State of the Biofuels Industry 2018

Last month, KNect365 Energy staged the World Ethanol & Biofuels State of the Industry Survey. We asked our international subscriber base of ethanol, biofuels and energy industry executives their opinions on a range of key issues affecting the market in 2018. The results are now in.

Read on for a summary of the background to each topic, and our analysis of the responses we received.

China’s Ethanol Mandate

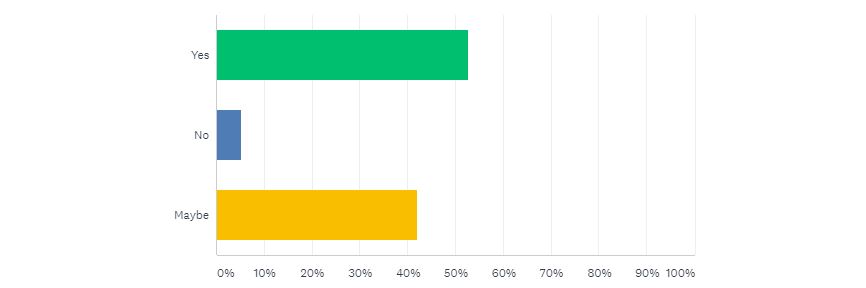

What we asked: “Do you think it is likely that China will follow through on its E10 ethanol mandate?”

Background in brief: China is the world’s largest car market – so it was not surprising that the Chinese government’s declaration of a proposed E10 blend mandate late last year caused some buzz among ethanol professionals. One of the motivations for the proposed mandate, which is due to come into force in 2020, was to find a market for China’s massive surplus corn stock. However many ethanol producers elsewhere in the world suspected that an E10 blend rate would also help to generate a thriving Chinese import market for ethanol.

That said, the proposal has been met with some scepticism among ethanol industry stakeholders who worry that Chinese policy makers may backpedal on imposing such a stiff target.

The response we received:

Analysis: A slim majority of responses to the question were positive - but there was a great deal of uncertainty present too. Doubt may stem from the fact that China will need to add 3.6 billion extra gallons of additional ethanol capacity onto the approximately 1 billion achieved in 2016, by any measure an imposing growth rate. The ongoing battle in the U.S. surrounding the nation’s E10 mandate may also be stoking fears of an oil industry fightback in East Asia.

The Trump Administration and the RFS

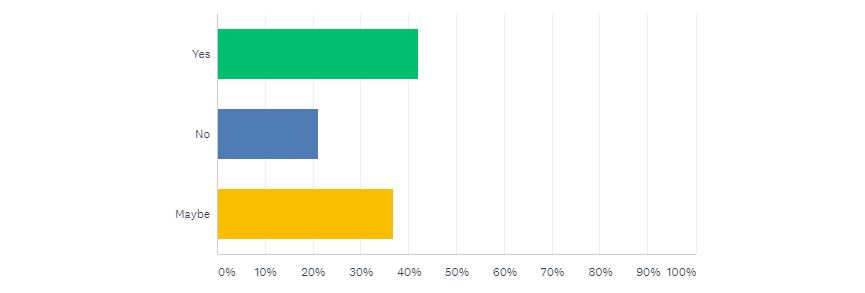

What we asked: “In your opinion, will the Trump administration get around to “reforming” the RFS this year?”

Background in brief: The renewable fuel standard (RFS) (which mandates a 10% blend rate for U.S. gasoline, and imposes a system of RIN biofuel credits on refiners) is an ongoing source of contention between U.S. ethanol producers and oil refiners. Although the Trump administration has announced its intentions to reform the RFS on several occasions, doing so has proved politically contentious due to Trump’s strong voting constituencies in both “corn states” and “oil states”.

The RFS has come under sustained criticism from oil majors on the grounds that it imposes unreasonable costs on refiners and inhibits the free operation of market forces. There are also suggestions that the RFS presupposes significant market penetration for cellulosic biofuels by the mid 2010’s, which has yet to materialise.

Rumoured changes have included capping RIN prices, lifting seasonal restrictions on high-ethanol gasoline sales, exemptions for smaller refiners, and switching from an ethanol blend mandate to an octane performance standard.

The response we received:

Analysis: The political drama surrounding RFS reform has been a quickly moving situation. It is therefore likely that the results would have been influenced by the time of response. Shortly after the survey’s release, news emerged of an impending decision by the administration on how to reform the RFS – only for this to be “delayed indefinitely” several days later. The uncertainty shown in the responses is a fairly accurate reflection of the news cycle’s mixed messaging around the topic.

We also asked: “What changes will the Trump administration make to the RFS?”

The response we received:

There were a number of additional suggestions from respondents too, including an extended waivers program, raising the blend rate to 15%, and applying RINs to ethanol exports. One respondent also suggested that the only solution to the dilemma would be a new American presidential election.

RED II and the EU’s Protein Strategy

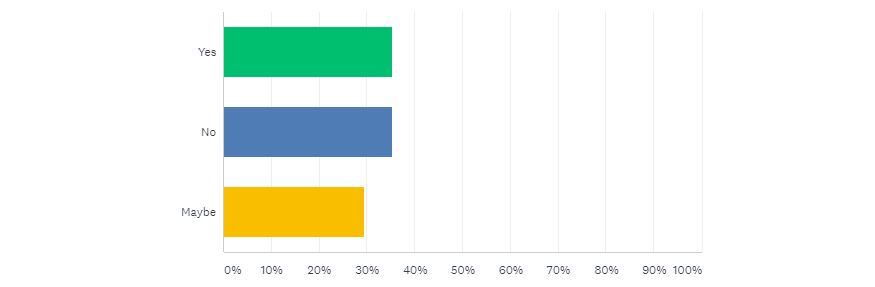

What we asked: “Will conflict with the EU’s strategy to reduce protein imports be enough to cause a reconsideration of RED II?”

Background in brief: RED II, an amendment to the EU’s Renewable Energy Directive, was proposed in 2016 and slated to come into effect in 2020. In its original form, RED II aimed to scale back the contribution made by crop-based biofuels over a ten year period, in favour of a higher share of cellulosic biofuels.

A key criticism of the directive was that it came into conflict with the European Commission’s objectives in drawing up an EU-wide “protein strategy”. Ethanol producers and farmers’ associations argued that co-products from the production of crop based biofuels are a vital source of protein-rich animal feed, so phasing them out would increase the European Union’s dependence on protein imports.

As of June 14th – shortly after this survey was released – the final version of RED II was agreed upon by the European Parliament. This version of the directive replaced the aim of phasing out crop based biofuels with the softer measure of capping their contribution at the levels reached by 2020.

The response we received:

Analysis: As can be seen, the results for this question were divided right down the middle. As RED II has in fact been adjusted to retain a higher contribution of crop-based biofuels, the optimists seem to have been borne out – although it is difficult to say whether the decision was influenced more strongly by the need for domestic protein production, or by the prohibitive costs of cellulosic ethanol production on the scale originally envisaged.

The Market for Bioplastics

What we asked: “Will public outcry over plastic waste translate into a growing market for bioplastics?”

Background in brief: Over the past year, public concern over the scale of the plastic waste problem has drawn increasing attention to solutions, from clean-up programmes, to banning single-use plastics and introducing biodegradable alternatives produced from biological sources. As of November 2017, bioplastics represent approximately one percent of the 320 million tonnes of plastic produced annually, the European Bioplastics association estimates.

The response we received:

Analysis: The results for this question are unambiguously positive. Unlike climate change, recognition of plastic waste as a valid environmental concern seems to extend across political divisions. It is encouraging to see that there is optimism on the part of the ethanol and biofuels industry about the ability of plant-based alternatives to make a genuine contribution to solving the problem.

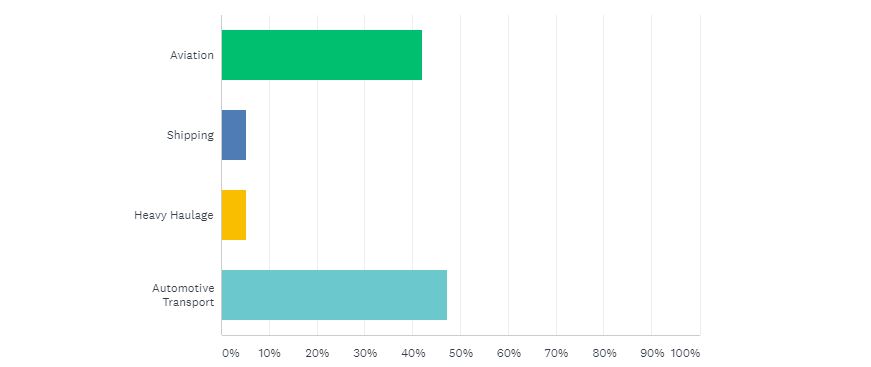

Demand Growth by Sector

What we asked: “Which of the following industries do you predict being the biggest growth market for biofuels?”

Background in brief: At present, the vast majority of biofuels produced worldwide are used by the automotive sector. With the uptake in electric vehicles by the consumer market, however, attention has shifted slightly to forms of transport which are harder to electrify – heavy haulage, shipping and aviation.

The response we received:

Analysis: The strong showing for automotive transport in the results received indicates that, as yet, the biofuels industry is not unduly worried by the growth of electric vehicles. This sentiment is in line with the International Energy Agency’s observation that the growth rate of the EV fleet has declined in recent years, from a growth rate of 84% in 2014 to 59% in 2016. The IEA also estimates that conventional biofuels will still account for 92% of renewable energy consumption in road transportation by 2022, with electric vehicles making up just 1%.

Out of the other sectors listed, aviation was by far the most popular choice. This is likely because biofuels have so far proved to be the only credible option for decarbonising long distance air travel (whereas both shipping and heavy haulage can expect to see other fuel sources and solutions implemented). The result also comes off the back of several promising developments for sustainable aviation, including the agreement of a “strategic collaboration” between Shell Aviation and SkyNRG in May to advance the use of sustainable aviation fuel.

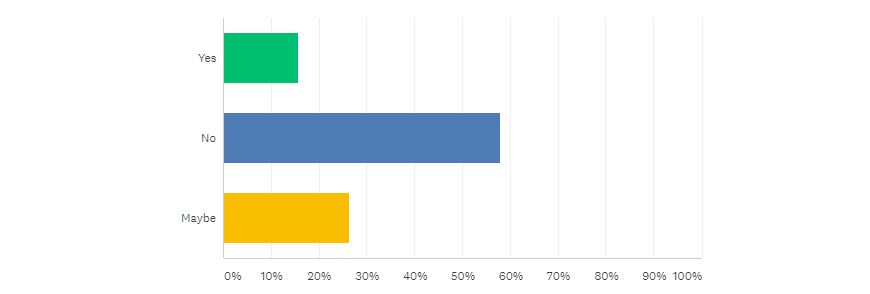

Lipid-Based Biofuels

What we asked: “Will lipid-based biofuels make a meaningful contribution in the short to medium term?”

Background in brief: Lipid-based biofuels, primarily derived from algae, have for some time been promoted as a promising choice as their use eliminates concerns about land utilisation and food security. At present, however, the algal biofuels industry is still mostly limited to research and development. Obstacles to algae’s commercial viability include selecting more suitable strains, encouraging demand for algal co-products and developing better mechanisms for nutrient circulation and light exposure.

The response we received:

Analysis: The results suggest that the industry is still some way from accepting lipid-based biofuels as a realistic near-term option. Such scepticism is unsurprising given the troubles run into by over-optimistic algal biofuels start-ups over the last decade. Many such companies have sought to pivot into other markets.

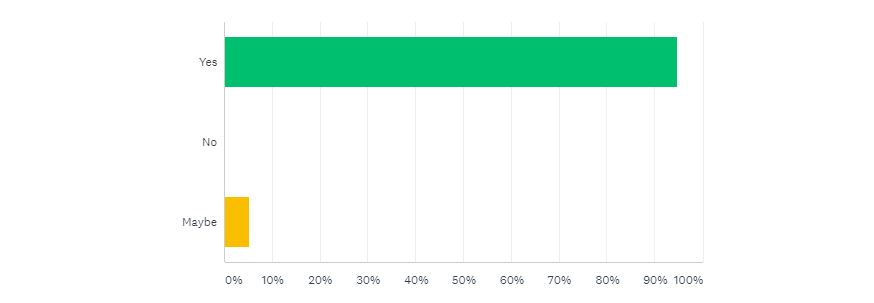

Biofuels Still Essential for Decarbonisation

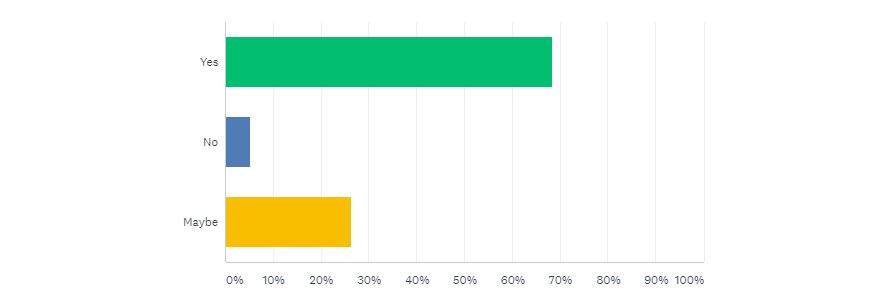

What we asked: “Are biofuels essential for meeting the 2°C temperature rise limit specified by the Paris Climate Accord?”

Background in brief: To remain compliant with the Paris Climate Accord, global carbon emissions will need to be limited to a total of 240 billion tonnes over the years until 2050, beyond which they will have to be effectively zero. Keeping emissions from transport within this carbon budget will be particularly challenging, as transport is the “only major EU sector where emissions today are well above their 1990 levels”.

The response we received:

Analysis: The responses to this question speak for themselves. Biofuels aren’t going anywhere if the industry can make its voice heard.

The Next 12 Months

What we asked: “Do you have any predictions for the biofuels industry over the next 12 months?”

Some of the responses we received:

- “More countries will join the bandwagon by implementing a mandated biofuels mix”

- “Demand will continue increasing slowly”

- “More problems on the way with the EPA and the Trump administration”

- “Market to remain stable as Brazil blends for fuel with oil prices on the up”

- “Growth in Asia will be more significant. Ethanol will represent a major share of total growth.”

- “The situation is very volatile at the moment. But looking at the crude prices, the biofuels industry will have a good time in the near term.”