to make way for cropland, the majority of which is used to produce palm oil – a highly lucrative commodity for which there is continuous global demand.

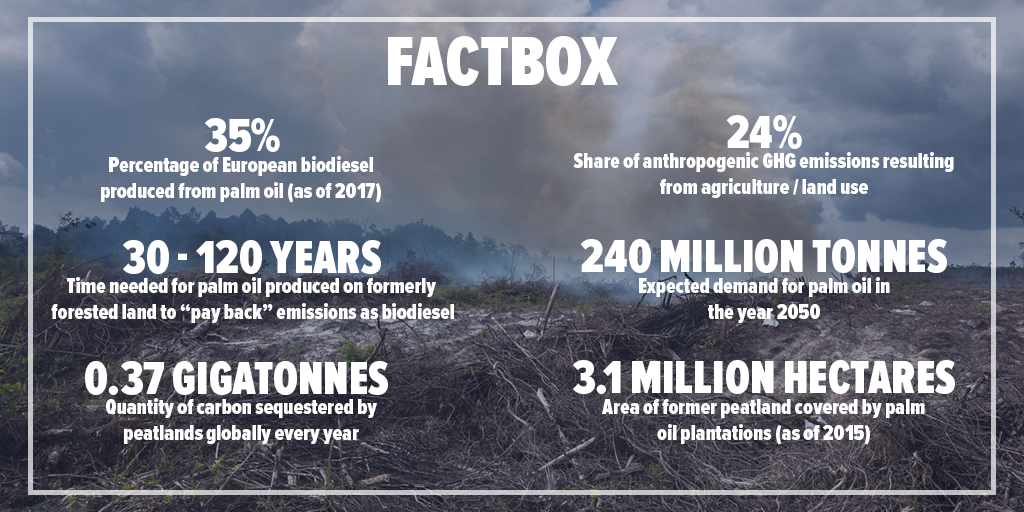

Between 1995 and 2015 palm oil demand has quadrupled, increasing from 15.2 million to 62.6 million tonnes per annum. It is expected to quadruple again by the year 2050, when it will reach 240 million tonnes.

The land area devoted to oil palm cultivation has increased commensurately. The total area covered by oil palm plantations in Indonesia was 2.6 million hectares in 1990. By the year 2014 this had increased to 10 million hectares, with 15 million hectares under oil palm cultivation globally.

Of the expansion in crop area given over to palm oil between the years 1990 and 2015 in Indonesia and Malaysia, 40 to 53% occurred on land with high carbon stocks, according to analysis conducted by the ICCT.

It should be observed that European demand for palm oil biodiesel is not the main culprit in driving harmful land use change. Asia accounts for two thirds of global demand for palm oil, much of which goes to India. Even when considered as a bloc, the European Union is only the third largest importer of palm oil globally.

Nevertheless, palm oil biodiesel commands close attention because the consequences of land use change are so much at odds with the stated objective of using plant-based fuels to counter emissions from transportation.

The logic for biofuels use is that, although biofuels release carbon when combusted, energy crops are a renewable resource which have only recently taken this carbon in from the atmosphere.

This means that, unlike with petrol or diesel, emissions from biofuels are essentially a closed loop. The only unrecoverable emissions occur as a result of the fossil fuels and fertilisers consumed during their production.

In many cases, this logic proves sound. The European Renewable Ethanol Association, ePURE, estimates that the average GHG savings for European ethanol (most of which is produced using cereal crops like corn or wheat) are 70% relative to fossil petrol. Other feedstocks, such as sugarcane, are capable of delivering GHG savings of 90% or higher.

When high carbon stock land is cleared to make way for an energy crop, however, the numbers stack up differently. The massive release of carbon induced by land clearance means that – for a period of decades or centuries – emissions reductions achieved with biofuels will not offset the carbon released in order to produce them.

According to a 2017 study on palm oil by the European Commission, the window for achieving “net carbon gain” from palm oil biodiesel after forested land has been cleared is between 30 and 120 years.

As peatlands are a vitally important carbon sink, clearing them means that it takes even longer - “several hundred years” before there is a net carbon gain. The study also estimates that clearing land with fire adds an extra 18 years onto the time needed to deliver emissions savings.

The significance of land use change when assessing the climate impact of a given feedstock is illustrated by the fact that, on certain types of land with low carbon stocks – such as grassland or scrubland – planting oil palm can actually result in an immediate net carbon uptake.

This is the reason why effective sustainability criteria for palm oil, at least in theory, could help to deliver a product with a much more modest climate impact. It’s also the reason why low-ILUC biofuel feedstocks, which present little risk to high-carbon stock land, can still be used to achieve appreciable emissions reductions on realistic timescales.

A study released by the European Commission in 2016 comparing the land use impacts of various feedstocks found no significant link between the loss of high-carbon stock land and the expansion of sugarcane or rapeseed. More significant impacts were observed for soybean, mostly through deforestation in Latin America.

The most severe impacts were, unsurprisingly, linked to palm oil.

These finding were corroborated by the EC’s assessment in February. The definition provided of high-ILUC feedstocks set a minimum threshold of 10% of expansion in cultivation area taking place on high carbon stock land.

Based on satellite map analysis conducted by the World Resource Institute and the Sustainability Consortium at Arkansas University, the EC found that the figure for palm oil expansion from 2008 – 2015 was 45%. The figure for soybean was 8%.

A final point on the land use impact of palm oil is that, although cultivation has already led to the conversion of millions of hectares of high carbon land, the bulk of the damage that could be done, has yet to been done.

Of the 27.1 million hectares of peatland remaining around the world, 14.7 million are in the largest palm oil growing regions. As of 2015, only 3.1 million hectares of former peatland had been replaced by oil palm plantations.

This means that establishing effective sustainability metrics is of the utmost importance going forward. But meeting the bulk of palm oil demand sustainably will be near impossible so long as that demand, and the land area needed to supply it, continues to expand.

Bringing an end to palm oil biodiesel in Europe

Although European biodiesel consumption only accounts for a fraction of global palm oil supply, plans to eliminate the feedstock have already sparked outcry from producing countries. Malaysia has threatened a WTO challenge against the European Union, as well as a suspension of purchases from European arms manufacturers. Indonesia has warned that it may pull out of the Paris Climate Agreement.

In a time of increasing trade tensions, the European Commission may find itself pressured to take a less contentious and less decisive path. But if anything, it is not acting decisively enough.

The loopholes left in the current phase out plan risk leaving open a backdoor as large as “current consumption levels,” according to Laura Buffet, Clean Fuels Manager at the European Federation for Transport and Environment.

The argument for automatically exempting palm oil produced by smallholders from the high-ILUC category is itself questionable. Much of the palm oil sold by the largest producers is grown in small, independently owned plantations and sold to big mills, meaning that there is little evidence for a link between average plantation size and land impact.

Furthermore, although the 2030 end date set for the phase out will prevent any shocks to feedstock availability, in the context of a target to cut European CO2 emissions by 40% by the same date, it may not prove ambitious enough.

What is needed is an approach to decarbonisation that fully recognises the relationship between using biofuels to reduce emissions from transport and optimising the emissions profile of agricultural land.

For years, the biofuels industry has complained (with some justification) that the European Commission has been unduly skeptical about the role of crop-based biofuels.

At the same time, the EC’s policies were actively incentivising biodiesel producers to import palm oil, the feedstock most at risk of driving deforestation and loss of high carbon stock land. European imports of palm oil increased 15% in 2010, the year after the first Renewable Energy Directive was published.

Contradictory signals on bioenergy have been characteristic of policy decisions at the European level.

Forecasts released by major energy and climate agencies, from the International Energy Agency to the Intergovernmental Panel on Climate Change, are less ambiguous: bioenergy will have to play a major role over coming decades if the world is to meet its climate targets.

But support for bioenergy should not be construed as blanket approval for crop-based biofuels, no matter the source. Not all biofuels are the same, and responsible sourcing is critical.

In regions with a large proportion of high carbon stock land – such as South East Asia – the risk of biofuels production having unwanted land use impacts is much greater. Likewise, the longer and more opaque the supply chain, the more difficult it is to be certain that a given feedstock is grown responsibly.

By planning to eliminate palm oil biodiesel, the European Commission has taken a positive step towards enabling the use of more sustainable feedstocks. Now it needs to ensure that this plan really delivers.