There are very few certainties in investing and one of the certainties is uncertainty – financial markets do not like uncertainty. Unfortunately, uncertainty is running rampant and has been driving the market performance this year and it makes for difficult conversations with your clients.

Has your call volume from concerned clients increased recently in response to the uptick in volatility?

By leveraging Zephyr’s data and analytics, here is recap of the current market dynamics impacting market volatility and we provide analysis and data that can help with some of those difficult conversations and decisions.

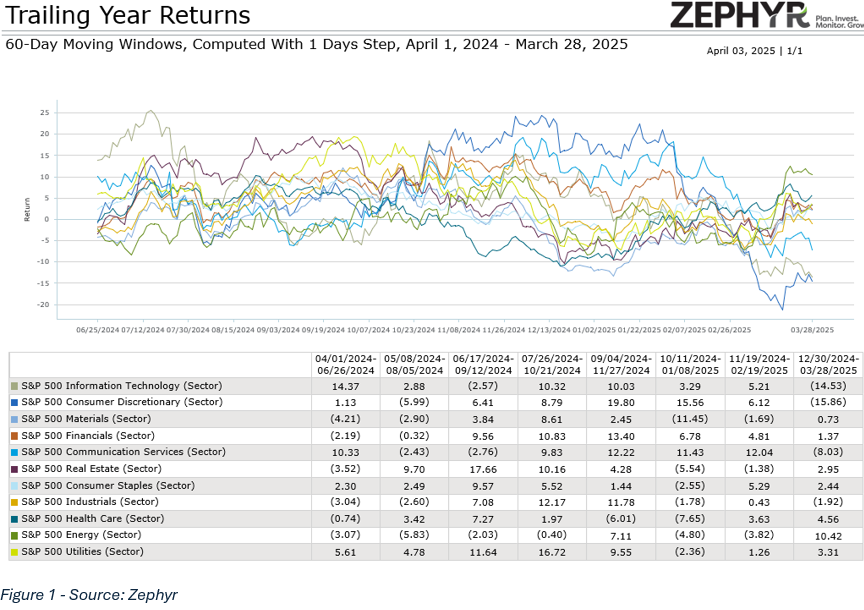

The start of 2025 has been a struggle for equities as the S&P 500 index is down over 7% and the poor performance has wiped out all of the post-2024 Presidential Election gains. Furthermore, a shift in equity leaders and recent Treasury yield movements signal investors are turning bearish. The very popular mega tech stock trade, that carried markets for the past few years has unwound, which has resulted in the NASDAQ 100 falling over 15% from its peak in February, marking a correction for the technology heavy index. The rotation into defensive sectors like health care, energy and utilities from the once outperforming cyclical sectors is also eye-opening (Figure 1). Lastly, falling Treasury bond yields have signaled that investors have become more concerned about the long-term economic growth versus short-term inflation.

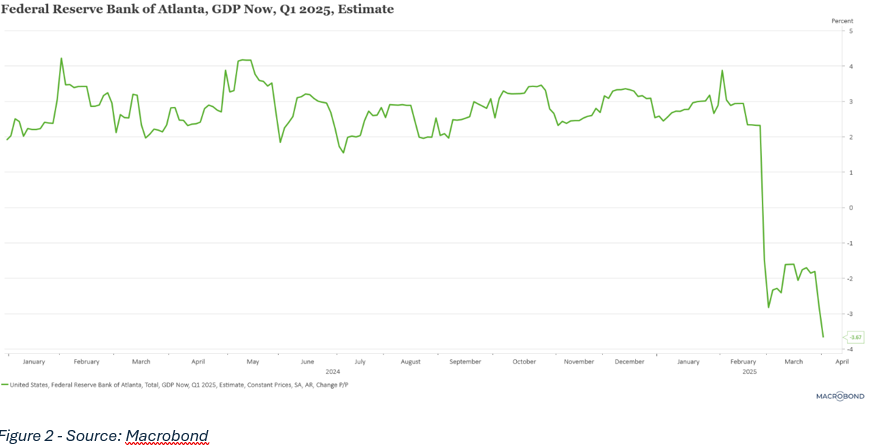

Meanwhile, a uncertain macro-economic environment adds to the gloomy outlook for equities. The boost from Donald Trump’s election victory due to his pro-growth initiatives faded quickly as the excitement turned to uncertainty as concerns over a possible trade war took the shine off. Unpredictable tariffs and the ongoing trade rhetoric continue to weigh on markets and will continue to do so until there is a clear and defined resolution. Furthermore, some cracks within the economy are starting to show themselves as economic data is starting signal slowing. The Atlanta Federal Reserve’s GDPNow model is now forecasting a 3.6% annualized decline for the first quarter (Figure 2). Important to note, the GDPNow Forecast is just that, a forecast.

Adding to the economic uncertainty is the Institute for Supply Management’s (ISM) February survey showing weakening overall conditions, new orders and employment. Meanwhile the unemployment rate has held steady recently and retail sales, while slowing, rose in February.

Taking the Emotion Out of Investing

We know that investing is very emotional, and fear is the strongest emotion. It’s understandable that investors are on edge due to the recent shift in equity performance and the less than rosy outlook, which requires financial advisors putting on their “psychologist hat”.

Conversations with clients during these volatile times are often the hardest as financial advisors try to remove emotion and get their clients to look at the bigger, long-term picture, which is easier said than done. It’s important that financial advisors balance empathy and information when trying to make sure the clients take a long-term approach rather than making near-term irrational decisions driven by fear. Here are some things to consider when having these client conversations.

Learn more about the most dominate emotion in investing.

Mid-year Corrections are Common

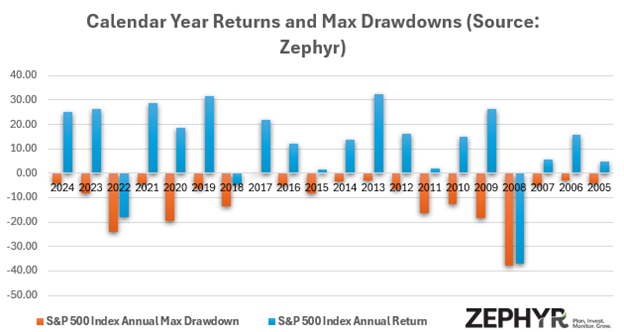

While a 10% pullback in stock prices can be tough to swallow and a cause for concern, mid-year corrections are common. Not only are mid-year corrections common, but they are also common during years of solid equity performance. Since 2005, the S&P 500 index experienced a correction (loss of 10% or more) during the calendar year seven times. Of those seven times the S&P 500 index ended the year positive four of the seven. In fact, the S&P 500 index posted +10% returns three of those seven times (Figure 3). While unnerving, a correction doesn’t indicate a bad year is upon us.

Figure 3 - Source: Zephyr

Calendar Year Declines of More Than 10% In a Year Are Rare.

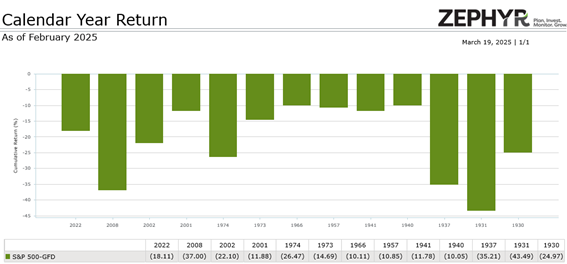

Large pull backs of more than 10% are much more uncommon and correspond to something really bad, such as a recession or war. Since 1922 (102 years) the S&P 500 index has been down more than 10% only 13 times on a total return basis. Eight of those occurrences corresponded to a recession (1930, 1931, 1937, 1957, 1973, 1974, 2001, 2008), four were during a war (1940, 1941, 1966) or heightened geo-political tensions (2002) and one was due to a Fed rate shock in 2022 (Figure 4).

Figure 4 - Source: Zephyr

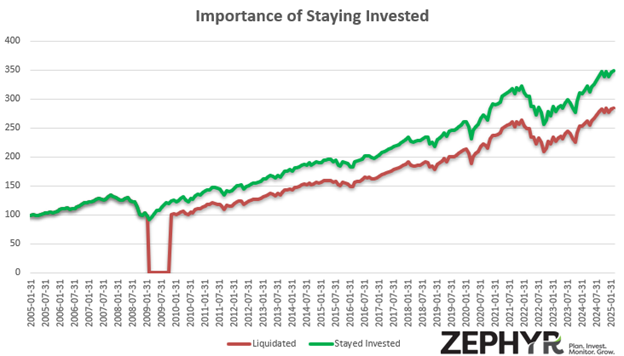

Importance of Staying Invested

During these tough conversations, the topic of liquidating or staying invested is always discussed. In some cases, showing data and graphs, like the below scenario, can make that discussion easier.

Say your client invested $100,000 20 years ago (January 2005) in a global allocation portfolio (Russell 3000 index 30%, MSCI ACWI ex USA index 20%, Bloomberg U.S. Government/Credit index 40%, Wilshire Liquid Alternative index 5%, FTSE Nareit Composite REITS index 5%). The investment portfolio climbs to $133,600 in late 2007 before the Great Financial Crisis (GFC) starts to take its toll. She does her best to stay invested before her nerves get the best of her and she liquidates in February 2009 after her portfolio falls to $97,480. The GFC bottom is reached shortly thereafter, but your client is still shaken and doesn’t feel comfortable jumping back in until later in 2009. In November 2009 she decides to jump back into the market and invests the $97,480 back into the same global allocation portfolio. The portfolio recovers and by the end of February 2025 the portfolio is worth $284,710 which looks good until you look at the alternative. Had your client stayed the course, her portfolio would be worth $348,640 at the end of February. Being out of the market for just ten months cost your client $63,930. What could’ve been (Figure 5).

Figure 5 - Source: Zephyr

Markets move quicker than ever, both on the way down and up, so it’s very hard to catch the bottom or top which puts the portfolio at risk when investors liquidate. History shows that things have to go very badly, like a recession, in order for equity markets to fall more than 10%. No one knows if a recession is on the horizon, so it’s important to create diversified investment portfolios that can balance both risk mitigation and capturing the upside.

Client conversations during times of heightened market volatility and uncertainty are arguably your hardest conversations, but your most important. As hard as it is, it’s important to keep your clients focused on achieving their long-term objectives rather than making hasty moves that could put those objectives at risk.

Looking to create similar analysis on your own? Zephyr can help.

Zephyr Can Help Advisors Create Optimized Investment Portfolios to Navigate Times of Uncertainty